The Bill From 1982

Energy shocks transmit in weeks. Industrial capacity rebuilds in decades. The difference is the story.

BY LUCA PACIOLI · PITTSBURGH PA · JUNE 2026

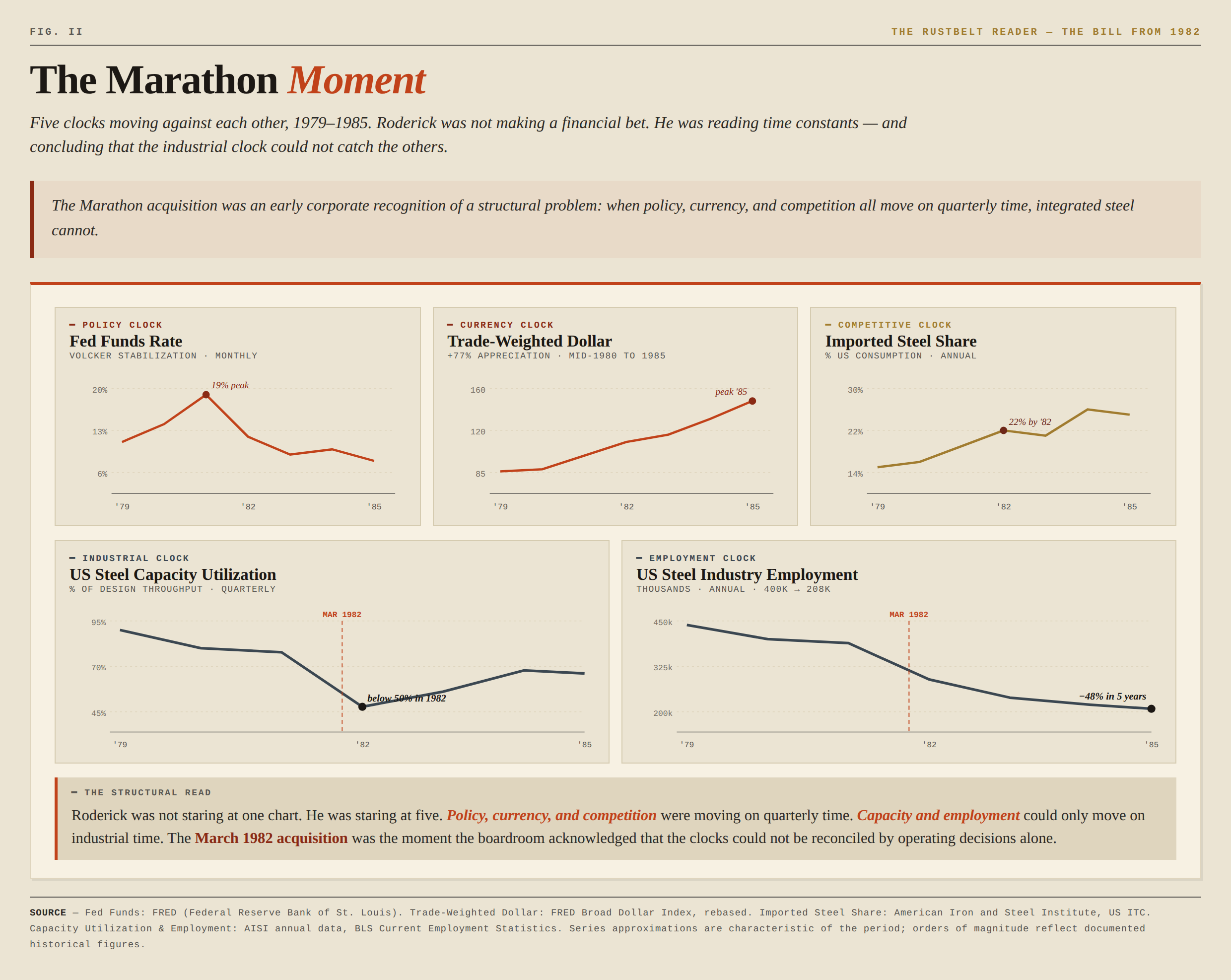

On March 5, 1982, U.S. Steel stopped behaving like a steel company.

It announced one of the largest acquisitions in American history: Marathon Oil, for $6.2 billion. At the time, many viewed the purchase as diversification.

It wasn’t. It was an admission. Management had concluded that the economics of making steel were now inseparable from the economics of producing energy. Four decades later, a proposed diplomatic agreement with Iran demonstrates that they were right — and reveals the deeper structural problem the Marathon trade was an early response to.

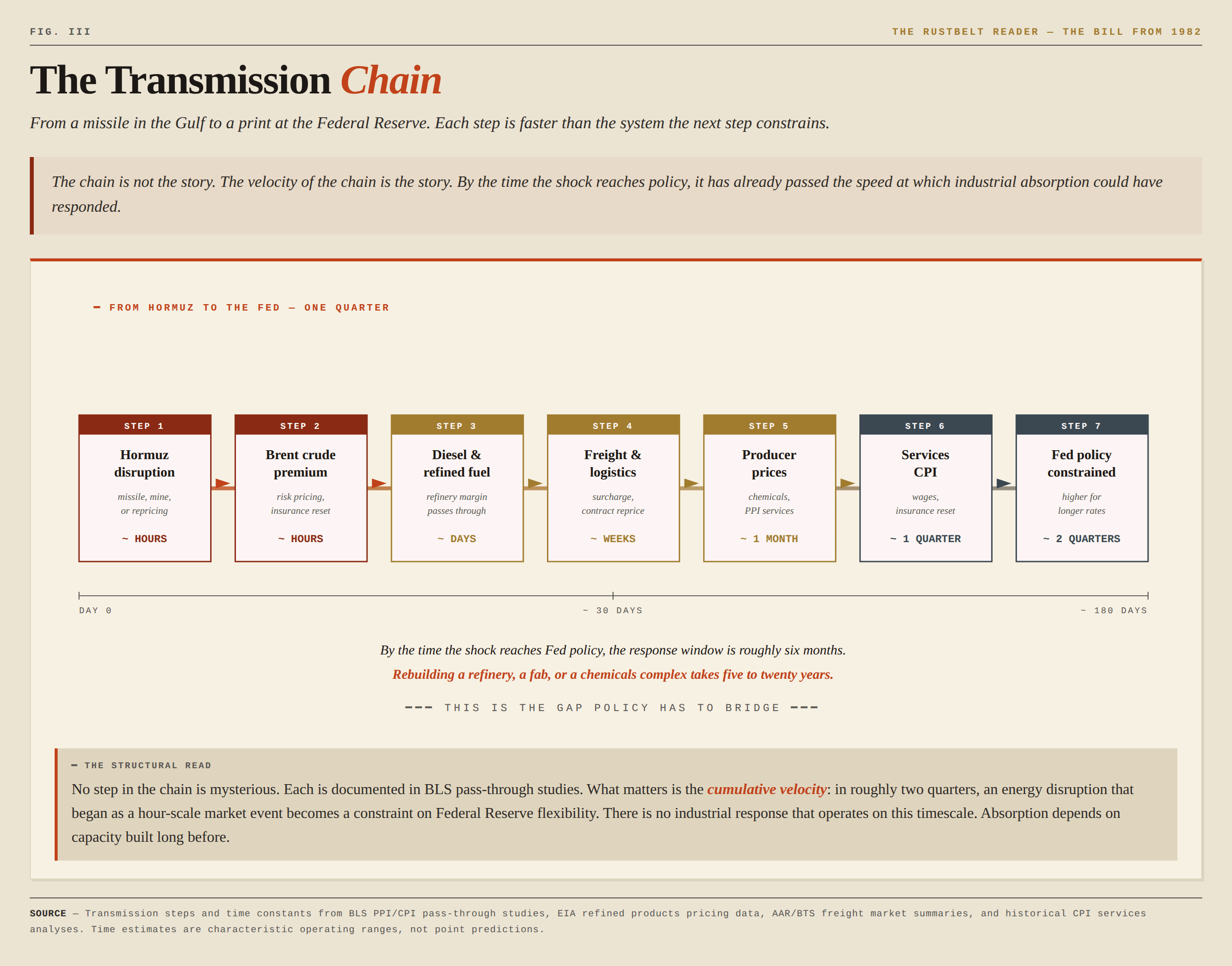

The reported fourteen-point Memorandum of Understanding between the United States and Iran is not, in the end, a story about Tehran. It is a story about time. About the speed at which an energy disruption in a narrow waterway moves through diesel, freight, chemicals, producer prices, and finally into the inflation reports that constrain Federal Reserve policy. About the speed at which industrial capacity, once optimized away, can be rebuilt — which is to say, not on a timeline that matters.

The shortest distance between Tehran and the Rust Belt is still the price of energy. But the binding constraint is not the price. It is the asymmetry between how fast energy shocks propagate and how slowly industrial systems adapt.

The framework

Energy is civilization’s universal input. Every economy has transmission mechanisms, and in industrial economies, energy is the first one. Credit, freight, chemicals, fertilizer, manufacturing margins, wages, and ultimately inflation all sit downstream from it.

But transmission is only half of the framework. The other half — the part that determines whether transmission becomes catastrophic — is the asymmetry of time constants.

The central problem is not simply that energy transmits. It is that every part of the industrial system operates on a different clock. Markets clear in days. CPI embeds in quarters. Refineries take years. Blast furnaces take decades. Policy is forced to bridge the gap. When the clock governing the shock runs faster than the clock governing the response, the system has no defense except absorption — and absorption depends on capacity that was built at the slower speed, decades before anyone knew it would be needed.

This is the mechanism behind every major American industrial dislocation of the last fifty years. The 1973 embargo did not deindustrialize the Mahoning Valley. The 2022 European gas shock did not deindustrialize Germany. The 2020 semiconductor shortage did not concentrate fabrication in Taiwan. In each case, the shock moved through the system at a speed the industrial base could not match, and revealed which parts of the system had been built thin enough to break. The Marathon acquisition was an early corporate recognition of the same problem from the other direction: a steel company concluding that the only defensive posture against a transmission mechanism it could not outrun was to own the source of the transmission itself.

The corpus

Three prior essays in this publication have traced parts of this system separately.

“The Deal That Explained America” documented the Marathon acquisition as the canonical case study of capital choosing return over resilience. David Roderick’s logic — that the highest available use of U.S. Steel’s capital was no longer steel — was rational at the firm level and destabilizing at the national-system level.

“The Most Dangerous Inflation Isn’t a Fire, It’s Transmission” identified the mechanism by which energy shocks move through the modern American cost structure. The pass-through is not instantaneous. It takes one quarter to begin and two quarters to embed. Once it embeds in services inflation, it cannot be solved by clearing a shipping lane — only by crushing demand through higher rates.

“Which Clock Breaks First” established that the current Iran conflict is two endurance contests coupled through energy markets. The variable that determines what end-state is achievable is services-less-shelter CPI. The April print landed at exactly the embedment threshold the framework had specified.

The three essays describe a system. This one describes the constraint inside the system: the rate at which energy shocks transmit through industrial economies is far faster than the rate at which industrial capacity can be rebuilt. Every other observation in the corpus sits inside that asymmetry.

Velocity, exposed

The 1970s did not deindustrialize the United States. Aging plants, globalization, exchange rates, labor costs, and technological change all mattered, and most of them were trends underway before OPEC announced an embargo in October 1973. What energy did was transmit those trends faster than the system could absorb them.

The mechanism is consistent because energy touches almost every productive activity. A crude price shock moves into diesel within days, into freight within weeks, into producer prices within a month, and into services inflation within a quarter. Each step amplifies whatever existing weakness it finds. A marginal steel mill becomes uneconomic. A leveraged shipping company faces a balance-sheet problem. A chemicals plant operating on thin margins moves into operating losses. The shock does not create the weakness. It reveals which parts of the system were thin enough to break under transmission pressure.

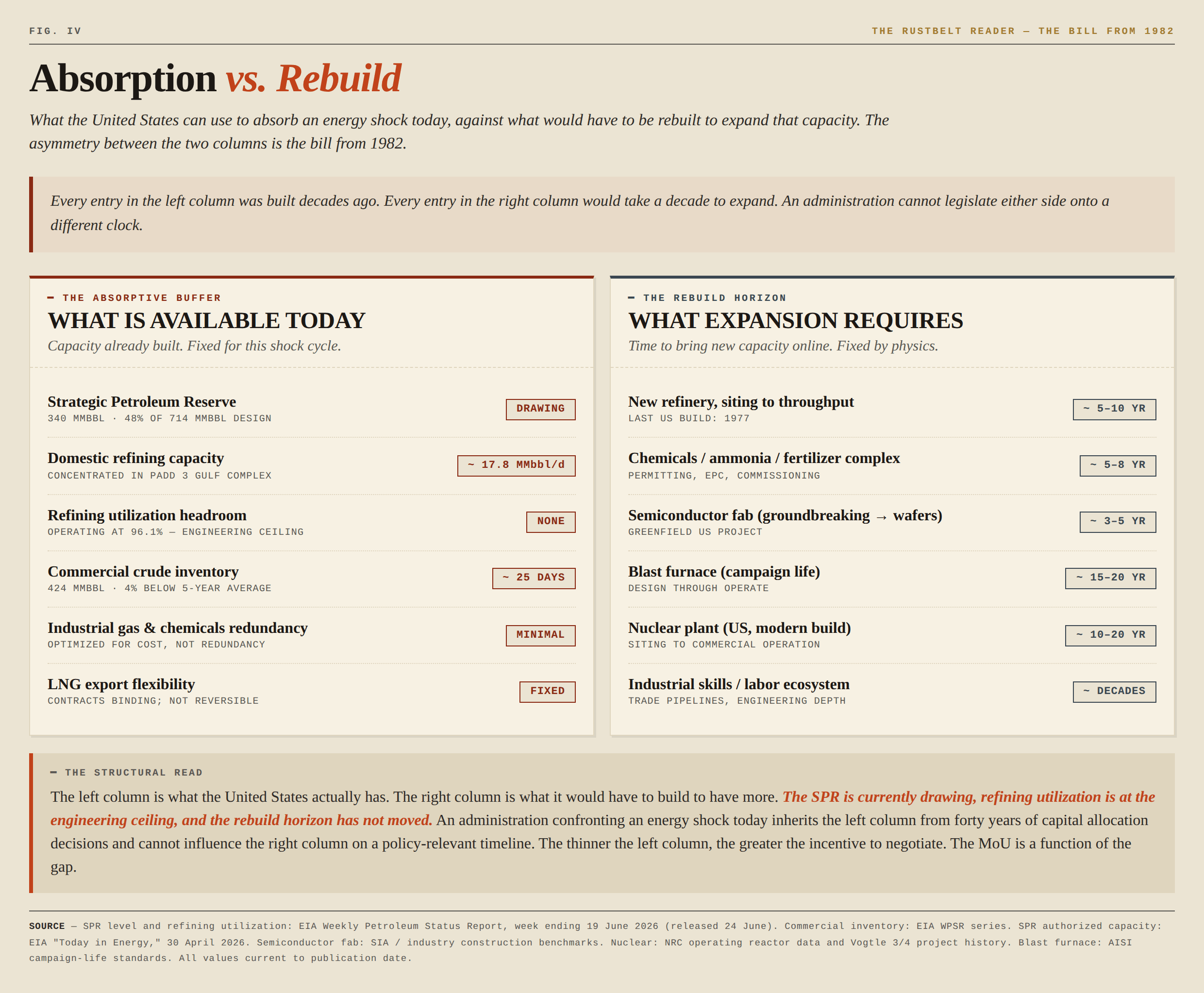

The rebuild velocity is on a different scale entirely. A blast furnace has a campaign life of fifteen to twenty years and a build cycle of five to seven. A refinery requires roughly a decade from siting to throughput. The last new US refinery completed construction in 1977 — the same year as Black Monday at Youngstown Sheet & Tube. A modern semiconductor fab requires three to five years from groundbreaking. A nuclear plant requires fifteen years if the regulatory environment cooperates and longer if it doesn’t. Industrial supply chains, once relocated, take a decade or more to bring back, and the labor pool and skills ecosystem that supported them require even longer.

This is the asymmetry that makes energy shocks structurally different from other macroeconomic events. An interest-rate shock can be reversed by the institution that created it. A currency shock has tools and counterparties. An energy shock, once it enters the transmission chain, can only be managed by absorption — and absorption depends on capacity that was built decades earlier.

The United States built that capacity once. Then, beginning in the 1980s, it began to optimize it away.

What the optimization trade exposed

The forty years that followed produced the highest-return equity market of any major economy. They also produced an industrial absorptive profile structurally different from every other Western economy and most major Eastern ones.

The Strategic Petroleum Reserve, drawn from to absorb the current shock, sat at 340 million barrels in mid-June 2026 — well below its 727-million-barrel peak, below its prior all-time low, and at 48% of its 714-million-barrel authorized design capacity. The buffer being spent today was built decades ago, and the rate at which it can be refilled is set by physics, not policy. Domestic refining capacity has not grown materially in two decades, with throughput concentrated in Gulf Coast complexes operating at 96.1% utilization — the engineering ceiling for sustained operation. US LNG export commitments, signed during the period when American natural gas was treated as a strategic surplus, now function as a draw on domestic supply during stress. Industrial gas, ammonia, and chemicals capacity — the second-derivative inputs that determine fertilizer prices, plastics availability, and downstream manufacturing margins — have been optimized for cost rather than redundancy. The 2022 European chemicals shock was a preview of what the American complex looks like under similar pressure.

None of these conditions are catastrophic in isolation. What makes them structurally significant is the velocity asymmetry. Each represents a thin point in the transmission chain that cannot be rebuilt on a policy timeline. An administration confronting a potential energy shock must negotiate within the industrial and energy system it inherits. The thinner that system’s absorptive capacity, the greater the incentive to avoid prolonged disruption.

The countries that did not make the same optimization trade have different transmission profiles. Japan never abandoned its METI-level energy-security planning. China retained heavy industry and built domestic refining and strategic reserves at scales the US has not matched. Germany’s 2022 lesson was to rebuild industrial energy redundancy, not to abandon it. They can absorb a longer shock because they were built differently.

The mainstream reading of the MoU treats it as a contest between American leverage and Iranian endurance. The framework the corpus has built suggests the contest that actually matters runs on a different axis: American transmission velocity against American rebuild velocity. The first is set by global energy markets. The second was set in boardrooms forty years ago.

The constraints

Whatever its provisions, the reported agreement runs into four constraints that no diplomatic instrument can dissolve.

Geography. The Strait of Hormuz is approximately twenty-one miles wide at its narrowest and carries roughly a fifth of global seaborne oil. The chokepoint exists regardless of what is signed. Any agreement that does not credibly reduce the probability of disruption has only postponed the question of when the next shock arrives.

Money is never just money. The Middle East’s principal powers rarely compete directly; they compete through proxies. Financial flows therefore become strategic flows. An agreement that releases capital to Tehran without specifying its destination has redirected pressure, not resolved it.

The Israel balance never resolves. American Middle East policy carries a permanent tension between regional de-escalation and Israeli security. The two objectives reinforce each other only sometimes. The reported MoU has drawn criticism for tilting toward the first. Whether that critique proves fair, the underlying dilemma is structural.

History rhymes in numbered lists. The fourteen-point framing is itself an echo. More than a century ago, Woodrow Wilson introduced his own Fourteen Points as the First World War dismantled the Ottoman Empire. Wilson imagined a stable regional order built on self-determination. What came instead were mandates, artificial borders, competing nationalisms, and most of the unresolved conflicts the current MoU is trying to manage. History rarely repeats exactly. But it often rhymes in numbered lists.

On March 5, 1982, U.S. Steel’s board concluded that steel and energy had become the same business.

Forty-four years later, diplomats negotiating over the Strait of Hormuz are confronting the same reality from the opposite direction.

The boardroom discovered what the map already knew.

Industrial power begins with energy.

Everything else is transmission.

RELATED ESSAYS:

The Deal That Explained America

The Most Dangerous Inflation Isn’t a Fire, It’s Transmission

The Most Dangerous Inflation Isn’t a Fire — It’s Transmission

The latest inflation data looked uncomfortable. Core PCE came in firm, and while Core CPI has cooled, it remains above target. Monthly prints are still stuck in that familiar 0.2%–0.4% range.

Which Clock Breaks First