Which Clock Breaks First

Two endurance contests, one war, and the inflation variable that decides the end state

David Capezzuto | Pittsburgh PA | May 27, 2026

For five months now I’ve been writing about Iran from two angles that I treated as separate. One was the Iranian clock — the arithmetic of a regime cornered by broken money, escalating coercion, and external capacity arriving on top of both. The other was the Western clock — the political and financial endurance of the societies prosecuting the campaign, channeled through bond markets and inflation transmission.

I treated them as two analyses. That was a mistake. They are one analysis, and the war’s end state will be determined not by the battlefield but by which of these two clocks breaks first.

Stated plainly: one side is trying to survive economic collapse long enough to outlast the pressure campaign. The other is trying to sustain pressure without reigniting the inflation problem that nearly broke its own political economy. That is the contest. Not simply Israel versus Iran, or America versus Tehran, but regime endurance versus democratic inflation tolerance.

This is the integration piece.

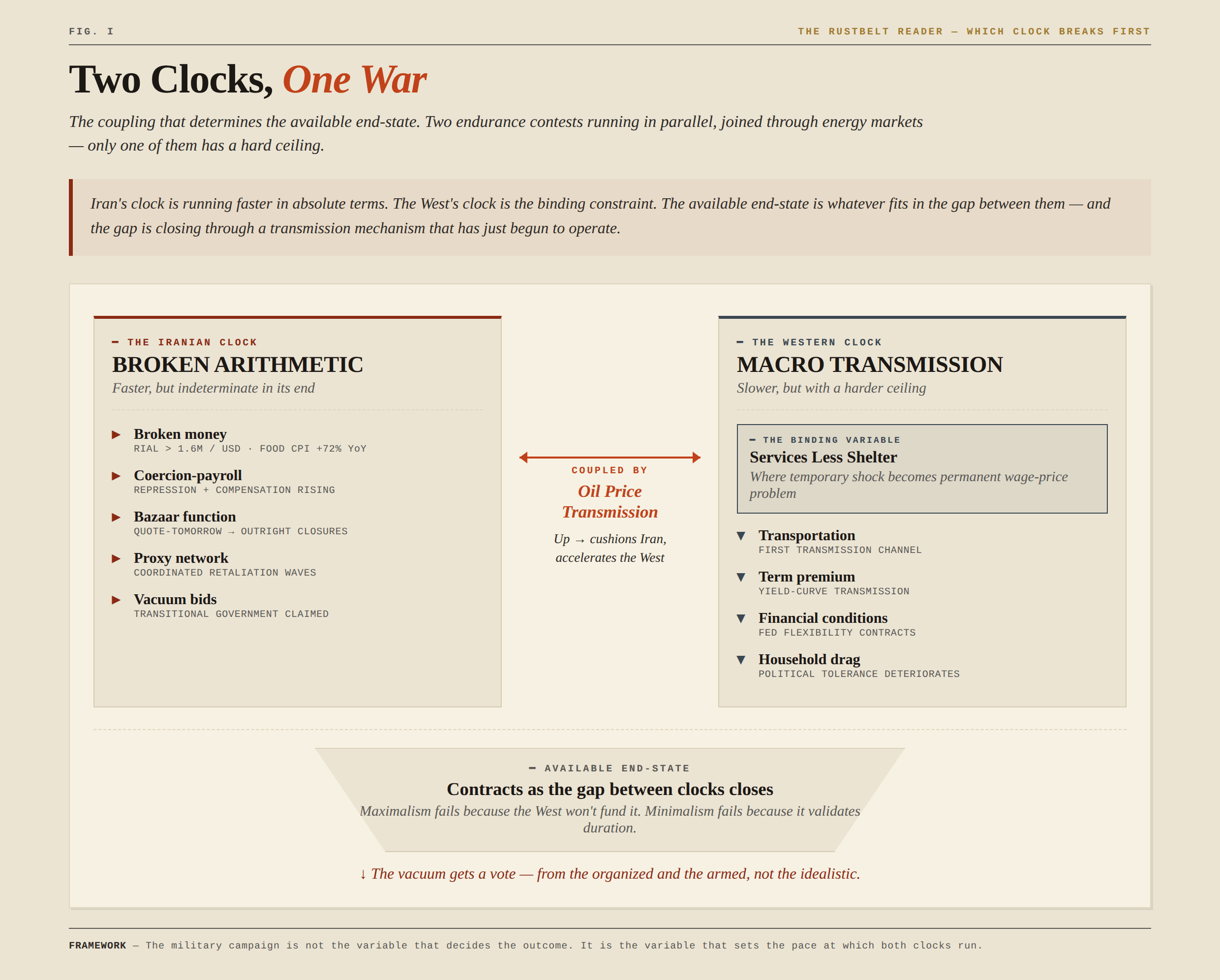

The thesis is this: Iran’s clock is running faster in absolute terms, but the Western clock is the binding constraint. The campaign has runway, but the runway is shorter than the headline data suggests, and the indicator that defines its length is not the one most commentary is watching.

The two clocks, restated

The Iranian clock is well-established in my earlier work. The rial trades through 1.6 million per dollar on the open market. Food inflation runs above seventy percent year-over-year. The bazaar — the most reliable single indicator of whether the Iranian economy is clearing — has moved from quote-tomorrow pricing to outright closures. Coercion has expanded from policing to a level of domestic enforcement closer to internal-security crisis than routine repression. And a self-declared transitional government has already started bidding for the vacuum that does not yet exist.

The claim does not need to be legitimate to matter. It matters because organized actors are beginning to bid for the post-regime space before the regime has fallen.

The external clock joined these in February when posture became contact. The campaign has not been an episode. It has been operations: multiple waves, multiple target sets, sustained design. Treasury has paired kinetic pressure with financial containment. The architecture of the pressure is broader and more durable than any single strike package.

The Western clock is the less obvious half of the contest, and the one most analysis still misreads. It does not run on public approval polls or congressional patience in the abstract. It runs on the macro-financial channel: oil shock to inflation expectations to long-end yields to credit conditions to growth. That chain is well understood. What it does not capture is the specific transmission mechanism — and the transmission mechanism is the actual clock.

That mechanism is energy pass-through into services inflation, particularly services less shelter — the services categories outside housing, where wages, transportation, insurance, maintenance, and other operating costs reveal whether an energy shock is being absorbed or embedded.

It is where a temporary energy shock becomes a permanent domestic wage-price problem. Once inflation moves out of volatile commodities and into wages and structural consumer behavior, it cannot be fixed by clearing a shipping lane. It can only be fixed by crushing domestic demand through higher-for-longer rates.

That is the trap, and it is why the Fed ends up treating a foreign-policy shock as a domestic inflation problem — not because anyone wants it to, but because the variable that constrains its policy room is sitting in the consumer basket, not in the Strait of Hormuz.

There is a historical rhyme worth naming. Suez ended not because Britain lacked soldiers, but because it lacked financial runway. The pressure point was not the battlefield; it was sterling. The principle applies here in a different form. The West’s constraint is not immediate military capacity. It is the inflation-financial channel through which energy shocks become domestic political limits.

This is why I’m narrowing the Western clock to a single indicator. The dashboard of yields, term premium, manufacturing construction, and the maturity wall provides context. But the binding variable is the pass-through. Everything else is downstream of it.

Why Iran’s clock is faster

The Iranian clock appears to be running faster than the Western clock right now, at least across the indicators that measure regime stress. The rial has moved an order of magnitude. Food inflation is at levels that historically correlate with regime instability. The coercion-payroll problem — the question of whether the security apparatus can be funded as legitimacy decays — is no longer hypothetical. The vacuum is not a future concern; it is already being bid on.

The five watch items I established in my February piece have all moved in the same direction over the last six weeks.

Flow risk: ships still transit Hormuz, but insurance markets are repricing war-risk coverage, and routing behavior is shifting from normal to contingency.

Escalation bet: Iran’s launches have arrived in coordinated waves, suggesting command-and-control persistence despite degradation, and proxy networks have signaled intent to widen the map.

Coercion capacity: the regime is doing both — increasing repression and increasing compensation, which is the literal arithmetic of payroll-dependent control.

Narrative oxygen: the foreign-fingerprints framing has accelerated, with “rioters” and “armed terrorists” replacing “protesters” in official language.

Vacuum bids: the transitional government claim is the most consequential domestic event since the protests began, because it shifts the question from whether a vacuum will form to who fills it.

Each of these has moved in the same direction. The cumulative reading is compression, not drift.

But here is the asymmetry that matters: a fast clock is not the same as a binding clock. Iran’s clock running fast tells you the regime is fragile. It does not tell you what end state is available, because what is achievable depends not on how fast Iran is breaking, but on how much runway the West has to convert that breakage into a durable outcome.

That conversion runway is what the Western clock measures.

Why the Western clock is the binding constraint

The Western clock is slower, but it has a harder ceiling. And the ceiling is closer than the headline inflation data suggests.

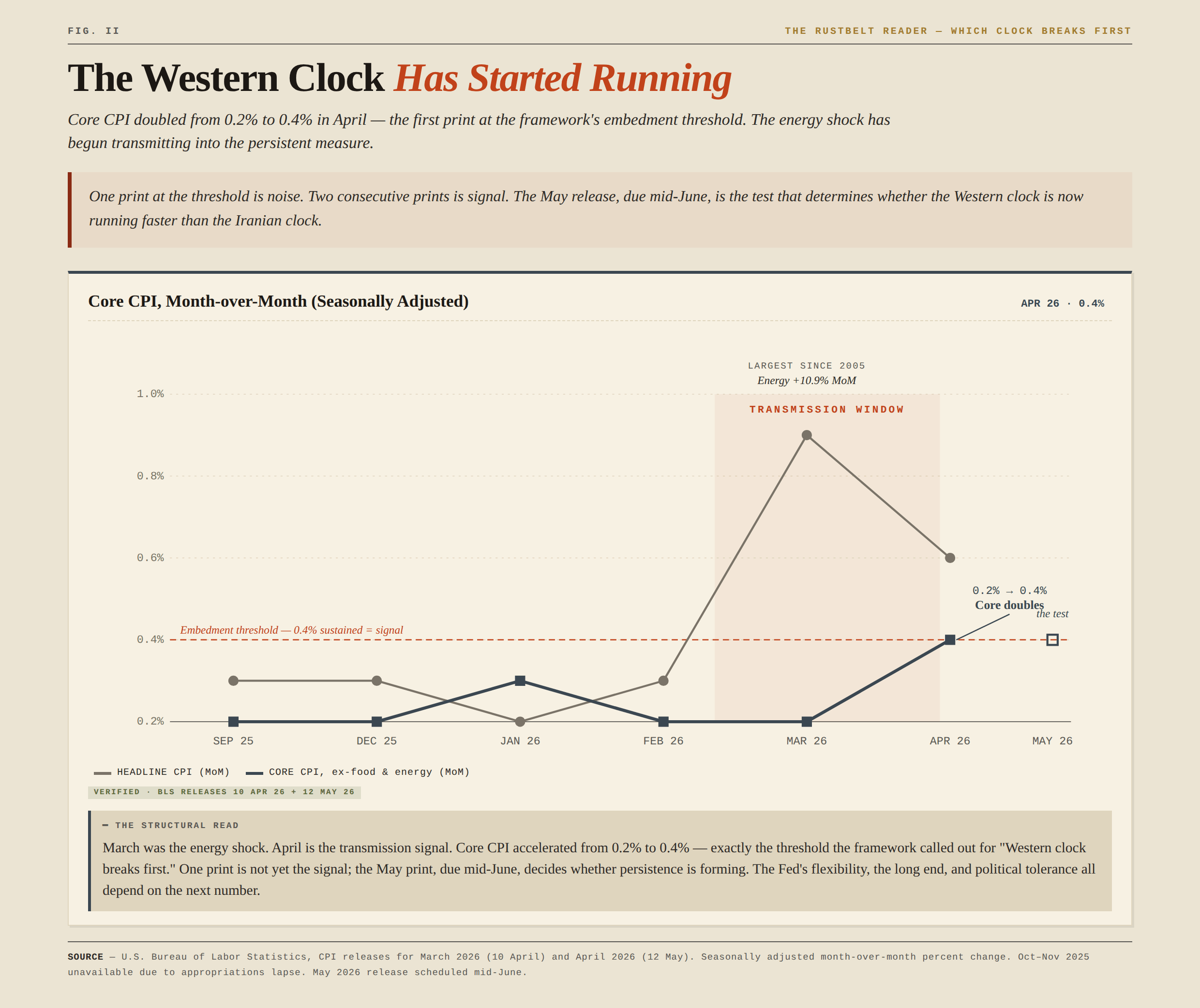

Through 2025 and into early 2026, the structure of inflation was generally improving. Headline numbers stayed sticky because of shelter and legacy categories, but the cyclical components were cooling. The system was warm, not overheating. The disinflation trend was intact.

Then came March.

Headline CPI jumped 0.9% month-over-month, driven almost entirely by energy. Energy alone rose 10.9% in a single month, the largest move since 2005. Gasoline rose 21.2%, the largest monthly increase since that series began in 1967. Core CPI held at 0.2%, which on the surface read as reassuring. But transportation services rose 0.6%, and the directional setup was clear: an energy shock of that scale was the kind of catalyst the transmission framework had been describing.

Then came April.

Core CPI accelerated to 0.4% — doubling from the March print. That is exactly the threshold the framework identified as the embedment signal. The April print is the first serious challenge to the disinflation trend that had been intact since mid-2025. One print at the threshold is not yet the confirmed signal; that requires two consecutive prints. But the trajectory has changed.

This is what the Western clock looks like when it starts running. Not a spike. A break in trend, followed by a print at the threshold.

The transmission process is not instantaneous. It takes sixty to ninety days for fuel costs to fully move through transportation into producer costs, and another cycle to reach consumer services. The April print is the initial signal. The May release, due in mid-June, is the test.

If services less shelter stabilizes or drifts back into the prior deceleration trend, the clock effectively resets. If it firms again — and with energy still elevated and Hormuz risk priced into insurance and routing, continuation is the more likely path — then the Western clock will have begun accelerating faster than the headline data suggests.

That is the asymmetry of the contest. Iran’s clock is faster but indeterminate in its end. The Western clock is slower but has a defined ceiling. Whichever clock breaks first determines what is achievable.

The coupling

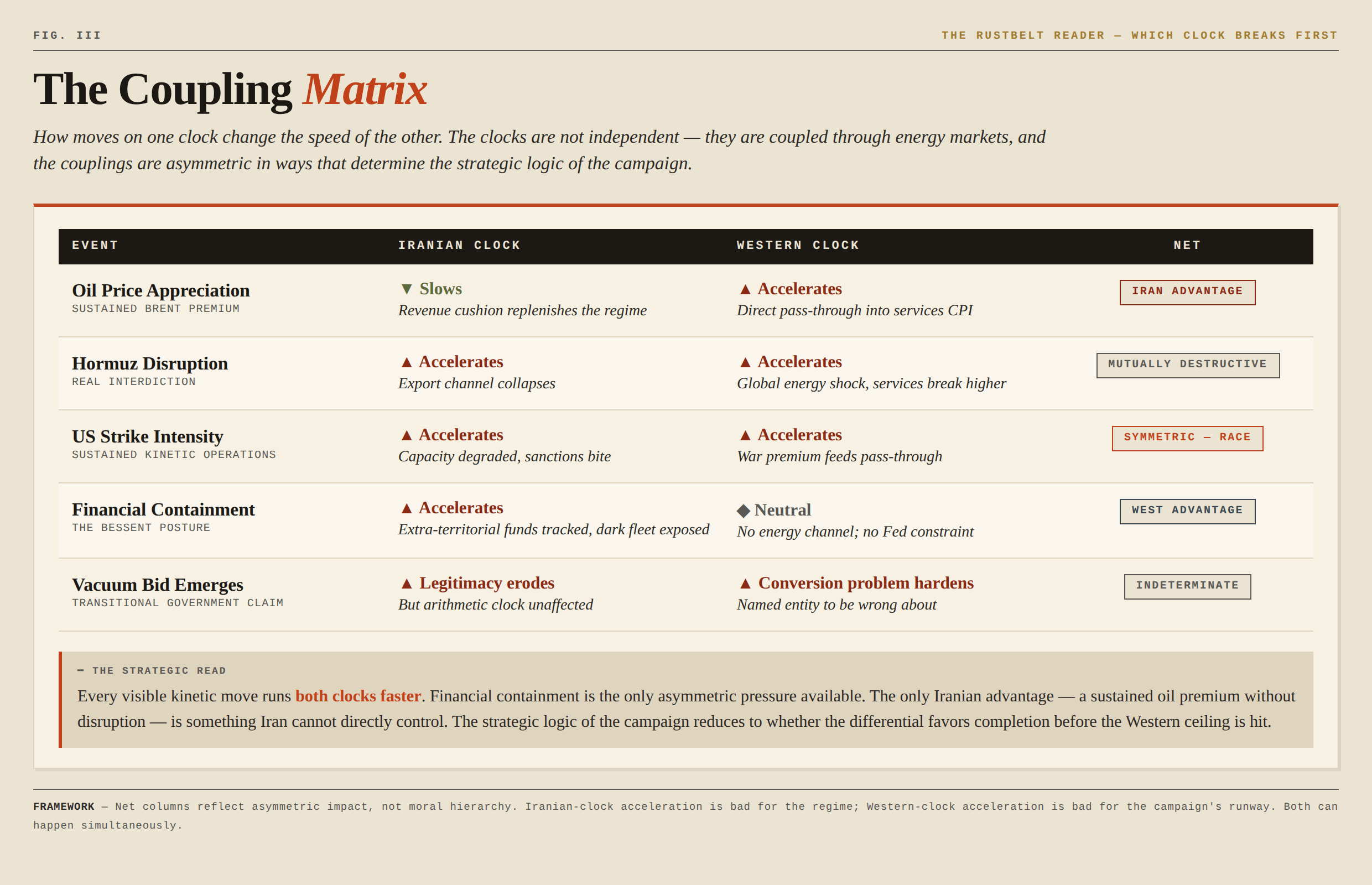

The clocks are not independent. They are coupled, and the couplings are asymmetric in ways that determine the strategic logic of the campaign.

The matrix tells you what the campaign actually looks like, stripped of the rhetoric. Every visible move on the kinetic side runs both clocks faster. The only asymmetric pressure is financial. The only Iranian move that benefits Iran on net — a sustained oil premium without disruption — is something Iran cannot directly control.

Two couplings deserve emphasis.

The first is the strike paradox: kinetic pressure runs both clocks. Degrading Iranian capacity accelerates the Iranian clock, but the war premium that follows accelerates the Western clock too. There is no version of sustained kinetic operations that does not consume Western runway as it consumes Iranian capacity. The strategic question becomes whether the differential favors completion before the Western ceiling is hit.

The second is the financial-containment advantage. Treasury’s posture under Bessent — targeting Iran’s oil revenues, currency channels, shadow-fleet networks, and foreign financial intermediaries in parallel with kinetic pressure — is the only available move that accelerates the Iranian clock without running the Western clock faster. It does not have the visible effect of a strike, but it is the most efficient pressure available because it is the only asymmetric one.

This is why financial containment is doing more work than the headlines suggest.

The call

Given the readings: Iran’s clock is faster than the West’s right now. But the differential is narrowing, and the variable that closes it is services less shelter pass-through. The April print just landed at the embedment threshold. May tells us whether that was noise or signal.

The available end-state is whatever can be achieved before services less shelter breaks. If transmission stays contained through the second quarter, the campaign retains room for the harder objectives — sustained capacity degradation, financial isolation, possibly engineered regime fracture. If transmission embeds, the available end-state contracts to deterrence restoration and capacity degradation, with the conversion problem unresolved and the vacuum left to the organized.

This is why maximalism is not so much wrong as structurally unavailable. The Western clock will not tolerate a multi-year regime-change campaign with vacuum-management overhead. It might tolerate a six-to-nine month finishing window if transmission stays contained. The honest version of the conversion question is not what we would like to achieve, but what fits inside that window.

My read: a defined, limited objective — sustained capacity suppression and financial containment, with regime fragmentation as a possible byproduct but not an explicit goal — is the only objective that is both meaningful and achievable within the Western clock’s tolerance.

Maximalism fails not because it is morally wrong but because the West’s clock won’t fund it. Pure minimalism — one-and-done deterrence — fails because it validates the duration strategy and resets the same problem for the next decade.

The narrow middle path is the only one that survives the arithmetic of both clocks.

What would change this call

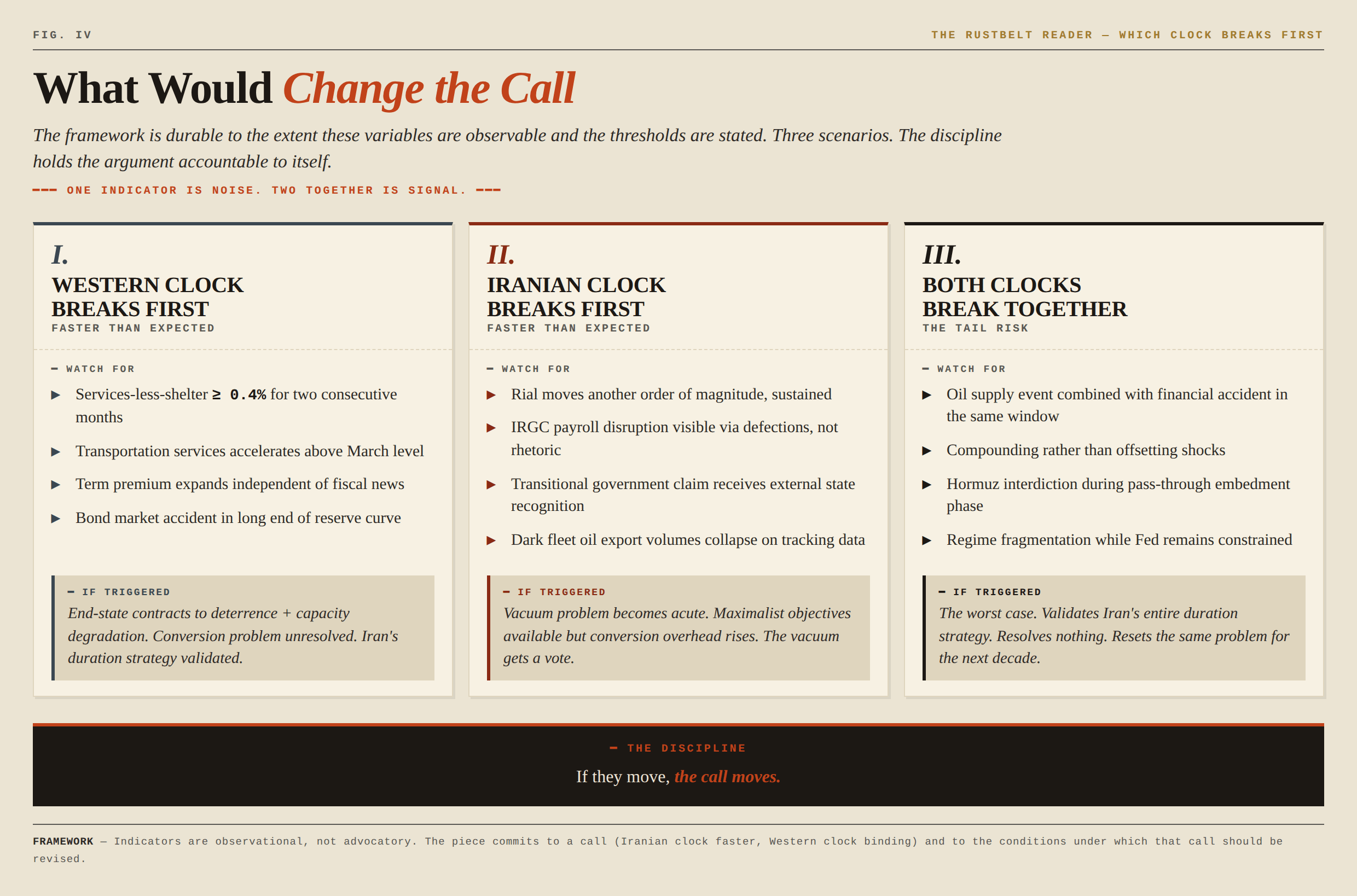

One indicator is noise. Two together are signal.

I would update toward “Western clock breaks first, faster than expected” if I saw services less shelter print at or above 0.4% for two consecutive months — a condition the April print has met one half of. Confirmation would also include transportation services accelerating above its March level, term premium expanding independent of fiscal news, or a bond market accident in the long end of a major reserve currency curve.

I would update toward “Iranian clock breaks first, faster than expected” if I saw the rial move another order of magnitude on a sustained basis, IRGC payroll disruption become visible through defections rather than rhetoric, the transitional government claim get external recognition from a state actor other than the obvious adversaries of Tehran, or dark-fleet oil export volumes collapse on tracking data.

I would update toward “both clocks break together” — the worst version — if I saw an oil supply event combined with a financial accident in the same window. That is the tail risk that resolves nothing and validates everything Iran’s duration strategy was built to test.

The framework is durable to the extent these variables are observable and the thresholds are stated. If they move, the call moves.

Closing

Iran’s clock is running faster. The West’s clock has the harder ceiling. The available end-state is whatever fits in the gap between them, and that gap is closing through a transmission mechanism that has just begun to operate.

The military campaign is not the variable that decides the outcome. It is the variable that sets the pace at which both clocks run.

The vacuum, as always, gets a vote — from the organized and the armed, not the idealistic. The question is whether the campaign can finish before either clock forces it to stop.

Sources

US inflation data

BLS, Consumer Price Index — March 2026 release, April 10, 2026:

https://www.bls.gov/news.release/archives/cpi_04102026.htmBLS, Consumer Price Index — April 2026 release, May 12, 2026:

https://www.bls.gov/news.release/cpi.htmBLS, CPI release calendar:

https://www.bls.gov/schedule/news_release/cpi.htm

Iran economic stress

Iran Focus, Iran’s Point-to-Point Inflation Surpassed 52% in December:

https://iranfocus.com/economy/56505-irans-point-to-point-inflation-surpassed-52-in-december/The Guardian, Iran coverage on food-price hikes and inflation pressure:

https://www.theguardian.com/world/iranReuters, Iran coverage on rial open-market rates and currency stress:

https://www.reuters.com/world/middle-east/Associated Press, Iran coverage on rial weakness and currency stress:

https://apnews.com/hub/iran

Civil-conflict pressure and regime coercion

The Economist, “The violence in Iran could lead to civil war,” February 1, 2026:

https://www.economist.com/middle-east-and-africaFinancial Times, Middle East coverage on Iranian crackdown dynamics:

https://www.ft.com/world/mideast

Treasury and financial containment

US Treasury, Secretary Bessent remarks on Iran maximum pressure, April 2025:

https://home.treasury.gov/news/press-releasesUS Treasury / OFAC, recent sanctions actions on Iranian currency exchanges, oil-revenue networks, and shadow-fleet activity:

https://ofac.treasury.gov/recent-actions

Hormuz, shipping, and insurance repricing

Financial Times, coverage of US military posture around Iran and the Gulf:

https://www.ft.com/content/Reuters, marine insurance and shipping-market coverage:

https://www.reuters.com/business/

Transitional government claim and vacuum bidding

See prior pieces in this series for full attribution and background:

Prior pieces in this series

The Check Bounced

When the Check Bounces, the Bullets Fly, and the Carriers Move

Iran: The External Clock Started Running

The Other Battlefield in a War With Iran

The Most Dangerous Inflation Isn’t a Fire — It’s Transmission