When the Grid Becomes the Liability — Part II

The receipts: how California rebuilt wildfire finance, why Berkshire sold, and what credit markets are actually pricing

Utilities were supposed to be the safest business in America: regulated monopolies with predictable returns.

Then wildfire risk met jury rooms—and it became a fight over who pays.

In the old utility world, the pitch was simple: steady and dull.

A regulated monopoly earns an allowed return, builds long-lived infrastructure, and pays a predictable dividend. Equity gets bond-like stability. Credit gets near-sovereign comfort.

Warren Buffett’s Berkshire Hathaway Energy (BHE) was built for that world.

Natural monopolies. Long-duration capital investment. Regulated returns.

In 2019, that assumption collided with reality.

PG&E — the largest utility in California — filed for bankruptcy after the 2017–2018 megafires turned contingent liability into an existential funding problem. The event mattered far beyond one company. It forced California to confront a brutal truth:

If wildfire losses remain uncapped, the grid becomes unfinanceable at regulated returns.

That bankruptcy is why the state rebuilt the wildfire model around certification, pooled backstops, and securitization — not to make fire risk disappear, but to keep capital markets open when it inevitably appears.

Then the wildfire era arrived — and it stopped being a California-only problem.

Why This Matters Now

The wildfire story is no longer just an environmental problem or a regional utility issue.

It is rapidly becoming a capital markets story.

Over the next decade the United States must invest trillions of dollars to electrify transportation, expand transmission networks, and harden aging infrastructure against extreme weather.

Those investments require one thing above all else:

cheap, reliable access to capital.

If wildfire liabilities make regulated utilities unfinanceable, the consequences extend far beyond California or Oregon.

They reach directly into:

the cost of electricity

the pace of grid expansion

and ultimately the feasibility of the entire energy transition.

The Question Beneath the Entire Sector

Before diving into PacifiCorp, California, or the bond market, one question sits beneath the entire utility sector:

When a catastrophic wildfire occurs — who ultimately pays?

Ratepayers?

Taxpayers?

Insurance markets?

Equity investors?

Or bondholders higher in the capital stack?

For a century the answer was mostly invisible because disasters were manageable.

Wildfire risk changed that.

Today the western utility sector is increasingly priced around one uncertainty:

Does the next fire stay in equity — or migrate up the capital stack into credit?

1) PacifiCorp’s Reality: Mitigation Is Real — Perfection Is Not

PacifiCorp has not been asleep at the switch.

Its wildfire mitigation program spans multiple states and includes the full modern playbook:

grid hardening

covered conductors

advanced relays

weather monitoring systems

vegetation management

public safety power shutoffs (PSPS)

Yet exposure persists.

Because tail risk is not linear.

The scale of the legal exposure is already staggering.

PacifiCorp has reached roughly $2.2 billion in wildfire settlements and faces estimates of as much as $55 billion in potential claims tied to western US fires, according to reporting on the company’s litigation exposure.

Oregon’s 2020 Labor Day fires produced a major jury verdict in 2023 and ongoing class certification fights that could broaden the claim set.

Ratings pressure has followed. PacifiCorp’s credit rating has fallen to one notch above junk territory, a remarkable development for what was once considered one of the most stable regulated businesses in the country.

Financing flexibility has become, in part, a regulatory question.

This is the uncomfortable truth:

Risk management reduces probability.

It does not eliminate maximum loss.

S&P summarized the mismatch in a recent investor FAQ.

Investor-owned utilities were designed a century ago to deliver reliable service with modest equity returns (roughly 9–11%) and relatively high leverage (around 50% debt).

That capital structure was never built to absorb multi-billion-dollar catastrophe liabilities.

One extreme event can devastate credit quality.

Perfection is not possible. That is not ideology. That is math.

2) Why Berkshire Sold — and Why Manulife Is in the Deal

Seen through that lens, Berkshire’s move reads less like a philosophical pivot and more like risk management and balance-sheet defense.

When a conglomerate owns a regulated monopoly, wildfire liabilities are not just operational risks.

They threaten the consolidated fortress through contingent liabilities.

Selling a “cleaner” asset can function as liquidity management while larger legal exposures remain unresolved elsewhere.

Now zoom in on the buy side.

Portland General Electric’s logic is straightforward:

acquire rate base

acquire customers

acquire long-duration infrastructure growth

Manulife solves a different problem.

How do you finance a large equity check without:

over-levering the balance sheet

diluting shareholders

concentrating catastrophic exposure?

The answer is structural.

Capital markets will fund growth — but a large minority partner helps absorb first-loss volatility, ring-fence risk, and keep the broader enterprise financeable when the next event arrives.

Manulife is not a legal shield.

It is a capital stack design choice.

3) California’s Redesign: PG&E’s Bankruptcy Forced a New Model

California responded to the PG&E bankruptcy not by eliminating wildfire risk, but by engineering a financial architecture to contain it.

The redesign rests on three pillars.

I. Operating Certification

Utilities must file formal wildfire mitigation plans and obtain annual safety certifications.

Operational discipline becomes the gateway to financial protection.

II. A Pooled Wildfire Backstop

California created a large wildfire fund to prevent each fire season from triggering a capital-markets shutdown.

Ratings analysts have been explicit: for high-exposure utilities, a robust wildfire fund is central to maintaining investment-grade credit.

Without it, the capital stack cannot support uncapped catastrophe risk.

III. Securitization

This is the bridge.

Wildfire liabilities are converted into rate-recovery streams, financed through securitization structures in capital markets.

Instead of collapsing balance sheets overnight, catastrophe costs become long-duration regulated obligations.

California did not solve fire.

It solved finance after fire.

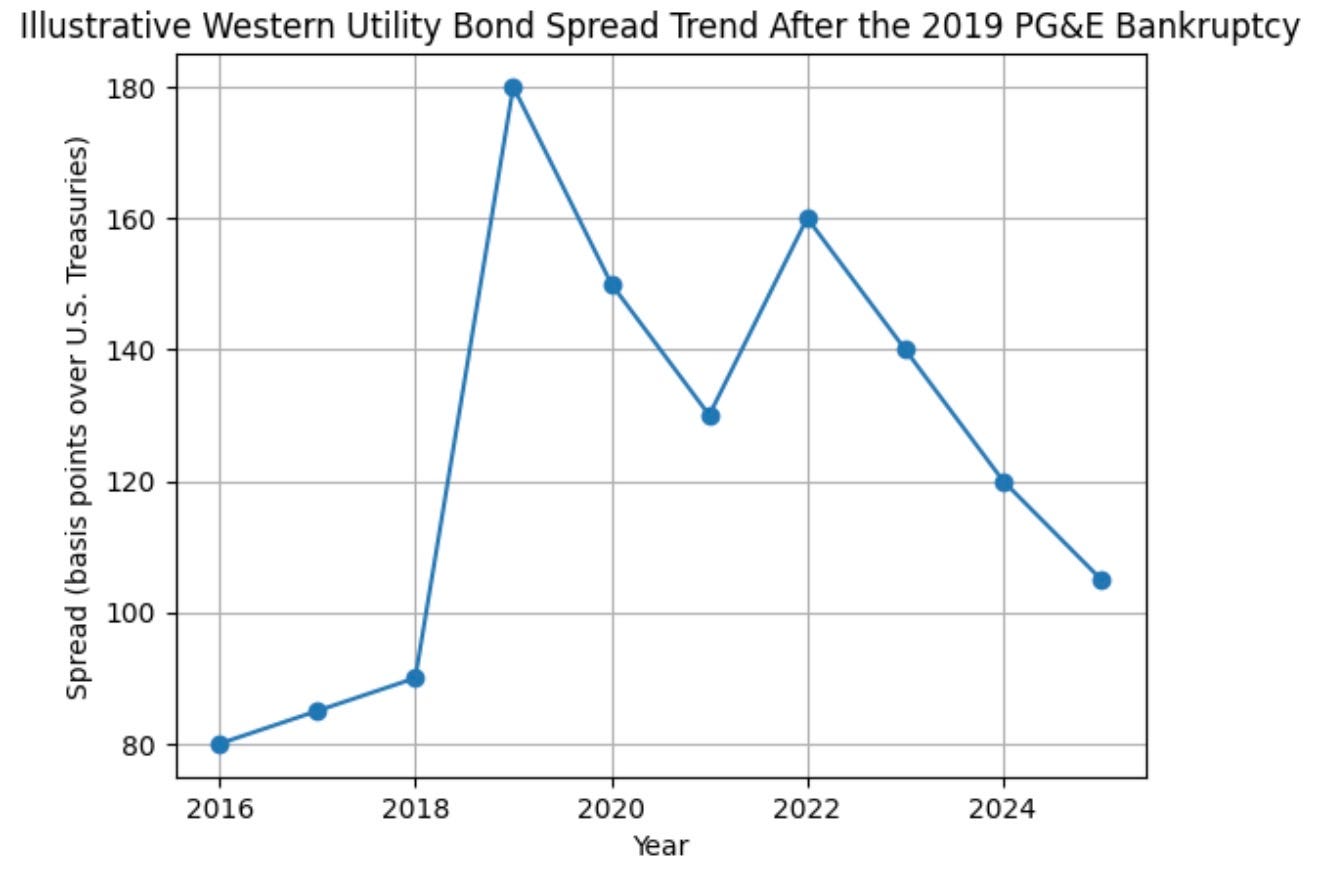

4) The New Tell: Credit Markets Have Set a New Floor

Was there a complete credit-market shutdown after PG&E?

No. But markets repriced the sector.

Spreads later compressed — but they remain higher than the pre-wildfire era for now.

The market moved in stages:

Shock repricing

Policy stabilization

A search for equilibrium

Western utilities now carry a wildfire premium.

Consider a recent Southern California Edison financing:

Yield to maturity: 4.825%

Spread: ~103 basis points over Treasuries

Credit markets are open.

But price based on a structured wildfire finance regime.

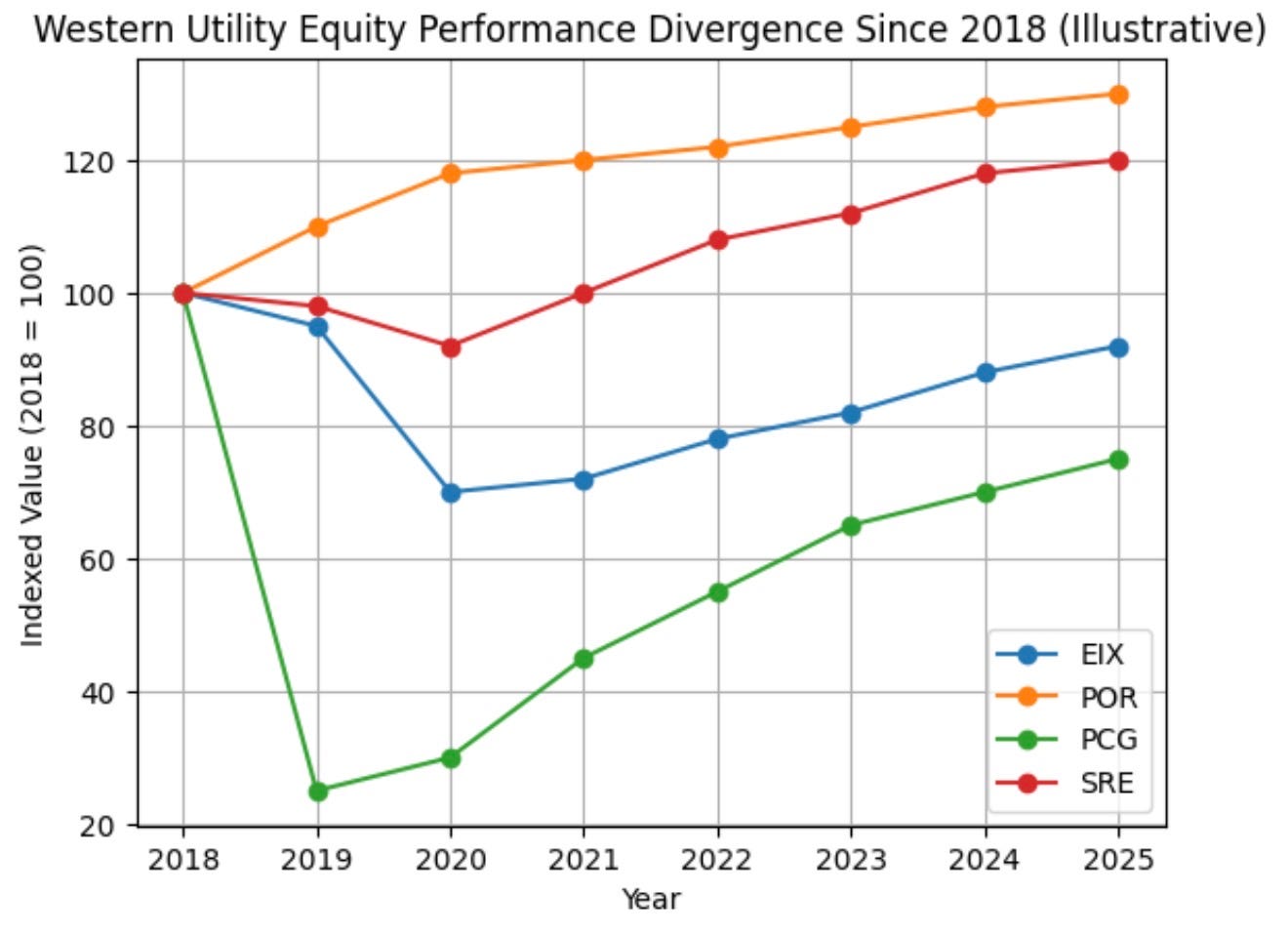

5) Equity Markets: Where the Risk Appeared First

Equity markets were the first place wildfire risk surfaced.

Some companies stabilized.

Others haven’t fully recovered.

The market began distinguishing between utilities with:

containable wildfire exposure

and open-ended catastrophe risk

6) The Human Flaw: Equity’s Normalcy Bias

Credit markets think in terms of term limits, collateral, and recovery hierarchy.

Equity does not.

Utility equities historically behaved like slow-compounding bond substitutes.

But wildfire liabilities do not arrive smoothly.

They arrive as step-function shocks:

wind event

ignition

litigation

jury verdict

Suddenly the steady dividend machine becomes a fight over who pays.

Which returns to the only question that matters:

Is the risk socialized or not?

And if it is — through whom?

Ratepayers.

Taxpayers.

Insurers.

Equity investors.

Policy is attempting to prevent two outcomes simultaneously:

a grid starved of capital investment

rate shock from citizens refusing to pay

That tension now defines the western utility sector.

7) The Forward Signal: Certification as a Credit Covenant

In California, wildfire safety certification is quietly becoming something resembling a credit covenant.

Approval of mitigation plans enables utilities to access:

regulatory protections

wildfire funds

securitization structures

Without certification, those protections weaken dramatically.

Which leads to the most important regime shift of all:

The cost of capital is now tied directly to fire governance.

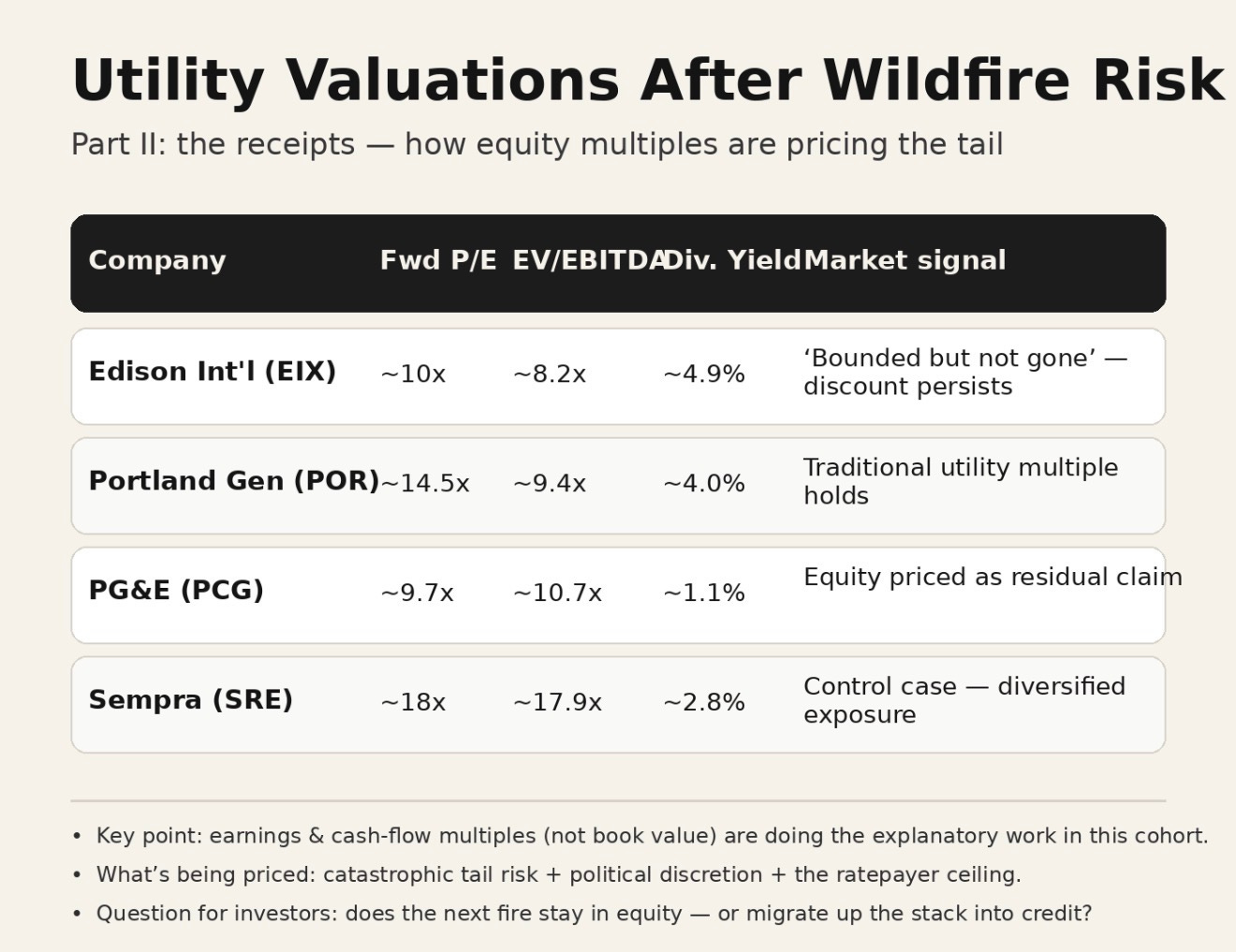

The Market’s Verdict

Utilities perceived to have containable exposure retain traditional multiples, while others trade at persistent discounts.

It prices it in:

earnings multiples

dividend yields

and the probability that catastrophe migrates up the capital stack.

The Takeaway

Berkshire did not sell because utilities stopped being “steady and dull.”

It sold because a new variable entered the model:

uncapped contingent liability that refuses to respect regulated returns.

When that variable becomes large enough, an allocator build to last protects the fortress.

California’s response is now the template:

certification

wildfire funds

securitization

A financial architecture designed to keep capital flowing into a grid that must expand, harden, and electrify.

Credit markets reflect this reality.

First came panic.

Then repricing.

Now a search for an new equilibrium.

A premium that says:

“We will lend — but we are not pretending.”

And equity remains the crumple zone.

At least until the next fire forces the system to decide again who ultimately pays.

That is the underwriting now.

If you found this analysis useful, consider subscribing to The Rustbelt Reader.

This publication focuses on the intersection of infrastructure, credit markets, energy systems, and the long economic cycles shaping the American economy.

Utilities, grids, and capital markets may seem technical — but they determine how fast the country can build, electrify, and grow.