When the Anchor Broke

Paul Volcker, Bretton Woods, and the long shift from gold discipline to real-world constraint

Act I: System Under Strain

The phone would ring early.

Before Paul Volcker left for the Treasury, foreign central banks were already watching the dollar—sometimes quietly asking for gold. By the early 1970s, those calls came too often.

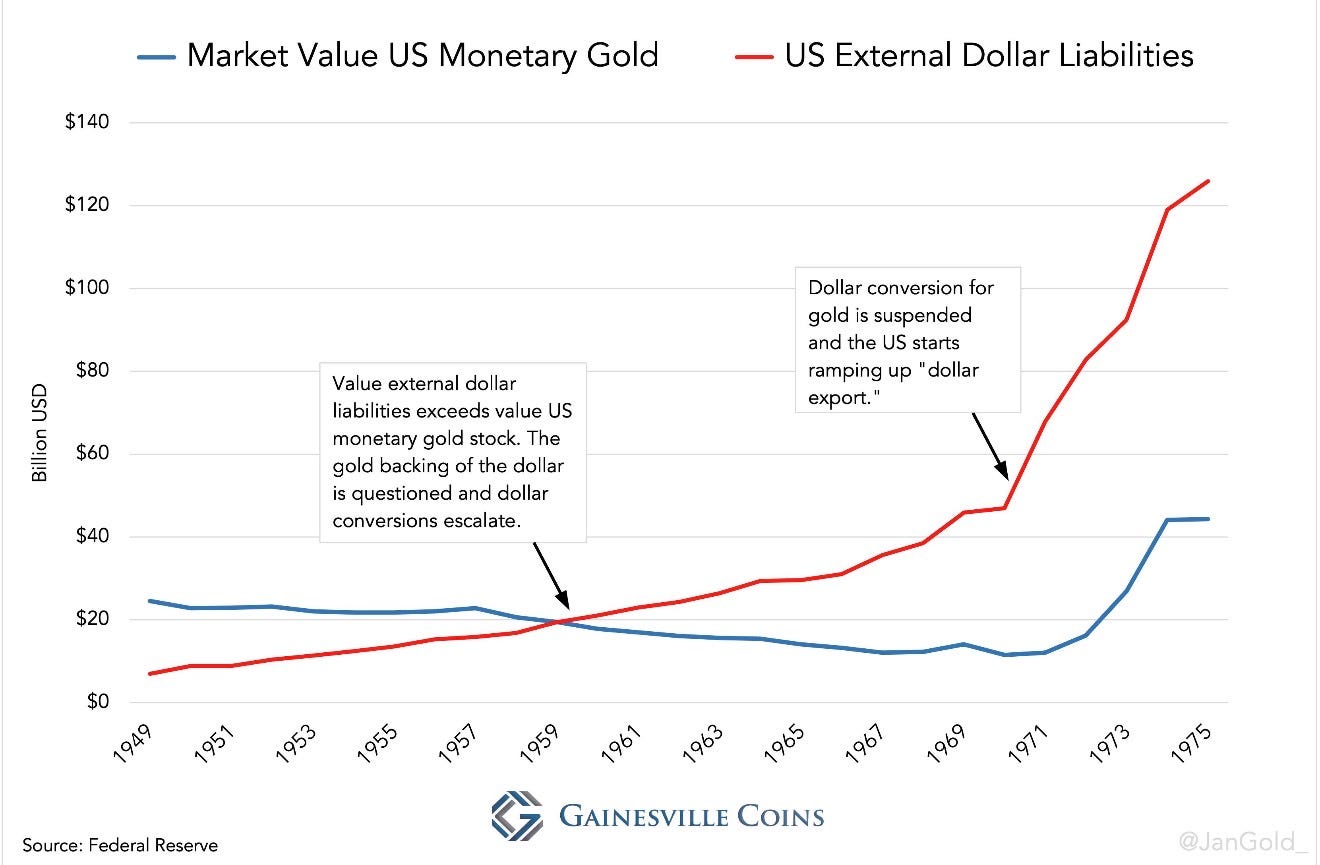

At the center of Bretton Woods was a simple bargain. Foreign governments accumulated dollars through trade and capital flows and, in principle, could exchange them for gold at $35 an ounce.

That meant U.S. deficits did not disappear. They accumulated abroad as claims on American gold.

As long as those claims were credible, the system held. Over time, they grew larger than the gold behind them. The problem was not hidden. It was embedded in the balance of payments.

At the same time, the United States was trying to do something historically familiar: sustain global leadership, expand domestically, and finance a war abroad without fully paying for any of it.

That is what historians call imperial overstretch: when a leading power’s external commitments begin to outrun its economic capacity and political willingness to sustain them.

Inside the system, the strain was visible. Outside, it was still tolerated.

Act II: Crisis and Decision

By 1971, the pressure had become acute.

Foreign governments were no longer just holding dollars. They were acting on their doubts. Requests for gold intensified. Confidence weakened. The system was being tested at its point of constraint.

Inside the administration, the debate narrowed.

Arthur Burns favored negotiation. John Connally believed the United States had to act first. Volcker understood both positions, but he also understood something more basic: preserving the system required accepting a degree of discipline the political system no longer wanted to bear.

So the United States moved first.

The gold window closed.

What followed was not a negotiated adjustment but a forced reset—suspending convertibility, adding import surcharges, and trying to regain control before the system broke on its own terms.

Act III: Temporary Stabilization

In the short run, the strategy worked.

Markets stabilized. Exchange rates were realigned. Cooperation appeared restored.

But something essential had changed. What emerged was not a repaired Bretton Woods system. It was a system that still functioned, but no longer disciplined.

Volcker later put it plainly: what was missing was not a mechanism, but a commitment.

That was the real loss.

Act IV: Volcker Becomes the Constraint

This is the missing turn in the story.

In 1971, Volcker helped close the gold window. He knew exactly what was being lost: the system’s external discipline.

What followed in the 1970s was the consequence. Without gold to anchor the system, the constraint shifted to domestic prices. Inflation rose. Energy shocks hit. Industrial America absorbed the strain. The problem no longer appeared as a run on gold. It appeared as a breakdown in the purchasing power of money.

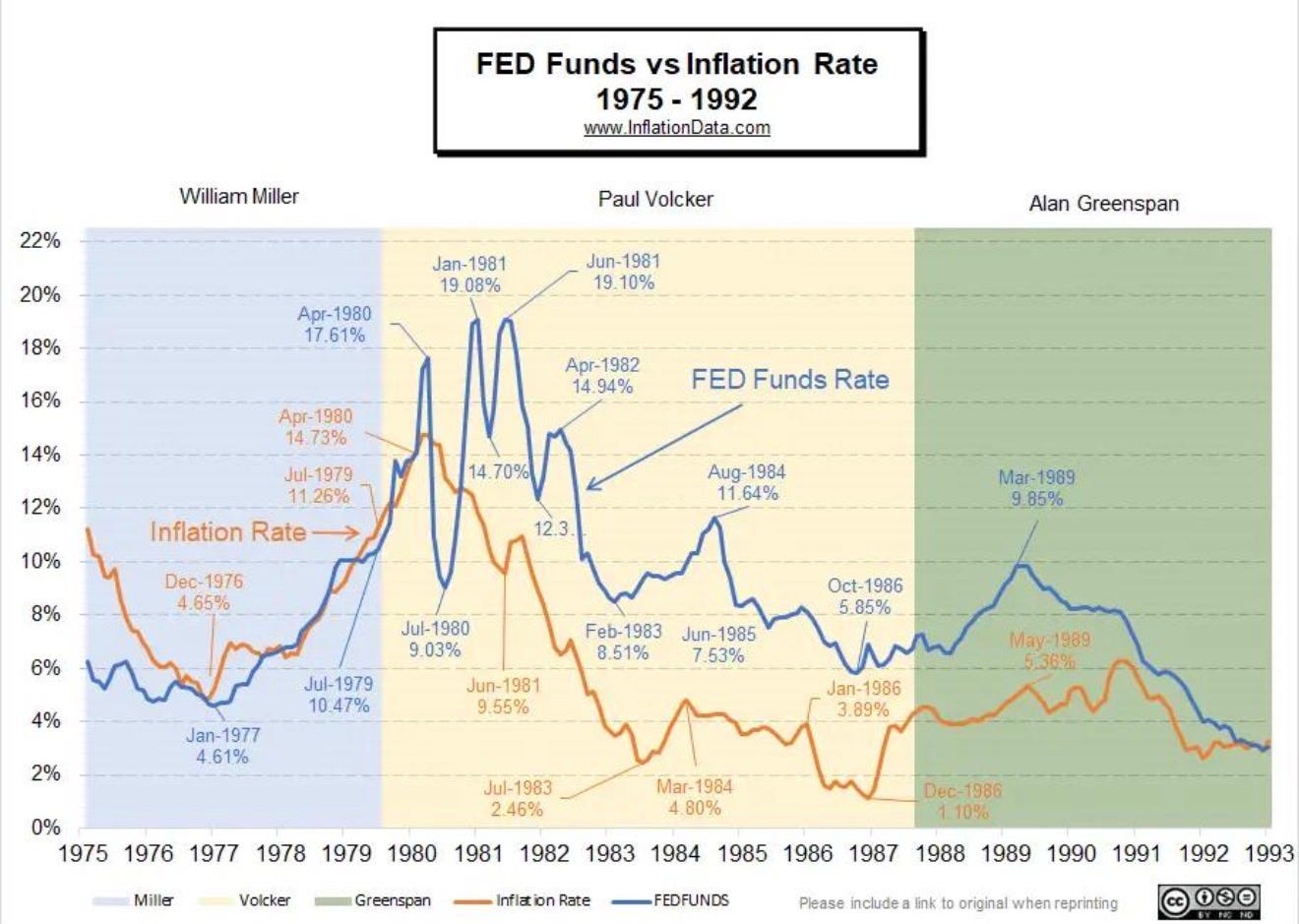

By the time Volcker became Fed chair in 1979, he was no longer managing the Treasury side of the story. He was now responsible for imposing the discipline that Camp David had helped remove.

He did it brutally.

He drove interest rates toward 20 percent, induced a recession, and broke the psychological habit of inflation. In effect, he became the internal discipline the fiat system required. He was the human version of the constraint policymakers had tried to escape in 1971.

That is what makes his arc so powerful. The young Volcker witnessed the end of external restraint. The older Volcker had to restore restraint through pain.

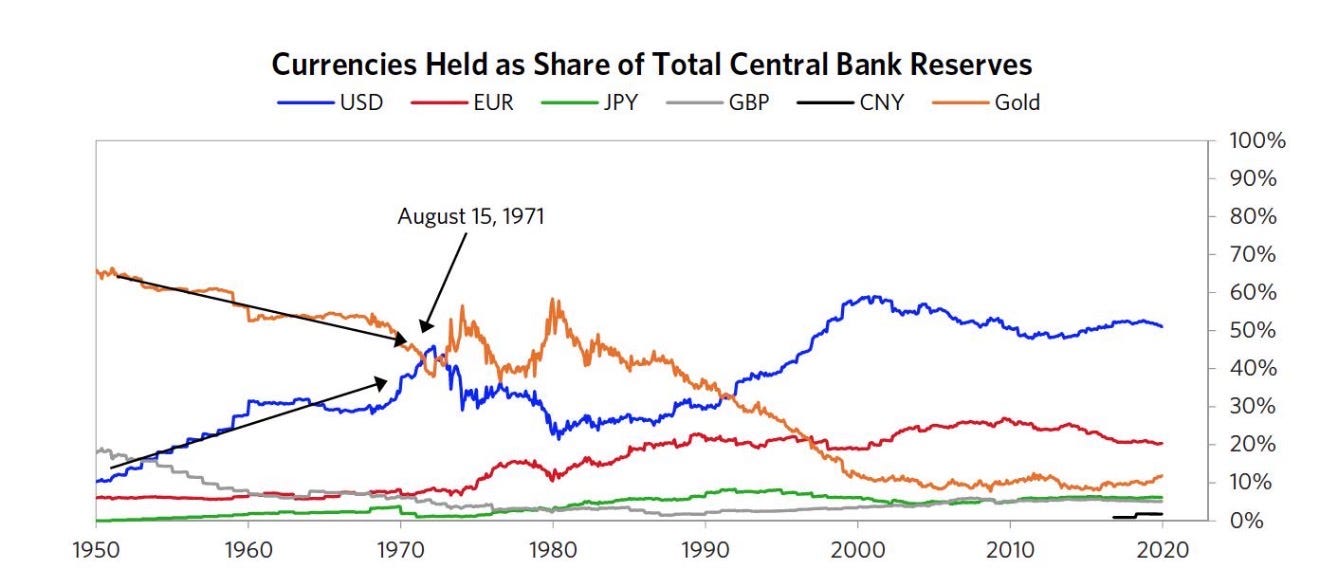

Act V: Bretton Woods II — The Long Dollar Era

After inflation was broken, a new order took shape.

What later became known as Bretton Woods II was a dollar-centered system without gold, but not without structure. Oil exporters recycled petrodollars. Later, export powers like China accumulated massive dollar reserves and invested them into U.S. Treasuries and other financial assets.

The United States supplied the reserve asset. Surplus economies supplied goods, ran surpluses, and recycled savings back into the American system.

It worked because it paired fiat flexibility with globalization.

Cheap goods helped suppress inflation. Foreign demand helped finance U.S. deficits. The system looked stable for a long time.

But the constraint had not disappeared.

It had been deferred.

Act VI: The Return of Constraint

That brings us to the present.

For decades, policymakers could manage the financial side of the system—interest rates, liquidity, exchange markets, balance sheets. But the real side remained outside their control: energy, food, metals, shipping, and security.

That is why the more recent “Bretton Woods III” framing matters. It suggests that the next constraint may not arrive through gold or even finance first, but through commodities, trade routes, and access to real resources.

Money still matters.

But so do oil, wheat, copper, freight, and geopolitical protection.

You can print money.

You cannot print oil.

Inflation, in that sense, is not just a monetary event.

It is the real world pushing back.

Act VII: The Enduring Question

Looking back, Volcker asked something simple and uncomfortable:

Why had the United States shown so little sustained commitment to the discipline required by the system it led?

Part of the answer was what policymakers once called benign neglect—the belief that external imbalances could be tolerated while domestic priorities took precedence.

For a time, that worked.

Then the system absorbed the cost.

That is the enduring pattern. A dominant power gains flexibility. Flexibility becomes habit. Habit becomes policy. The constraint does not vanish. It returns in a different place.

The last time the system was tested, allies asked for gold.

The next time, they will not need to.

They will adjust more quietly—through supply chains, real assets, and the things fiat cannot print.

1971 did not end constraint. It changed where the constraint lives.

Thanks for reading. If you found this valuable, please consider subscribing.

In the next piece, we’ll look at what it actually took to restore discipline once it was lost—how inflation in the 1970s forced policymakers into choices they had spent a decade trying to avoid.

A great piece. I wrote a lot about this on Facebook after the 2008 Crash. Whilst it impacts U.S. citizens, the country is resource rich, relative to Europe. The institutionally socialist European Union , in a resource poor continent, serially refuses to face the truth about the $ which backs its own €. The former British Prime Minister Liz Truss understood, but was undermined by our own Bank of England socialists. The new Restore party's Rupert Lowe understands too. In the long term we must all trim our cloth to suit our purse.

great insights -thanks!