Two Hands on the Same Lever

A respected critique of “activist” Treasury issuance turns out to be one half of a larger story — and the other half is who’s left to buy the debt.

MACRO & MARKETS · JUNE 2026

There is a paper that has circulated quietly among rates desks for the better part of two years, and it deserves a wider reading — not for the controversy it caused, but for what it accidentally proves.

The argument, made by Stephen Miran and Nouriel Roubini, is called Activist Treasury Issuance. Its claim is narrow and sharp: that the Treasury, by tilting its borrowing toward short-dated bills rather than longer-dated coupons, can suppress the term premium — the extra yield investors demand to lend long — and thereby ease financial conditions without the Federal Reserve lifting a finger. They put the effect at roughly a quarter-point of suppressed long-term yield (a range of 14 to 40 basis points), the equivalent of about a percentage point of Fed cuts. Stealth easing, run from the issuance window instead of the monetary one.

It is a good paper. What makes it worth returning to is that it confirms, almost inadvertently, the spine of an argument this letter has been making from the opposite direction — and that the two, set side by side, describe something more unsettling than either does alone.

THE MECHANISM BENEATH BOTH

Strip the Miran paper to its foundation and you find a single proposition: the Treasury is a price-insensitive seller. It issues not because yields are attractive but because Congress has already spent the money — the size of the borrowing is set by the deficit, not the market. The buyers are price-sensitive: they will absorb the paper, but only at a yield that makes them sell something else to do it. From which Miran draws the conclusion that matters: the market-clearing yield is whatever it takes to induce that switch.

Readers of this letter will recognize that sentence, because we have been building on it under a different name. The Clearing Price thesis holds exactly this — that there is no “natural” yield on government debt, only a clearing price, the level at which a price-insensitive issuer meets whatever demand remains. Miran arrives at the engine from the supply side; we arrived from the demand side. It is the same machine.

That agreement kills a comfortable myth — the idea that the ten-year yield reflects some deep equilibrium of growth and inflation that the bond market “knows.” It doesn’t. That notion is itself a managed-era promise, the financial cousin of the lifetime pension and the secure plant: an arrangement that feels permanent right up until the support beneath it is tested. The yield is simply the price at which the last necessary buyer can be coaxed in. Everything else is narrative laid over that single transaction.

THE TWO HANDS

Here is where the two analyses combine into something neither contains by itself. If the clearing price is set by a price-insensitive issuer meeting price-sensitive demand, then there are two distinct ways to move it — and right now both are being worked, in opposite directions.

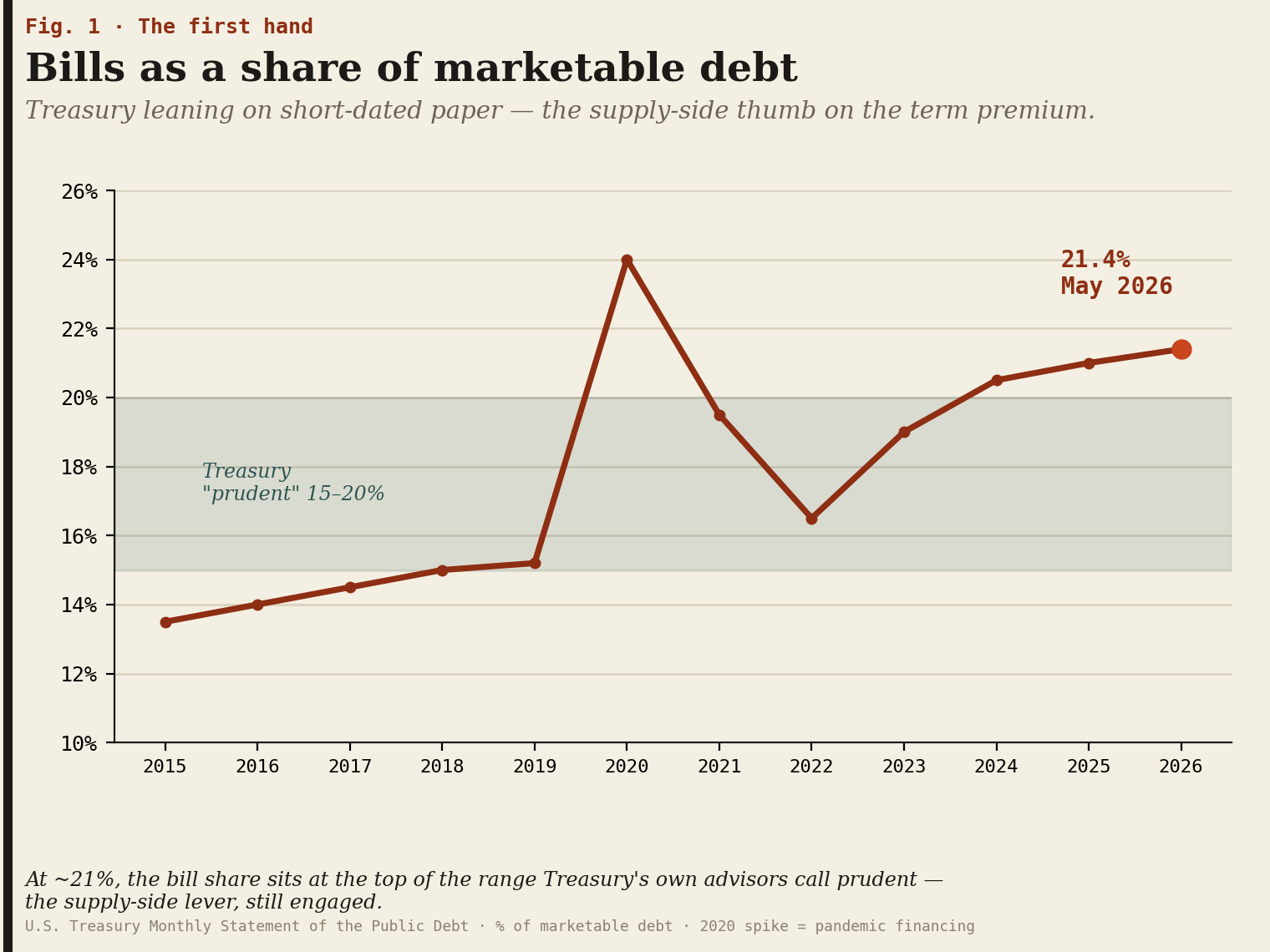

The first hand is the one Miran describes. The Treasury can hold the clearing yield down by skewing issuance toward bills, starving the market of the long-dated paper that carries term premium. This is a government thumb pressing on the scale, and the data show the thumb is still there: as of May 2026, bills make up roughly 21 percent of marketable debt — the high end of the range Treasury’s own advisors have historically called prudent — while the ten-year term premium sits near 0.67 percent, positive but plausibly lighter than a debt held by the public of some $31 trillion (with gross debt past $37 trillion and climbing toward $40 trillion by autumn) would otherwise command.

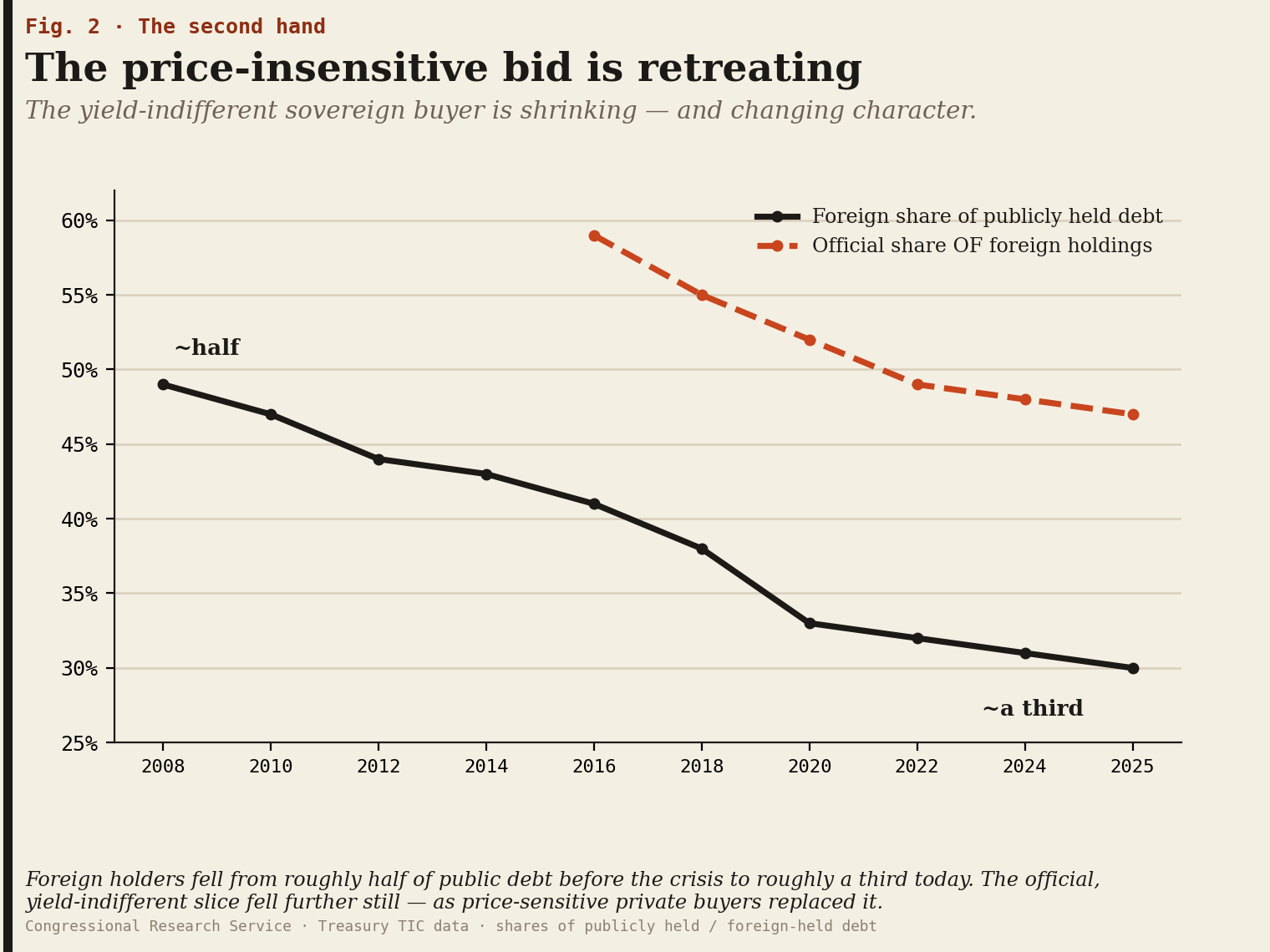

The second hand is the one we have been tracking, and it deserves the same hard numbers. The buyers who used to hold the clearing yield down — foreign central banks, reserve managers, the great price-insensitive official bid that absorbed American debt for two decades without much regard for yield — are turning price-sensitive, and stepping back. The foreign share of publicly held debt has fallen from roughly half before the financial crisis to roughly a third today — and the part that matters most has retreated furthest: foreign official holdings, the genuinely yield-indifferent sovereign bid, peaked around 2020 and have been flat-to-falling since, their share of total foreign Treasury holdings sliding from nearly 60 percent to under 50. The slack has been picked up by price-sensitive buyers — private funds, money-market vehicles, leveraged accounts — who demand a yield to show up. The structural demand that once flattered the clearing price is not merely thinning; it is changing character, from indifferent to exacting.

Set the two hands together and the picture sharpens into something genuinely uncomfortable. The clearing price of American debt is being propped down by an issuance tactic at the very moment the structural demand that used to prop it down is eroding. One support is artificial and temporary; the other is real and fading. Miran sees the first hand and warns it is a trick. We have been watching the second hand and warning it is structural. Both are right, and the danger is in the overlap: the trick is buying time against the erosion, and tricks of this kind have a way of running out precisely when they are needed most.

THE IRONY IN THE CHAIR

There is a turn here worth pausing on. The critique of activist issuance was written outside government — Miran and Roubini published it at a hedge fund in 2024. Its lead author then spent eighteen months inside the policy apparatus the paper helps explain: first as the administration’s chief economist, then briefly on the Federal Reserve Board, before returning to the private sector in mid-2026. So the framework traveled a full circuit — from the outside, through the policy machine whose issuance and rate regime it describes, and back out again.

Meanwhile the Treasury Secretary — a different principal, and the one actually setting issuance — has built his public framing around a phrase that is, almost word for word, the doctrine that critique held up as the honest alternative.

That phrase is “Regular and Predictable.” He has enumerated its virtues: transparency, reduced rollover risk, the avoidance of a supply premium, the credibility of the risk-free rate. He has deferred increases in coupon auction sizes “for at least the next several quarters,” and his borrowing advisory committee has flagged that the coupon increases the math eventually requires are a story for fiscal 2027, not today.

So the honest question — and it is a question, not an accusation — is whether “Regular and Predictable” is a genuine return to disciplined issuance, or activist issuance with better public relations and a later invoice. Continuing to lean on bills while postponing the coupon supply that would actually test the clearing price is, functionally, the same hand on the same lever, whatever it is called. The critique of the tactic and the continuation of the tactic are, for now, coexisting in the same policy regime.

The test is not rhetorical, and it has a date attached. It arrives when the deferred coupon issuance can no longer be deferred — when the bills have to be turned into bonds and the long end has to absorb supply at whatever yield clears it. That is the moment the second hand gets put to the demand it has been spared. On current trajectories, that moment lives in 2027.

WHY THE MARKET ISN’T PRICING IT

The obvious objection to all of this is the same one leveled at every structural warning: if it were true, the market would already have priced it. Yields would be higher now.

It is worth noting that Miran’s own answer to this objection is, almost exactly, the answer this letter gave its readers last week about a different subject. Markets, he argues, do not price a certain-but-untimed event until a catalyst drags it into the investable horizon. He reaches for the 2013 taper tantrum and the long-flagged exhaustion of the entitlement trust funds — events everyone knew were coming, that the market nonetheless ignored until a trigger made them tradable.

That is the identical mechanism we described in arguing that the coming shelter reacceleration is already determined but not yet priced: a future sitting in the data pipeline, discounted by a market that won’t act until something dates it. Two different theses — the clearing price of debt, the floor under inflation — resting on the same epistemic foundation. The market systematically underprices certain-but-untimed structural shifts, and it does so not from stupidity but from the way pricing works: conviction requires a catalyst, and the catalyst always arrives after the certainty.

This is the quiet thread connecting everything we write. The managed world — managed yields, managed inflation, managed expectations — does not end with a crash. It ends when a price that was being held by an eroding or artificial support gets discovered, all at once, because something finally forced the discovery.

WHERE IT LANDS

Both hands push toward the same destination, which is why this matters beyond the elegance of the framework. Activist issuance is inflationary in the present, because it blunts the monetary restriction that would otherwise bite. A fading foreign bid is inflationary structurally, because it raises the clearing yield and forces more dollar issuance into a thinner pool of willing buyers. The supply-side tactic and the demand-side erosion arrive at the same place: a higher resting rate of inflation, and a higher resting cost of money — the same place the components of the price index already pointed.

The Rust Belt has watched this kind of transition before, at a smaller scale and a lower altitude. A managed promise — the pension, the plant, the order book — gave way, not gradually but suddenly, to a discovered reality, the day the support that had been quietly holding it up was finally tested and found absent. What Miran describes at the Treasury’s issuance window, and what we have described at the foreign bid, is the same passage from managed to discovered, now running at the level of the sovereign itself.

The clearing price has two hands on it. One is buying time. The other is letting go. The interesting question is not whether they meet, but when — and which one the market is finally made to notice first.

I spent 30 yrs in the bond market and I still think Central Banking is indistinguishable from Central Planning.

Add to this another important component of demand - The Fed….Kevin Warsh is anti QE and will change the approach of the Fed when crisis hits…..the Fed balance sheet will not be there with the same ease as in the last few Fed chairs…