Too Small to Succeed

Bessent on Private Credit, Deposit Hierarchies, and the Systems Test Facing American Banking

“We’ve Gone From Too Big to Fail, to Too Small to Succeed.”

- Scott Bessent, Dallas Economic Club (February 2026)

That line captures the structural shift now underway in American finance.

Over the past decade, the system has tilted. Private credit has expanded outside the regulated perimeter. Community banks have declined in number and relative weight. Deposits, particularly large uninsured balances, have shown a tendency to concentrate at the very largest institutions during periods of stress. Meanwhile, the labor market sits in an unusual posture — cautious, “slow to fire, slow to hire,” waiting for capital investment to either accelerate or stall.

In a recent interview, Treasury Secretary Scott Bessent described this environment as a rebalancing. The implication is that policy adjustments — from bank capital rules to deposit insurance thresholds — can restore equilibrium.

The deeper question is whether this rebalancing reduces systemic fragility or simply shifts it from one part of the architecture to another.

To understand that, you have to start with private credit.

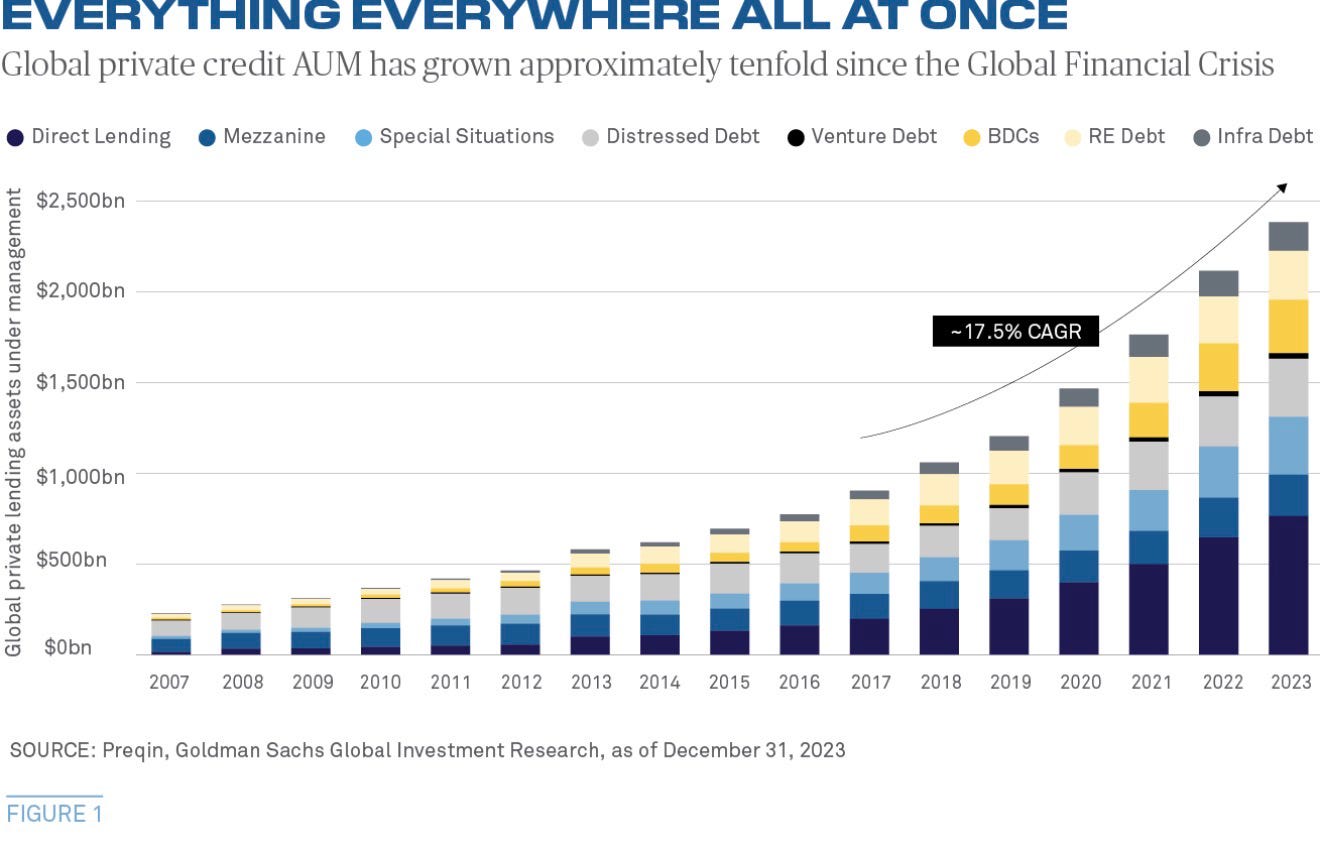

Private Credit: Migration, Not Magic

After Dodd-Frank, regulated banks faced tighter capital requirements and heavier supervision. Lending did not disappear. It migrated.

Private credit stepped into the vacuum.

Over the past decade, private credit assets under management have expanded dramatically, filling lending gaps left by the regulated system.

Bessent calls this regulatory arbitrage. When capital becomes expensive inside the formal banking system, it seeks lighter terrain.

In good times, that flexibility is efficient. In stress, the key question is where the risk ultimately settles.

Treasury’s effort to potentially unlock as much as $2.5 trillion in additional regulated bank lending capacity signals an attempt to rebalance the system — restoring competitiveness to supervised institutions without dismantling discipline.

The test is not whether private credit is good or bad. It’s whether risk is priced clearly or simply displaced.

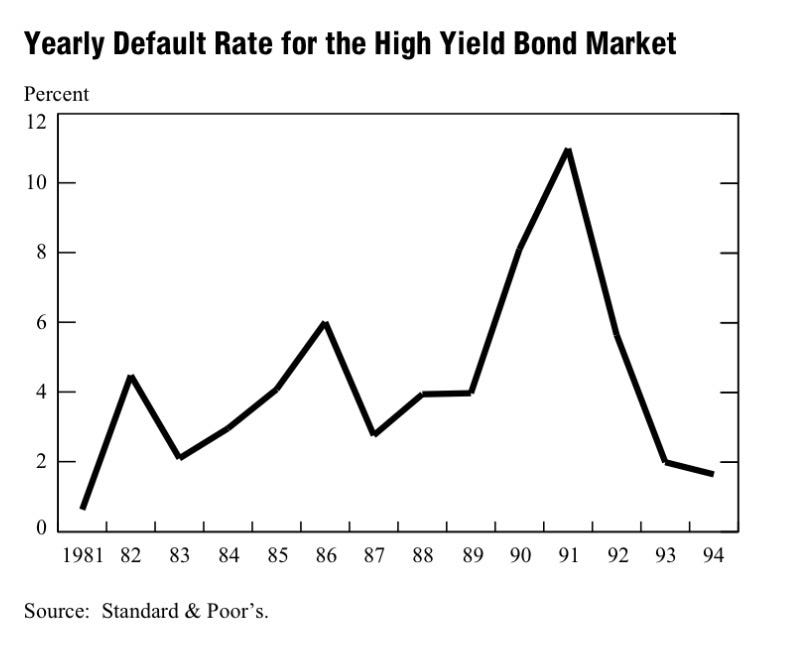

A Historical Parallel: The Junk Bond Wave

This isn’t the first time credit migrated when traditional lenders stepped back.

In the early 1980s, after the Volcker rate shock and mounting balance-sheet stress, banks became capital-constrained and defensive, the high-yield bond market scaled rapidly to finance leveraged buyouts and restructurings.

The capital wasn’t inherently reckless — it was innovative. It funded borrowers the traditional system wouldn’t.

But it was also largely untested by a true downturn.

As the market grew, discipline softened. Underwriting loosened, covenants weakened, and incentives rewarded volume. When the cycle turned in the late 1980s and early 1990s, defaults surged and the weakest deals were exposed. The market survived — but only after a hard repricing and a painful round of restructuring.

Private credit today isn’t junk bonds in 1988. But the rhyme is structural: when the perimeter tightens, credit moves. The real test is whether standards hold when growth slows and refinancing windows narrow.

And while credit has been migrating outside the regulated perimeter, the regulated banking system itself has been thinning underneath the largest institutions.

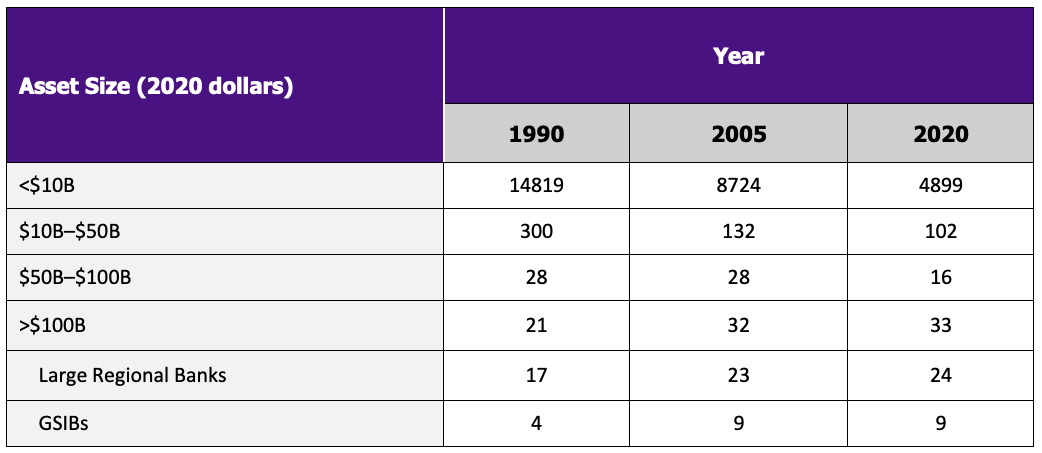

The Structural Thinning

The American banking system didn’t merely consolidate after 2008. It thinned.

Since 1990, the number of banks under $10 billion in assets has fallen by roughly two-thirds. Thousands of small institutions — the traditional lenders to local businesses, farms, and commercial real estate — have disappeared through merger or failure.

Mid-sized banks have also contracted sharply.

At the top of the system, however, the trend runs in the opposite direction. The number of institutions above $100 billion in assets has increased. Globally systemically important banks (G-SIBs) have more than doubled.

This is the backdrop to Bessent’s “too small to succeed” line.

The issue is not simply the 2023 acceleration in deposit migration following the collapse of Silicon Valley Bank. It is that the institutional base beneath the largest banks has been eroding for three decades.

Community banks have not just faced competition. They have faced structural compression — regulatory burden, funding volatility, and scale disadvantages.

Bessent emphasizes that community banks matter because they are embedded in their local economies. Unlike distant balance-sheet allocators, local bankers understand the businesses, farms, and commercial properties they finance. Relationship capital still matters.

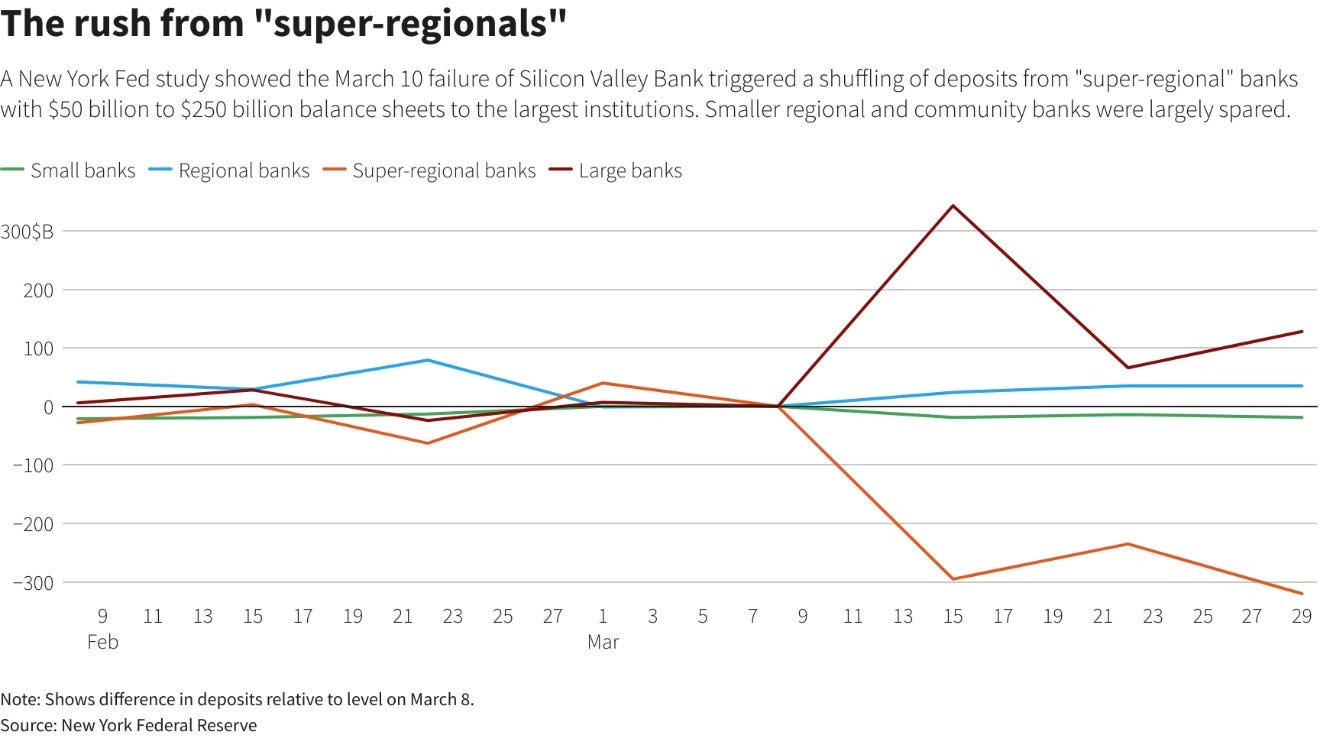

The Deposit Hierarchy

The 2023 episode did more than trigger isolated failures. It clarified a hierarchy.

Large, uninsured balances — corporate treasurers, venture funds, high-net-worth accounts — moved first. They did not simply flee “small banks.” They climbed the perceived safety ladder.

Even U.S. Bank, the fifth-largest institution in the country, saw deposits migrate toward JPMorgan Chase during the stress. In moments of uncertainty, sophistication concentrates.

Retail deposits behaved differently. Smaller operating accounts were comparatively stable. Households and local businesses tend to value relationships and continuity over basis-point optimization.

But sophisticated capital prices tail risk.

That reality informs Bessent’s support for raising insurance limits on certain non-interest-bearing business accounts — potentially up to $10 million — as a way to interrupt automatic deposit concentration during future stress.

Community banks remain the economic engines of local America, driving roughly 70% of real estate, agricultural, and small business lending. If funding volatility permanently pushes deposits upward, the credit pipeline to Main Street narrows.

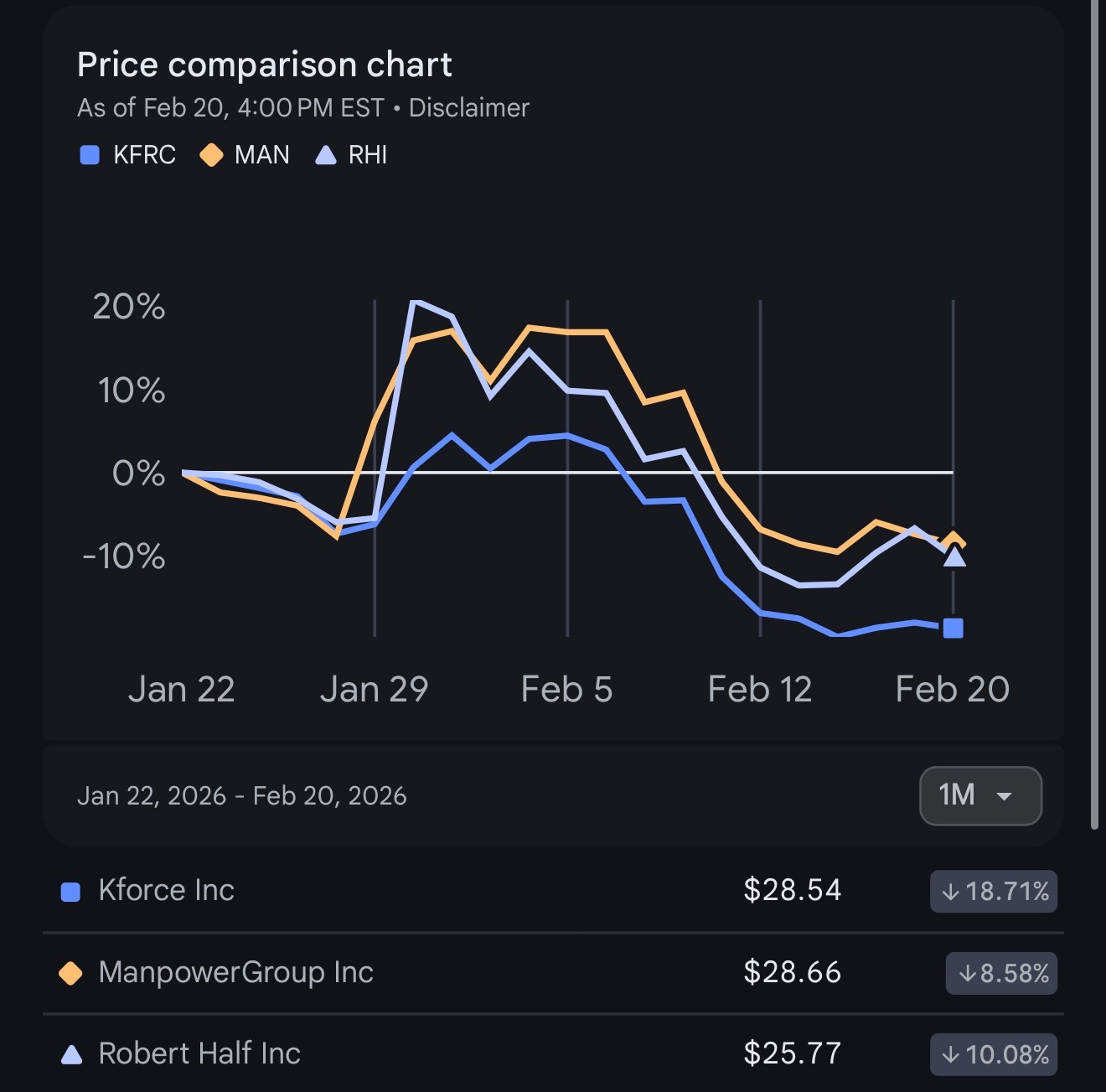

The Labor Signal

Bessent also touched on the labor market in his interview. He argues that positive equity trends in temporary staffing is a leading indicator of broader employment acceleration.

The recent data, however, is more nuanced than his optimism suggests.

Over the past month (Jan 22 – Feb 20), major staffing equities have declined sharply:

Kforce (KFRC): –18.7%

Robert Half (RHI): –10.1%

ManpowerGroup (MAN): –8.6%

Historically, staffing firms see demand accelerate before permanent hiring follows. Companies test the waters with contract labor before committing to payroll expansion.

Nonetheless, if capex growth of 12–14% in 2025 is indeed productive, job growth should follow. The market will likely signal that inflection before the payroll data does.

The issue is timing — and whether capital investment translates into durable employment or short bursts of activity.

The Realpolitik Question

This moment is not a morality play about shadow banking. It is a systems test.

Does private credit expand capital formation without embedding hidden fragility?

Does regulatory recalibration restore competitive balance without recreating moral hazard?

Does deposit insurance reform interrupt automatic concentration without socializing excess risk?

And does capex actually translate into durable payroll expansion — not just temporary staffing tests?

Factories, power plants, and logistics networks do not price off headlines. They price off predictability. Long-cycle investment requires a stable credit architecture.

Credit doesn’t disappear over cycles. It migrates. And over the past decade, it migrated from regulated balance sheets to private credit vehicles. In stress, deposits migrated from regional institutions to the largest banks.

The question is whether this reallocation reduces systemic fragility — or merely concentrates it.

If the emerging structure lowers the long-term risk premium for real-economy investment, it strengthens Main Street. If it simply shifts leverage, concentrates deposits, and delays durable hiring, the underlying vulnerability remains.

That is the audit.

If you value structural analysis over headlines — and audits over rhetoric — subscribe to The Rustbelt Reader.

We follow the receipts: in credit spreads, deposit flows, capex data, and payrolls. Because durable economies are built on structure, not slogans.

Thank you for being part of this community.

Perfect bite-sized piece, coming out at a time when private equity / credit looks wobbly due to Anthropic / OpenAI challenging those SaaS moats that the privates invested in. Thanks for helping enlighten me on this area.