President Trump’s nomination of Kevin Warsh to lead the Federal Reserve is being treated as a debate about the next rate cut. That’s too narrow. The bigger question is whether Washington is trying to buy growth with policy—or earn it through productivity.

Mr. Warsh’s recent remarks at the Reagan economic forum captured the entire doctrine in one line:

“I think we are on the cusp of another productivity boom, as long as a government does not do harm with it.”

The point isn’t that government can create the boom. It’s that policy can block it—by distorting incentives, subsidizing misallocation, or turning the central bank into a permanent market backstop.

The Supply-Side Alignment

This productivity-first posture aligns naturally with the supply-side story coming out of Treasury. Scott Bessent has argued publicly that the next leg of growth depends on investment broadening beyond a narrow set of winners—CapEx first, jobs second. Policy should clear the runway for private-sector expansion rather than smother it with friction. In Treasury remarks this month, Bessent framed the goal in operational terms: build domestically, hire domestically, and convert investment into capacity.

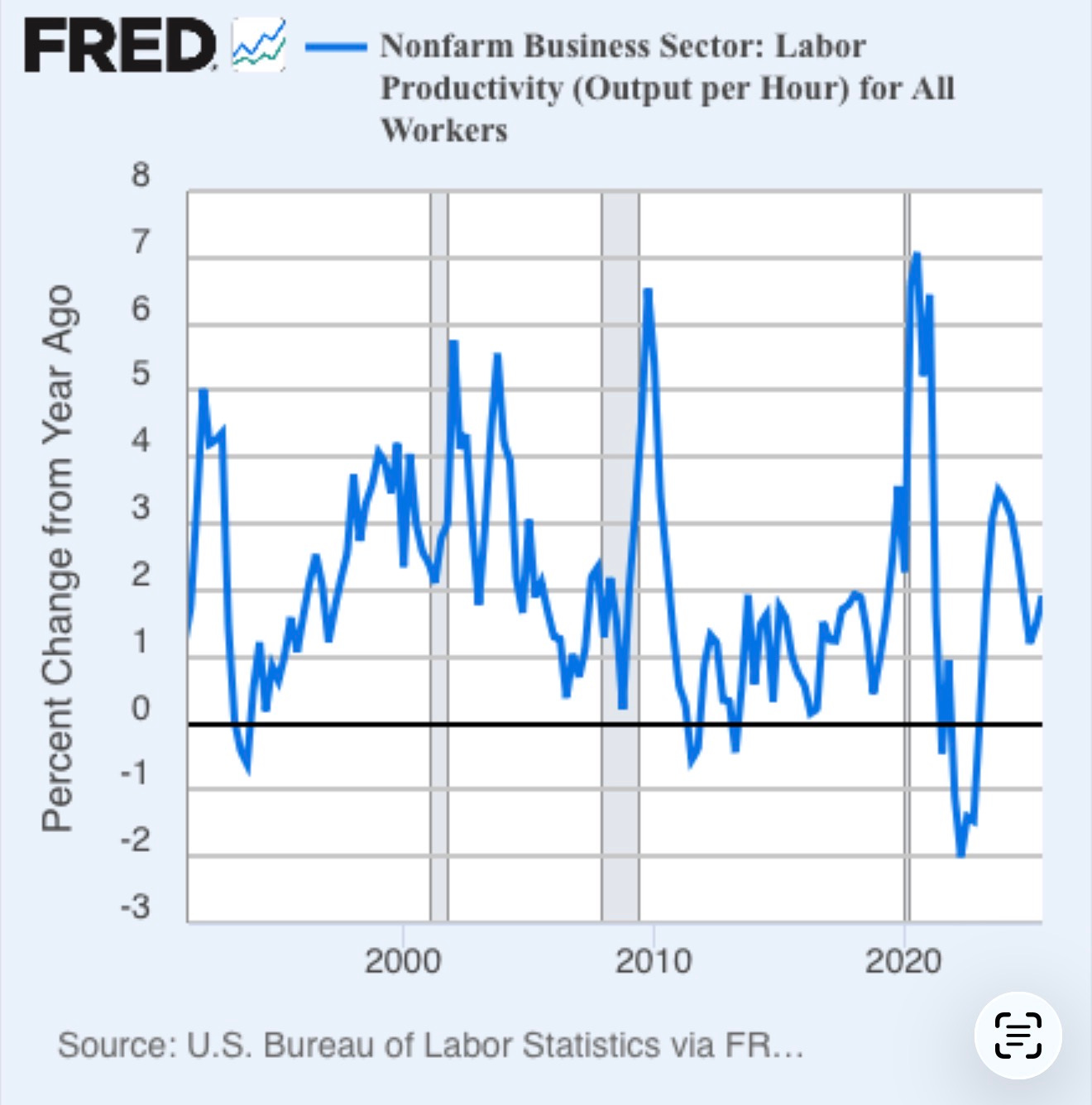

The best historical analogy is the mid-1990s—not as nostalgia, but as sequencing. In that period, productivity rose, capital spending followed, and employment gains broadened without a lasting inflation problem because supply expanded. The Fed was not trying to run markets; it was trying to avoid being the story every day. A Warsh-led Fed would aim to recreate that posture: less “promise,” more “conditions.”

Productivity is the economy’s speed limit. If it rises, you can grow without “paying” in inflation.Productivity is volatile—but regimes matter. The 1990s delivered sustained productivity gains. The post-2010 era did not. Today’s spikes show potential—but not yet a durable trend.

Plot Armor and Independence

Warsh also knows the political mechanics of independence. He offered a line that doubles as an institutional warning label:

“Doing its job and having stable prices is the Fed’s plot armor.”

In other words, independence isn’t a privilege to be asserted; it’s protection earned through competence. When inflation is contained, the Fed gets left alone. When it isn’t, the knives come out—especially if the institution has wandered into mission creep.

Markets, however, are not the markets of 1996. They are faster, more levered, and more conditioned to central-bank reassurance. That’s why investors have noted Stanley Druckenmiller praising Warsh as flexible rather than ideologically rigid. It signals a team trying to harness productivity without rebuilding the old habit of asset coddling.

Druckenmiller matters here because he’s a tape reader, not a theorist—and he’s effectively vouching that Warsh understands the feedback loops.

The Countercase: “1999 With Better Branding”

The strongest critique is that “boom” talk encourages leverage, and leverage encourages fragility. In manic markets, even a doctrine meant to reduce distortions can be interpreted as an all-clear to chase the next momentum trade, turning tech optimism into a speculative bubble.

The Rebuttal: Anti-Bubble By Design

But that critique mistakes Warsh’s premise. His point isn’t “growth at any price.” It’s “stop subsidizing misallocation.” The goal is to raise the burden of proof for capital—so returns come from productive investment, not from front-running the next policy rescue.

A Warsh Fed would force that distinction into the open: fewer implied guarantees, fewer attempts to smooth every bump in asset prices, and a renewed insistence that productivity—not permanent monetary anesthesia—has to carry the next expansion.

Rustbelt Reader — Reflections

The Exit Plan: Markets are manic. When the signal turns unmistakable, it won’t be a “rotation.” It’ll be an exit plan.

Follow the Tape: If CapEx turns into broad jobs, the thesis is real. If it stays narrow and financial, it’s 1999 with a new slogan.

Engineer Your Balance Sheet: If you’ve made serious money in the melt up, shift from maximizing upside to protecting the base—so you can get aggressive when momentum flips.

What to Watch (the “tape” checklist)

CapEx breadth: Is investment spreading beyond AI leaders into equipment, industrial buildout, energy, and infrastructure?

Jobs confirmation: Do payroll gains broaden, or does hiring stay narrow while asset prices scream “boom”?

Credibility constraint: Does inflation stay contained enough for the Fed to step back without markets demanding rescue?

The Kicker:

The Warsh Playbook assumes that if you fix the money and clear the regulatory brush, American dynamism will handle the rest. It is a high-stakes bet on the “real” economy over the “financial” one, rooted in the belief that “stable prices are the Fed’s plot armor.”

Sources

[1] Kevin Warsh — Reagan Economic Forum (video / remarks + Q&A), C-SPAN via Archive.org:

https://archive.org/details/CSPAN3_20260130_193600_Fed_Chair_Nominee_Kevin_Warsh_at_2025_Reagan_Economic_Forum

[2] Kevin Warsh, “on the Fed’s mistakes and consequences” (includes “plot armor” framing), *The Wall Street Journal* (Opinion):

https://www.wsj.com/opinion/kevin-warsh-on-the-feds-mistakes-and-the-consequences-7922f46f

[3] Stanley Druckenmiller comments on Warsh (flexibility / Greenspan-style posture; AI/productivity framing), *Financial Times*:

https://www.ft.com/content/4ec81de7-eb59-4be8-81db-bff657e6c5d3

[4] Warsh profile / broader critique of modern Fed tools and mission creep, *Financial Times*:

https://www.ft.com/content/2030acc1-4026-4ad1-81bc-12754389f71d

[5] Scott Bessent: “CapEx boom … will lead to an employment boom” (reported quote), *Yahoo Finance* syndication:

https://finance.yahoo.com/news/trumps-one-big-beautiful-bill-233118822.html

[6] Scott Bessent: the U.S. economy is “brittle underneath” / emphasis on private-sector dynamism, *Reuters*:

https://www.reuters.com/markets/us/us-economy-is-brittle-underneath-despite-reasonable-metrics-us-treasurys-bessent-2025-02-25/

[7] U.S. Treasury — press releases / official remarks hub (primary-source landing page for Bessent statements):

https://home.treasury.gov/news/press-releases

My biggest concern: will Warsh be independent, given his close ties with Trump? And always: I am not a fan of supply side economics. Instituted in the Reagan years as the central philosophy of U.S. economic policy, the gap between the haves and have nots has only widened.

Hey, great read as always. It's realy insightful to articulate the distinction between 'buying growth' and 'earning it through productivity' so clearly. The emphasis on capital expenditure as a leading indicator for sustained economic health and job creation resonates strongly with historical patern.