By Luca Pacioli | Pittsburgh PA | May 12, 2026

A strange thing is happening in the American economy.

The stock market continues climbing toward record highs. Corporate credit spreads remain remarkably tight. AI capital spending is exploding. Large technology companies are generating cash flows on a scale that would have been unimaginable a decade ago.

At the same time, the bond market is uneasy.

Treasury yields remain elevated. Oil markets remain volatile. Consumer sentiment surveys are collapsing. Housing activity is sluggish. Traditional manufacturing continues to soften. Lower-income households increasingly appear exhausted by years of inflation and higher borrowing costs.

To many observers, these realities appear contradictory.

They are not.

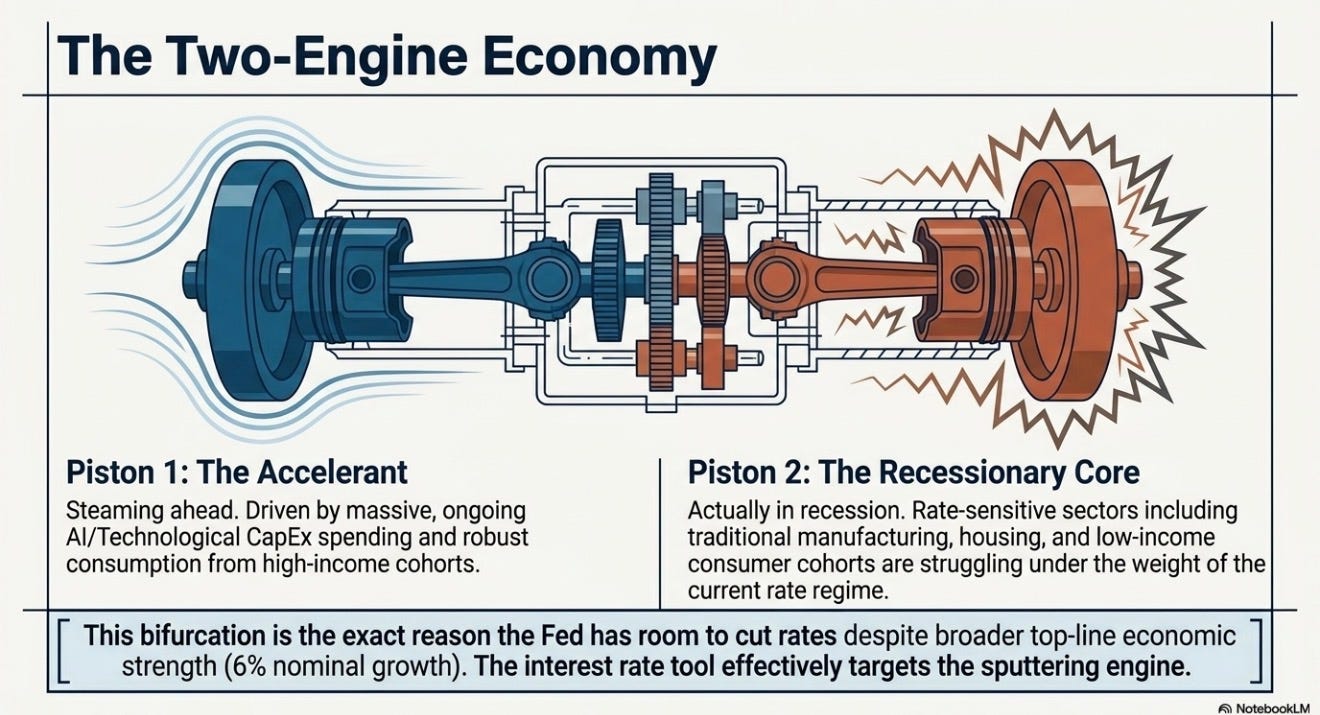

America is operating with what can best be described as a two-engine economy: one engine accelerating aggressively forward, while the other sputters under the pressure of the highest interest-rate regime in decades.

The market confusion stems from the fact that investors keep trying to force both realities into a single narrative.

But the economy is not singular.

It is bifurcated.

The Accelerant Economy

The first engine is powered by capital abundance.

This economy belongs to large technology firms, AI infrastructure spending, defense spending, high-income consumers, and corporations with significant pricing power.

These sectors are not merely surviving higher interest rates. In many cases, they are thriving.

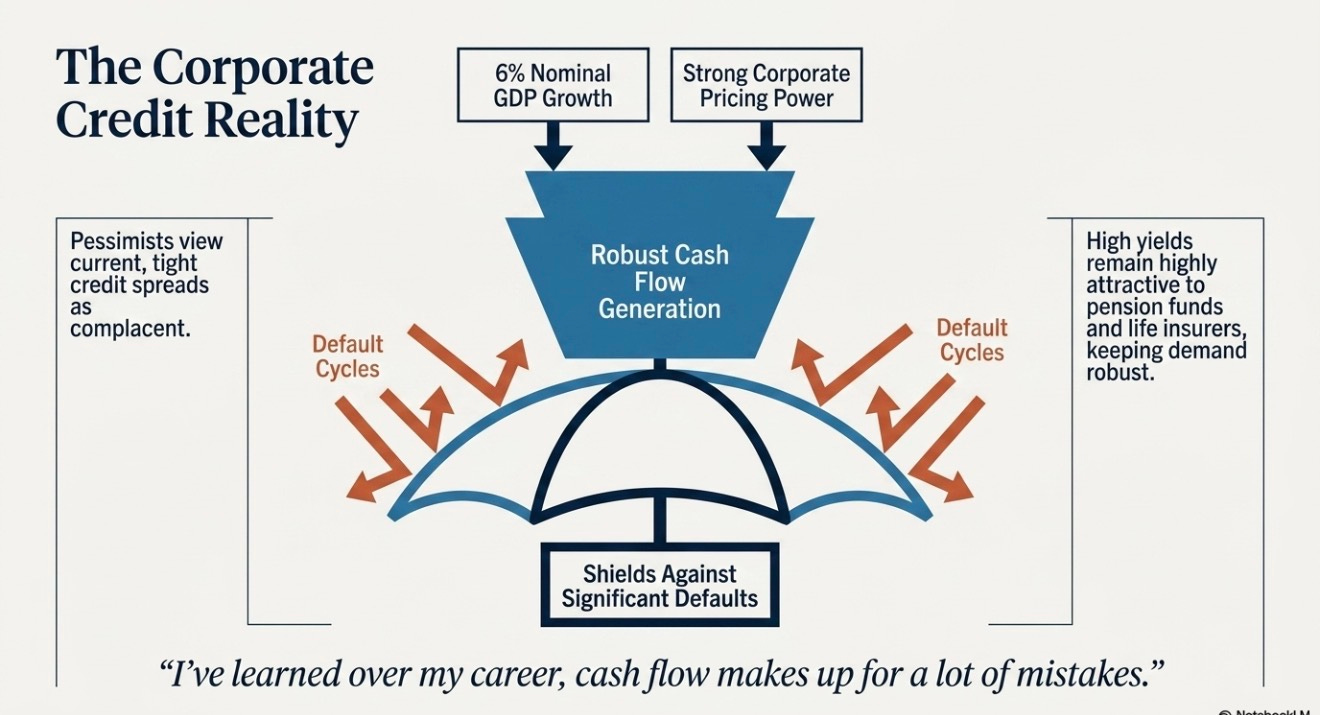

Nominal GDP growth around 6% matters enormously here. Even if real growth is slower, the combination of inflation plus economic expansion creates extraordinarily powerful top-line revenue growth for companies with scale and pricing power.

That reality explains why corporate cash flow generation has remained so resilient.

For years, investors assumed higher rates would inevitably trigger a major corporate default cycle. Instead, many large corporations refinanced debt during the zero-rate era and entered this tightening cycle with unusually strong balance sheets.

Cash flow covered a multitude of sins.

As BlackRock’s Rick Rieder recently summarized:

“I’ve learned over my career, cash flow makes up for a lot of mistakes.”

That may be the defining credit lesson of this cycle.

Pessimists continue pointing toward historically tight credit spreads as evidence of complacency. But credit markets are often less concerned with economic morality than with simple mathematics.

If companies continue generating robust cash flow, the feared default wave never fully materializes.

And that is precisely what has happened.

The Recessionary Core

The second engine tells a completely different story.

This economy belongs to rate-sensitive sectors.

Housing.

Traditional manufacturing.

Small businesses.

Regional consumers.

Households increasingly dependent on credit cards and installment debt.

These sectors are already behaving as though the economy entered recession months ago.

Higher rates are not theoretical in these industries.

They are immediate.

A mortgage rate above 7% fundamentally changes housing affordability. Elevated auto loan rates reduce purchasing power. Small businesses dependent on floating-rate debt suddenly face financing costs that no longer resemble the pre-2022 world.

Meanwhile, inflation remains deeply embedded in daily life.

Even if headline inflation moderates, the cumulative rise in housing, insurance, healthcare, food, and energy costs has permanently altered household psychology.

That is why consumer sentiment data looks so weak despite continued aggregate spending.

The top portion of the economy continues spending aggressively.

The bottom portion increasingly looks exhausted.

America is simultaneously experiencing prosperity and strain.

The averages conceal the divide.

The Technical Imbalance

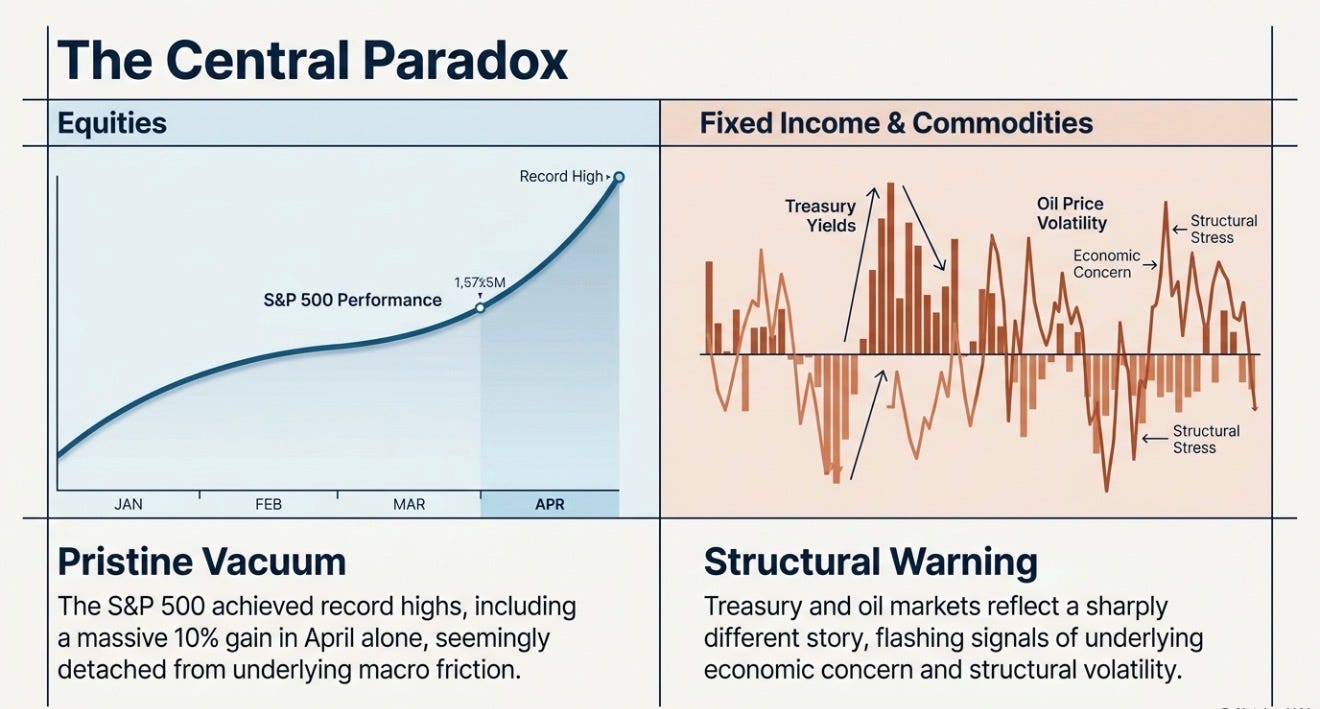

This bifurcation also explains one of the most important market divergences today: the growing disconnect between equities and bonds.

Equities currently benefit from extraordinary technical support.

Corporate buybacks continue removing enormous amounts of stock supply from the market. Meanwhile, the IPO market remains relatively muted. Massive pools of institutional and retail cash continue chasing a shrinking pool of public equities.

The result is a structural scarcity dynamic.

Stocks are not merely rising because investors are optimistic.

They are rising because supply-demand mechanics increasingly favor equities.

The Treasury market faces the opposite problem.

The federal government is issuing staggering amounts of debt into the market.

Weekly gross Treasury issuance now regularly reaches levels that would have seemed extraordinary only a few years ago.

This creates a fundamentally different technical backdrop than equities.

The stock market faces scarcity.

The bond market faces abundance.

That distinction matters.

Even if pension funds and insurers continue demanding higher-yielding fixed income, the sheer volume of Treasury supply creates persistent upward pressure on long-term yields.

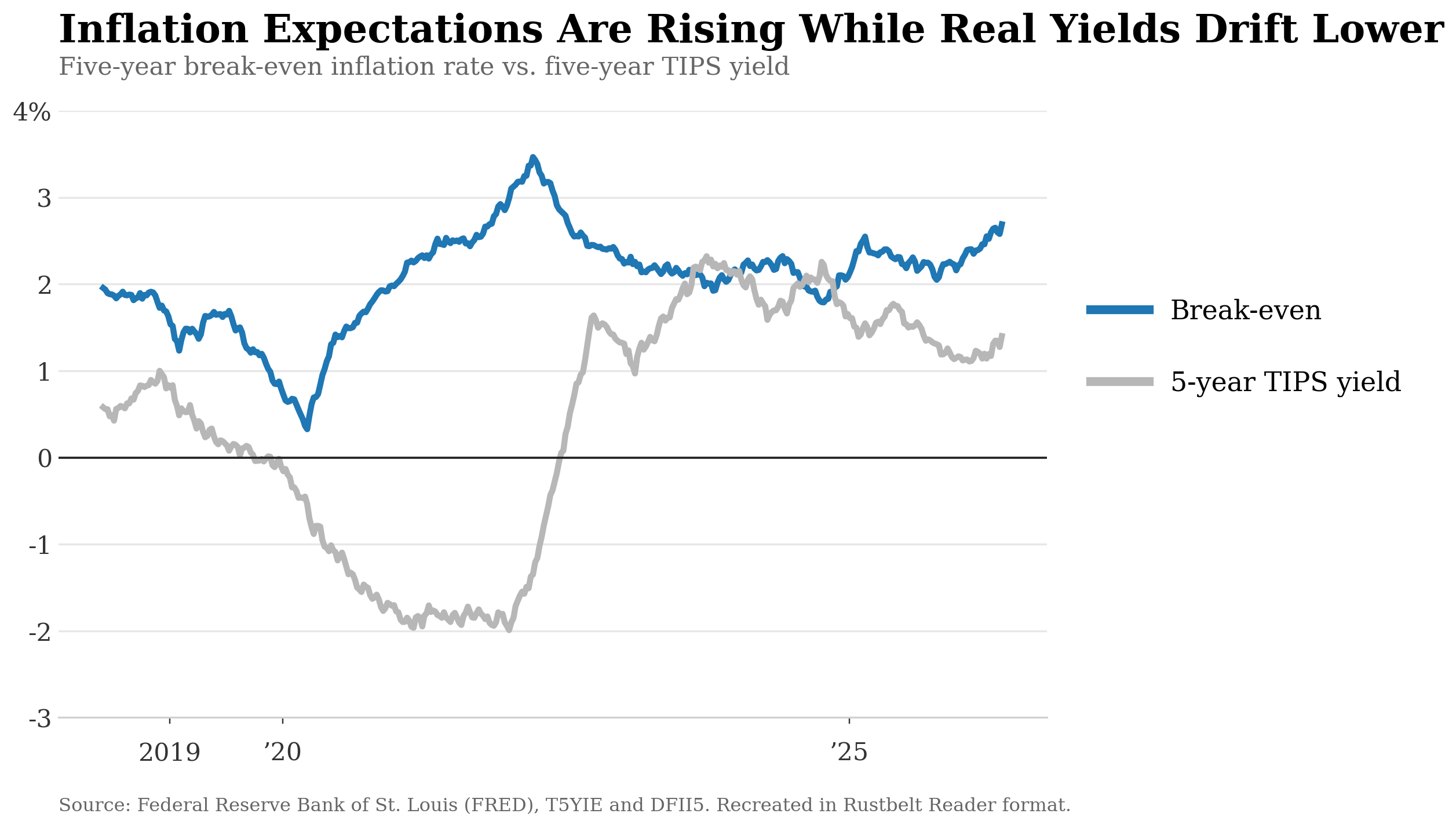

This is particularly true when inflation risks remain unresolved.

And energy remains the hidden variable.

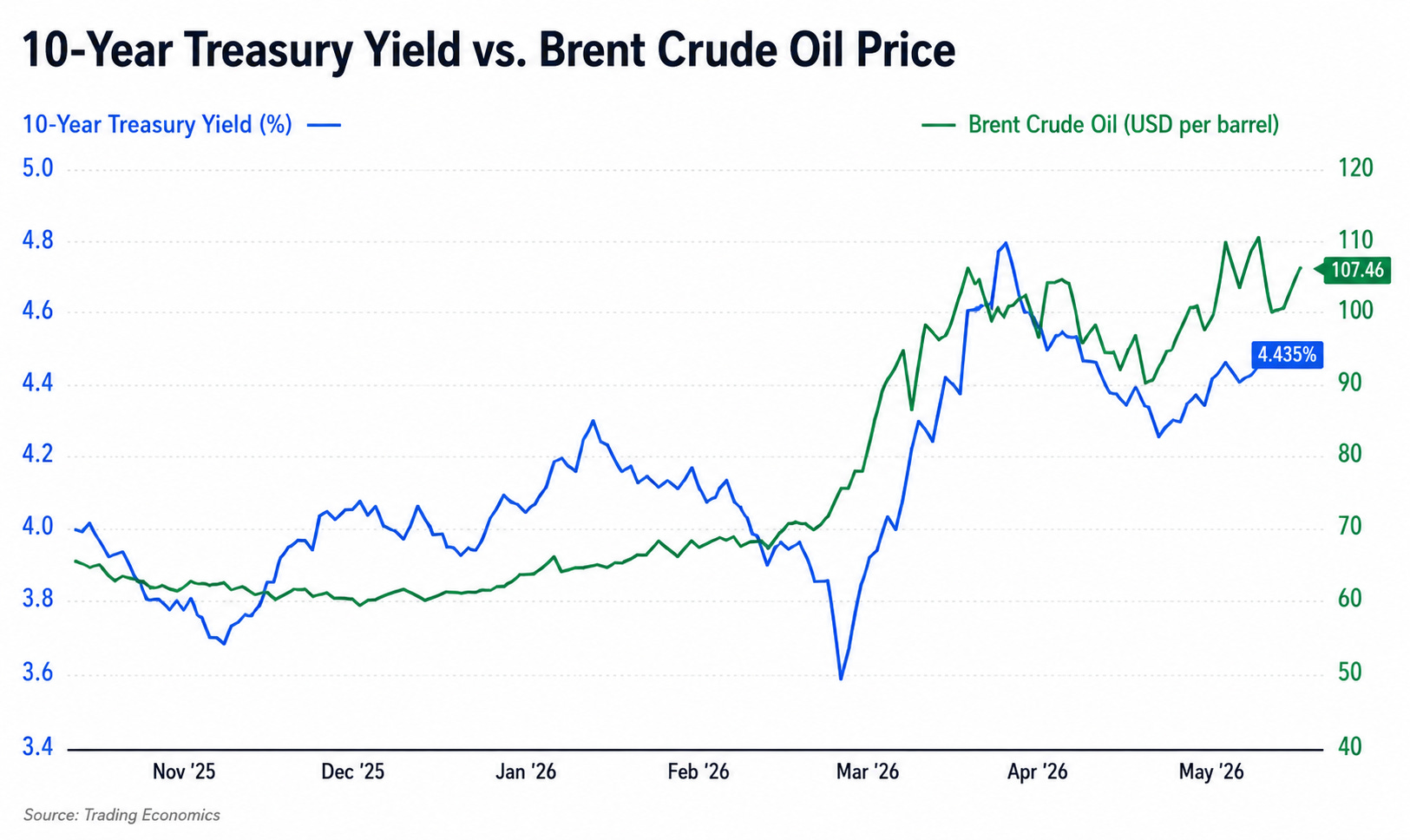

Oil Is Still the Macro Axis

Many investors continue underestimating the importance of energy prices.

Oil shocks rarely operate through a single mechanism.

They spread through the system.

Higher oil prices raise transportation costs, production costs, utility costs, and ultimately consumer prices. That keeps inflation stickier than central banks would prefer.

Sticky inflation then pushes bond yields higher.

Higher yields tighten financial conditions.

And tighter financial conditions disproportionately hit the weaker engine of the economy.

This is why markets can simultaneously experience:

Strong equity performance

Rising Treasury yields

Weak consumer sentiment

Volatile oil markets

Slowing rate-sensitive sectors

These are not contradictory signals.

They are interconnected symptoms of the same structural divide.

The equity market increasingly reflects the strength of capital-heavy sectors with pricing power.

The bond market increasingly reflects concern about deficits, inflation persistence, and long-term supply pressure.

And households increasingly reflect the exhaustion of absorbing cumulative cost increases.

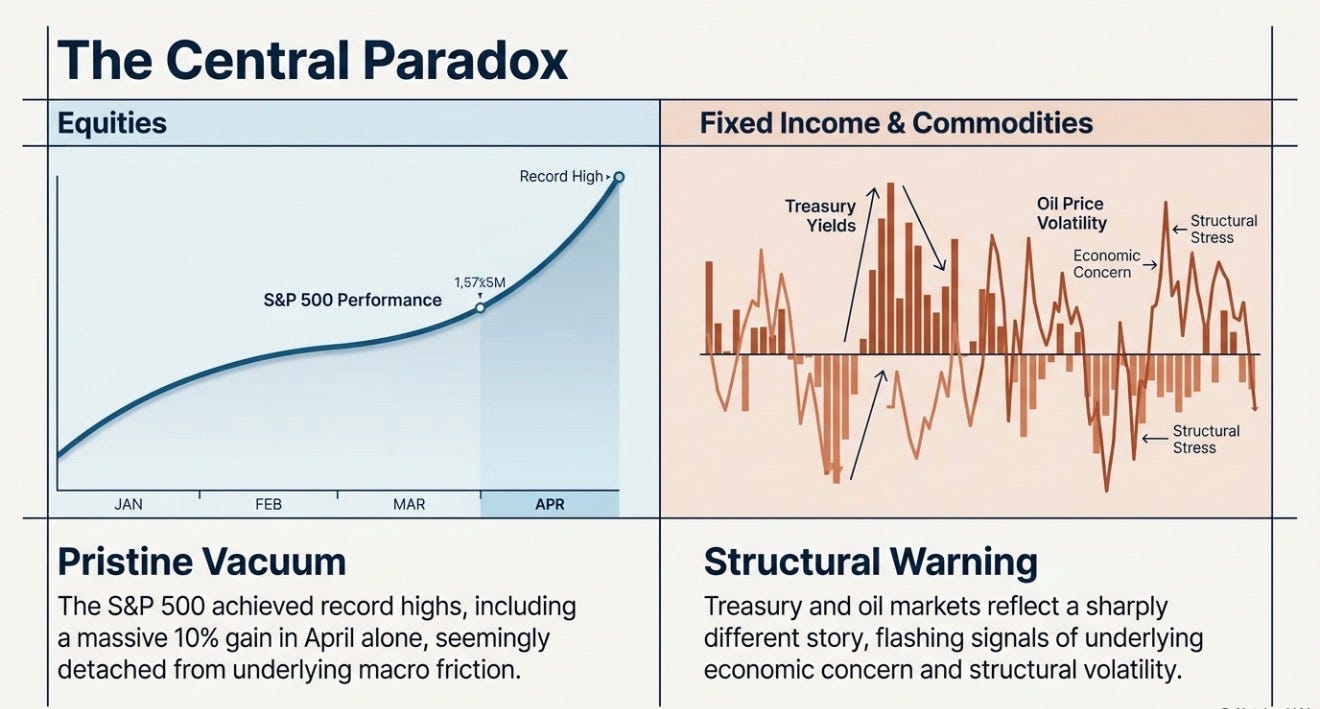

The Central Paradox

The great paradox of this cycle is that strong nominal growth may actually be damaging parts of the economy.

The very pricing power supporting corporate earnings is simultaneously keeping inflation elevated enough to prevent a meaningful collapse in yields.

That keeps pressure on consumers.

It keeps pressure on housing.

And it keeps pressure on interest-rate-sensitive industries.

This creates an unusual dynamic for policymakers.

The Federal Reserve may eventually have room to cut rates not because the entire economy is collapsing, but because one engine already is.

The challenge is that monetary policy is blunt.

Rate cuts designed to relieve pressure on struggling sectors could simultaneously reignite speculation inside the stronger engine.

That tension may define the next phase of this cycle.

Because this is no longer a synchronized economy.

It is an economy increasingly divided between capital owners and rate-sensitive earners.

Between asset inflation and living-cost inflation.

Between technological acceleration and financial exhaustion.

The Real Risk

The real danger is not necessarily an immediate recession.

It is structural fragmentation.

Historically, periods of strong market performance combined with deteriorating consumer psychology often create political and social instability.

People do not experience the economy through GDP tables.

They experience it through rent, groceries, insurance bills, and job security.

If financial assets continue surging while large portions of the population feel increasingly squeezed, the divergence itself becomes destabilizing.

Markets can tolerate inequality longer than societies can.

And that may ultimately become the defining political economy story of the late 2020s.

The stock market sees abundance.

The bond market sees strain.

The consumer sees exhaustion.

All three may be correct.

Tofler's Revolutions of Increased and Decreased Expectations. He predicted it half a century ago.