“There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency.”

— John Maynard Keynes

Money is often mistaken for the objects we carry—coins, notes, digits on a screen. History tells a different story. Money is a social technology.

More precisely, money is stored time.

When you work, you trade the finite hours of your life—your sweat, skill, and focus—for a claim check. That token says society owes you equivalent value in the future. Money is the ledger that records that sacrifice.

When that ledger is credible, societies scale. When it fails, money does not merely weaken—it breaks. And when money breaks, it rarely stays financial. It becomes political, then social.

Inflation is not just prices going up. It is the retroactive theft of time you already spent working. At the extreme, it is a society killer.

Money Isn’t Wealth. It’s a Contract.

Anthropology makes this painfully clear. On the island of Yap, enormous limestone disks—fei—served as money. Their weight made physical circulation impractical; ownership changed because the community updated its shared record. One famous stone sank at sea, yet it retained value because everyone agreed it still “counted” as wealth.

The object didn’t matter. The agreement did.

When John Maynard Keynes encountered this story, he grasped a truth modern societies still resist: money’s value comes not from substance, but from collective recognition and enforcement.

Every monetary system—cowrie shells, silver coins, gold bars, paper notes, digital reserves—is just an interface for a single promise:

Your past labor will be honored in the future.

Once that promise is broken, nothing else holds.

Debasement: The Mechanics of Theft

Debasement is usually explained badly, as though it were ancient rulers secretly shaving coins.

That’s not what it is.

Debasement is issuing more claims on future labor than the underlying economy can plausibly deliver—while insisting those claims retain their old value.

In ancient Rome, this meant reducing the silver content of the denarius while forcing it to circulate at face value. The state gained temporary relief; the cost arrived later: inflation, hoarding, farm abandonment, and coercive taxation.

In early modern Spain, it meant borrowing against silver extracted in the New World to fund imperial wars. The bullion arrived; prices rose; domestic industry thinned as imports filled the gap. The tax base strained even as obligations grew.

In the modern world, debasement wears a suit. It looks like:

chronic deficits

debt growing faster than productive output

central banks smoothing every downturn

inflation tolerated as policy lubricant

This theft is never distributed equally. When new claims are created, those closest to the source—governments, large institutions, and asset holders—get to spend them before prices rise. The worker, whose wages are sticky, receives this diluted money last. By the time the new money reaches the mill or the machine shop, its purchasing power has already been siphoned upward.

Debasement isn’t any expansion of money—it’s expansion that becomes a substitute for real reform, where the adjustment is forced through purchasing power rather than openly through taxes, defaults, or spending cuts.

It is theft with a spreadsheet instead of a knife.

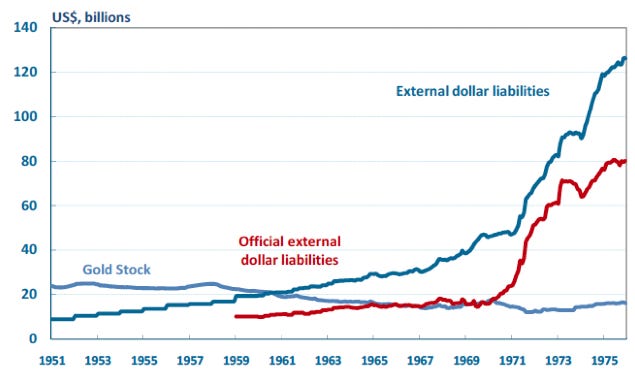

Why 1971 Is the Hinge

The hinge in the modern story is not 2008.

It is 1971.

Under Bretton Woods, currencies were pegged to the dollar, and the dollar was anchored to gold. Gold was a harsh taskmaster: it limited how much credit a government could create, forcing fiscal discipline by tying money to something outside politics.

In August 1971, Richard Nixon closed the gold window.

That single act did two things:

It removed an external discipline mechanism from the system—converting the monetary promise from redemption into credibility.

It expanded the feasible policy set: deficits could be financed with far less immediate penalty, because adjustment could happen through inflation, repression, or time—rather than through explicit taxes or immediate austerity.

From that point on, money was no longer anchored to metal or output. It was anchored to something far softer: institutional credibility.

That made financing wars and welfare states without raising taxes easier. It didn’t cause financialization by itself—but it removed the anchor that forced discipline, so the system increasingly solved problems by expanding claims rather than expanding output.

And it rewired incentives at the margin: when returns to paper claims are protected, backstopped, or advantaged by policy, capital naturally flows toward balance sheets and markets—not the mill, the mine, or the machine shop.

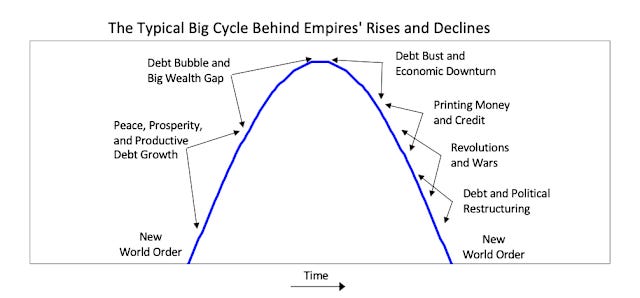

Dalio’s Arc: Money Inside the Cycle of Power

When debts grow faster than incomes, the only question is how the losses will be shared.”

— Ray Dalio

This is where Ray Dalio earns his keep.

Dalio’s Changing World Order framework shows how great powers rise on productivity, then drift toward financialization, leverage, and internal conflict. Late in the cycle, promises multiply faster than output. Debt replaces growth. Money becomes political. When a nation reaches this stage, it has effectively exhausted its own stored time. To maintain the illusion of solvency, the system must either pull time forward from the future (through debt) or strip-mine it directly from the present (through inflation).

Leaders do not choose debasement because they are foolish. They choose it because the alternatives—explicit taxation, benefit cuts, or strategic retreat—are politically radioactive.

The system buys time by spending future.

This curve is not a prophecy. It is a mechanical sequence.

On the way up, debt finances productive growth. On the way down, debt finances stability itself.

Inequality widens. Politics polarize. Money printing replaces reform because it is faster and less visible. The breaking point arrives not when the system looks weakest—but when it looks most dependent on leverage to keep functioning.

Ferguson’s Heuristic — Properly Understood

What is often called “Ferguson’s Law” is not a formal law invented by Sir Niall Ferguson. It is a historical heuristic he has articulated and popularized, drawing on long-run evidence from past empires.

The formulation is simple:

When interest payments on public debt exceed military spending, a great power enters a danger zone.

The insight is not arithmetic trivia. It is strategic.

Interest payments buy nothing. They secure no borders, build no infrastructure, and fund no research. They are pure deferred maintenance on the past.

When debt service crowds out defense, a state loses maneuverability. Resources are consumed maintaining yesterday’s promises rather than securing tomorrow’s capacity.

The United States has now crossed this threshold.

But Ferguson’s deeper warning is institutional, not just fiscal. Late-stage states do not merely overspend—they lose administrative competence. Tax systems become brittle. Bureaucracies expand but perform worse. Legal systems slow. Trust erodes.

Money printing steps in not only to fund obligations, but to compensate for institutional decay.

When institutions weaken, inflation accelerates.

“The real danger is not bankruptcy, but the steady erosion of a state’s capacity to govern itself.”

— Niall Ferguson

Thucydides Trap: When Time Runs Out

“The strong do what they can, and the weak suffer what they must.”

— Thucydides

Debt cycles alone do not determine collapse timing. Geopolitics does.

Thucydides observed that the rise of Athens and the fear it inspired in Sparta made war more likely. Rising powers overspend to establish credibility; incumbents overspend to maintain dominance.

War compresses timelines. It forces systems to prove strength now, not later.

This is why monetary breakdowns cluster around geopolitical shocks. The ledger can be stretched for years. War makes the stretch visible.

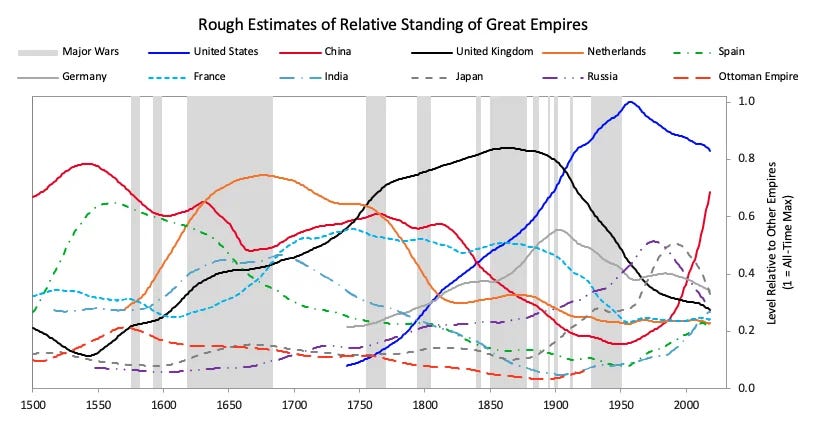

The above chart is modern synthesis of major historical power transitions often cited in discussions of the “Thucydides Trap.” The pattern is not deterministic, but it illustrates how rising powers have repeatedly triggered conflict when institutional and economic buffers fail.

When Money Dies, Society Breaks

Here is the hard historical warning: high inflation is not just an economic illness. It is a moral solvent.

It punishes the saver, rewards the speculator.

It teaches speed over patience.

It tells workers their stored time was a lie.

The Weimar Republic did not merely experience rising prices. It experienced a collapse of trust: savings wiped out, contracts mocked, politics radicalized. Money stopped coordinating life.

France’s assignats and Britain’s imperial unwind followed the same script at different speeds. Inflation does not announce itself as theft. It presents as relief. Then it dissolves the social contract.

The False Indicators—and the Long Survivors

History is full of false recoveries.

Rome reformed. Britain stabilized. France reset. Even Weimar briefly balanced. Systems can look “fixed” right up until the next shock exposes how leveraged they still are.

Some empires endure astonishingly long. The Byzantine Empire survived nearly a millennium after the fall of Rome’s West—not because it was virtuous, but because it adapted, retrenched, and repeatedly renegotiated contracts.

In the modern era, this renegotiation is called financial repression. A highly leveraged state survives by holding interest rates below inflation, forcing captive buyers—like domestic pension funds—to swallow government debt, and quietly eroding purchasing power over decades. The system does not always end in a spectacular, sudden crash; often, it just slowly grinds the middle class to dust.

Longevity does not mean safety. It means time. But time is bought at a price.

This 500 year “look back” from Ray Dalio matters not because it predicts collapse, but because it shows how systems fail slowly.

Notice that decline is rarely linear. Power ebbs, stabilizes, and sometimes rebounds—often after reforms or temporary re-anchoring of trust. The inflection points cluster around major wars, where fiscal strain forces fantasy to reconcile with reality.

The danger is not decline itself, but mistaking a plateau for permanence.

The Contract That Matters

Dalio gives the arc: late-stage powers monetize promises.

Thucydides gives the trigger: rivalry accelerates the timetable.

Ferguson’s analysis gives the threshold: when debt service crowds out defense, capacity erodes.

And the history of inflation gives the human warning: when money lies, society fractures.

A currency is the most important contract a state signs with its citizens. It says:

Your time will be honored.

When that contract is broken—quietly, gradually, politely—it is still broken.

The ledger is always rewritten.

Not by ideology.

Not by politics.

By necessity.

Sources & Further Reading

Dalio, Ray. The Changing World Order: Why Nations Succeed and Fail. Bridgewater, 2021.

Ferguson, Niall. The Cash Nexus: Money and Power in the Modern World, 1700–2000. Basic Books, 2001.

Ferguson, Niall. “The Debt Interest Trap.” Hoover Institution, lectures and essays.

Thucydides. History of the Peloponnesian War.

Keynes, John Maynard. “The Economic Consequences of the Peace” and essays on money.

Eichengreen, Barry. Globalizing Capital: A History of the International Monetary System.

Reinhart, Carmen & Rogoff, Kenneth. This Time Is Different.

U.S. Congressional Budget Office, historical and projected federal outlays.

Quite enlightening. Thank you

Very well written and articulted. Many thanks,