The Second Reactor

France proved nuclear works. Then it forgot how to build a reactor. America never learned.

By Phil Brunelleschi

There is exactly one example of a large industrial economy decarbonizing its electricity in a hurry, and it happened before anyone was trying to decarbonize anything.

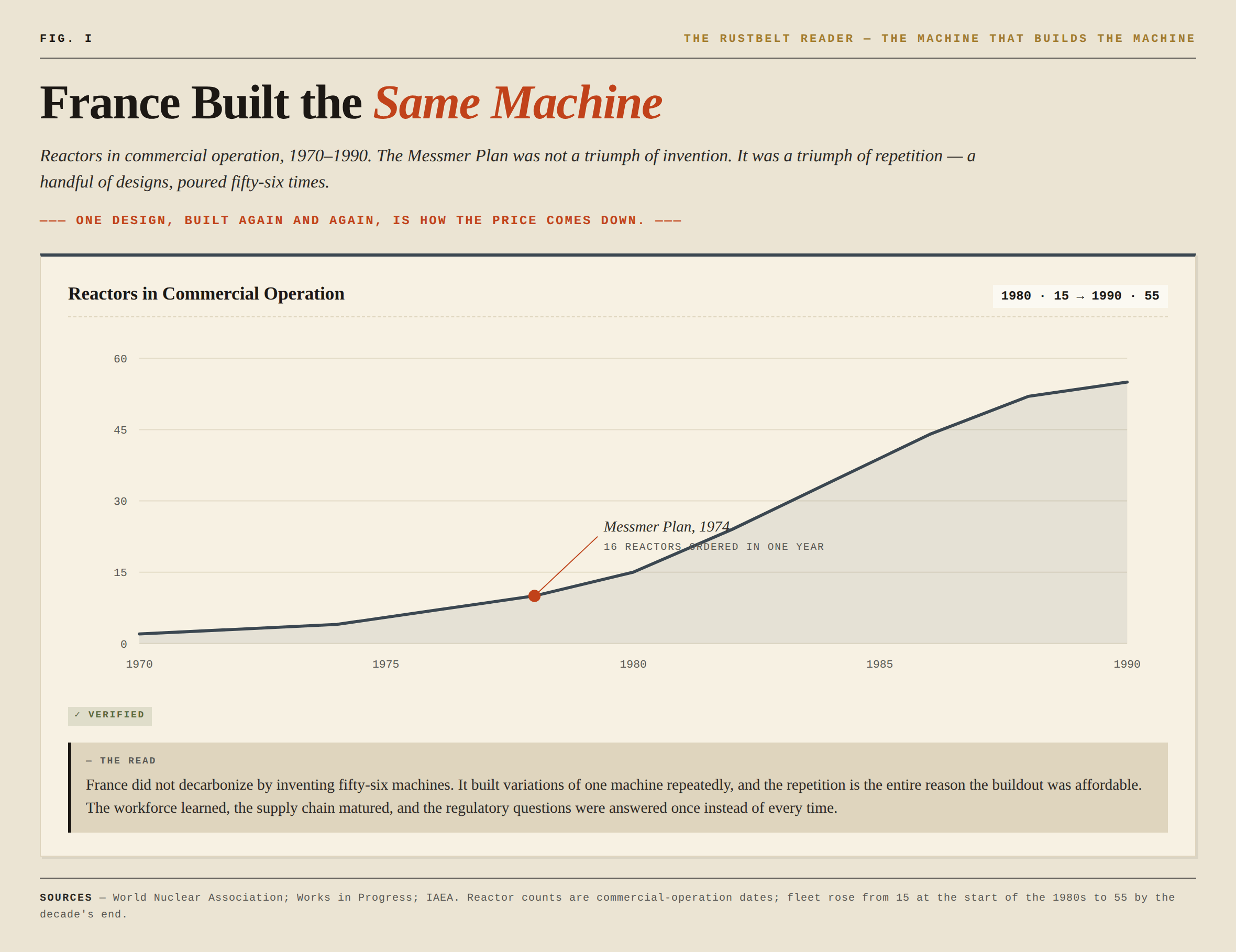

In March 1974, five months after the oil embargo exposed how much of France ran on imported petroleum, Prime Minister Pierre Messmer went on television and committed the country to building nuclear reactors at a pace no democracy had attempted in peacetime. The plan was not debated in parliament. It was not put to referendum. EDF, the state utility, ordered sixteen reactors that year alone, doubling the national order book in a single procurement.

Over the next fifteen years France built fifty-six of them. The fleet went from fifteen reactors in operation at the start of the 1980s to fifty-five by the end. By the time it was finished, France produced roughly three-quarters of its electricity from nuclear fission, and it has stayed there for forty years.

No large democracy has matched that pace before or since; even China’s current nuclear buildout, enormous in absolute terms, has not replicated France’s per-capita sprint. If you want to know whether the firm, low-carbon grid the climate models assume can actually be built on a compressed timeline, France is the only completed experiment you have. It is worth understanding precisely what it proves — and, more importantly, what it doesn’t.

Because the most instructive thing about the French nuclear program is not that it succeeded. It is that France, having done the hardest version of this once, can no longer do it at all.

For the Rust Belt specifically, this is not an abstract energy debate. The region still holds much of the country’s industrial memory — steel, forgings, turbines, welders, river logistics, rail, machine shops, the habit of building heavy things meant to last longer than a software cycle. If America is serious about nuclear, the question is not only which reactor wins. It is whether the industrial belt that once made the components of national power can be rebuilt to do it again.

The lesson comes in three parts. France proved nuclear works when a country standardizes the machine and finances it like national infrastructure. France also proved that the capacity to build can decay until even a single reactor becomes a fiasco. America’s recent record, from Vogtle to NuScale, shows the same failure in a different form — not bad physics, but bad institutions and bad capital structure. And the new Westinghouse push matters because it is the first American attempt in decades to solve the actual problem, which was never engineering.

Nuclear’s modern problem is more accurately a question of capital structure: who absorbs the first-of-a-kind risk, who carries the interest during the years of delay, and who gets to build the second unit cheaper than the first.

What France actually proved

The standard telling treats the Messmer Plan as a triumph of engineering or national will. It was neither, exactly. It was a triumph of standardization and finance — and those are the two variables that matter for anyone trying to learn from it.

France did not build fifty-six different reactors. It built a handful of designs, repeatedly, mostly licensed from Westinghouse and adapted domestically. Build the same thing fifty times and the fiftieth is dramatically cheaper than the first: the workforce learns, the supply chain matures, the regulatory questions get answered once instead of every time. This is the learning curve, and it is the entire reason the buildout was affordable. EDF moved to larger standardized designs specifically to capture economies of scale.

The financing was the other half. A state utility borrowing at sovereign-adjacent rates, building on a national mandate, does not face the cost-of-capital problem that kills nuclear everywhere else. Nuclear plants are almost all upfront cost — the fuel is cheap, the construction is brutal — which means the interest rate during construction is not a detail, it is the ballgame. France financed its fleet at terms no ordinary American utility project could replicate, and it never had to relitigate each plant in front of a hostile rate commission.

So the benefits were real and they were large. Four decades of some of the lowest-carbon electricity in the developed world. Electricity prices that stayed low and stable while neighbors swung with the gas market. Genuine energy independence — the original goal, climate being a happy accident the French backed into fifty years early. An export business in both power and reactor technology. And a live demonstration of exactly the attributes the rest of this decade is rediscovering it needs: power that is dense, dispatchable, domestic, and always on.

That is the case for nuclear, and France is the proof of concept. But a proof of concept is only useful if you understand the conditions it ran under. And the conditions are where the story turns.

How France lost the machine

Three problems came for the French fleet, and all three are instructive because they are not arguments against nuclear — they are arguments about what you are actually signing up for.

The first is that standardization cuts both ways. The same design fifty times means the same flaw fifty times. In late 2021, inspectors found stress-corrosion cracking near welds in certain reactors, rooted in a design geometry EDF had adapted from the original — and because the fleet was standardized, the discovery could not be contained to one plant. By the summer of 2022, thirty-two of France’s fifty-six reactors were offline. National nuclear output fell to 279 terawatt-hours, the lowest since 1992, and France, the model of energy independence, became a net electricity importer for the first time in decades — during the European energy crisis, at the exact moment nuclear was supposed to prove its resilience against the gas shock. A standardized fleet carries standardized failure risk. The warning arrived on schedule.

The second problem is demographic, in the way that fleets have demographics. Build fifty-six reactors in fifteen years and you have bought yourself fifty-six retirements in roughly fifteen years, four decades later. The grand carénage — the refurbishment program to push the fleet past forty years — runs into the tens of billions and climbing. The sprint that built the fleet so cheaply guaranteed the bill would come due all at once. You do not avoid the capital-stock turnover problem with a compressed buildout; you time-shift it.

The third problem is the one that should stop anyone who thinks the answer is simply “do what France did.” France can no longer do what France did.

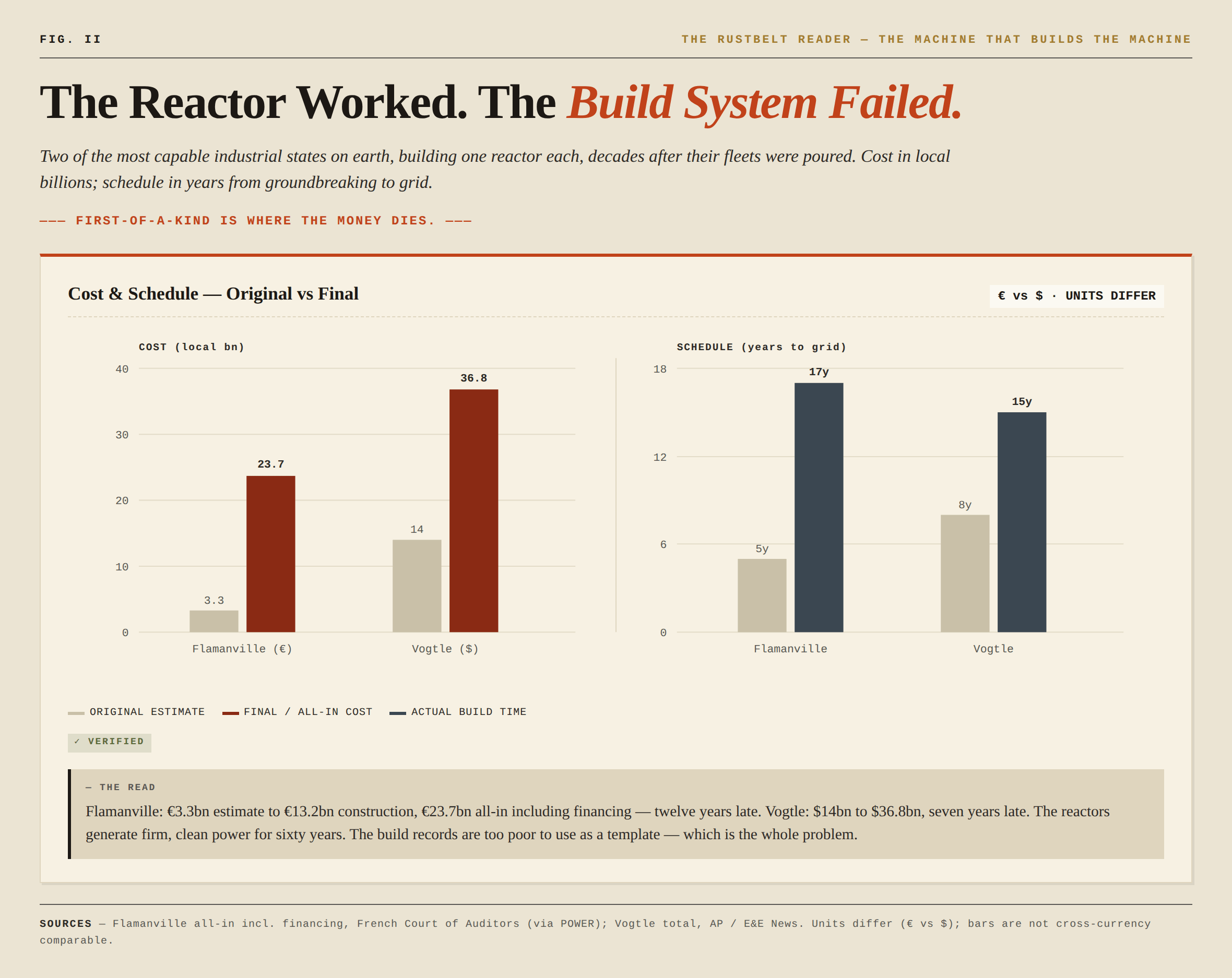

Flamanville 3, the reactor France began in 2007 to prove it could still build, was supposed to cost €3.3 billion and open in 2012. It connected to the grid in December 2024 — more than twelve years late — at a construction cost of €13.2 billion. The French Court of Auditors, counting the financing, put the all-in figure near €23.7 billion. At that number, the auditors calculated, the electricity would have to sell at roughly €138 per megawatt-hour to earn a four-percent return. That is not competitive power. That is a monument.

The country that built fifty-six reactors in fifteen years took seventeen years to build one. The capability did not transfer across the generational gap. The workforce that knew how to pour the concrete and weld the circuits had retired. The supply chain had atrophied. The standardization advantage was gone, because you cannot have a learning curve on a fleet of one. Everything that made the 1970s buildout cheap was absent from the 2000s rebuild, and the cost reflected it precisely.

The American mirror

If you want to know whether the United States can simply decide to build nuclear, the answer is already in the record, and it reads almost identically.

Plant Vogtle in Georgia, Units 3 and 4, are the only new reactors completed in the United States in more than thirty years. They used the Westinghouse AP1000, a new design, built for the first time. They were projected to cost $14 billion and open in 2017. They were finished in 2024 — seven years late, fifteen years from start to finish — at a final cost of $36.8 billion. Westinghouse went bankrupt partway through. The twin project in South Carolina, the V.C. Summer expansion, started at the same time using the same reactor, was abandoned in 2017 after billions had been spent and nothing was finished; some of the executives involved went to prison over the cost misrepresentations.

Read the French and American stories side by side and the symmetry is the whole point. Two of the most capable industrial states on earth, with every incentive and considerable political will, have struggled to build large nuclear reactors on a schedule or budget that can serve as a repeatable model. France lost the capability it once had. The United States arguably never industrialized it — Vogtle and Summer were first-of-a-kind builds precisely because America never did the standardized fleet France did.

This is why the lazy version of the pro-nuclear argument fails. “France did it, so we can too” ignores that France did it under conditions neither country can reconstruct: a single state utility, a standardized design built dozens of times, sovereign-cost financing, and a political system that could override local opposition and never reopen the question. Strip those conditions away and you get Flamanville. You get Vogtle. You get expensive power with real operating value — sixty years of firm, clean electricity — but a construction record too poor to use as a template.

The binding constraint on American nuclear was never the physics. The reactors work; Vogtle is generating clean power right now and will for sixty years. The binding constraint is institutional and financial — the cost of capital, the absence of a standardized design, the regulatory relitigation of every plant, and a utility model that earns its return on getting projects approved rather than on building them cheaply. The regulatory weight is real and worth understanding on its own terms. After the 1971 Calvert Cliffs decision forced nuclear licensing to take environmental review more seriously under NEPA, the permitting process became slower, broader, and easier to litigate. At the same time, the ALARA principle — radiation exposure kept “as low as reasonably achievable” — created a safety logic with no obvious stopping point: if another layer of protection can be justified, the plant can be asked to carry it. Some studies attribute a meaningful share of the 1970s and 1980s nuclear cost escalation to this regulatory ratchet, much of it before Three Mile Island. Then came the accident itself, only days after The China Syndrome had put a fictional meltdown into theaters. The result was not just higher cost. It was a cultural fusion of civilian nuclear power with catastrophe.

There is also a political economy question underneath the cost history. Nuclear threatened incumbent fuel systems, especially coal, oil, and gas, because it offered dense baseload power without a continuing fuel market of the same kind. That does not prove a coordinated campaign against it. The regulatory ratchet, local opposition, environmental law, and post-Three Mile Island fear had plenty of organic force on their own. But an honest account of why America stopped building should still ask who benefited from delay, because the economics of the delay were not neutral. These are the same institutional questions that run through every account of why the American grid costs what it does. Nuclear just states them in their most expensive form.

Two bets, and the one that isn’t

So the country needs more firm, dense, carbon-free power — the kind that survives the winter peak, that holds when the wind drops, that the prior essays in this series have argued the retirement schedule wrongly assumed away. And the one technology that unambiguously provides it cannot currently be built at acceptable cost by the two nations best positioned to build it. The way out is not a new machine. It is a different way of paying for the machine that already works.

The popular answer is the small modular reactor — shrink the machine until you can build it in a factory, identically, hundreds of times, and buy the French learning curve through manufacturing repetition instead of state command. It is an appealing thesis. It is also where most of the hype has attached to the shakiest structures, and the distinction between the two tracks of the nuclear revival is the most important thing to get right.

Start with what the institutional argument actually predicts. If the binding constraint is the cost of capital and the absence of a repeatable design, then the credible builders are the ones with a licensed, operating design and a balance sheet — or a state — large enough to absorb first-of-a-kind losses. That is not a clean-sheet startup. It is an incumbent.

Watch where the real money went. In October 2025 the U.S. government, Brookfield and Cameco announced a strategic partnership intended to accelerate at least $80 billion of new Westinghouse AP1000 deployment, with the government helping organize the financing and permitting framework and the regulator extending the AP1000 design certification to 2046. Strip away the politics and look at the structure: it is the only Generation-III+ design actually built and operating in America — the Vogtle reactors — slated to be poured again, repeatedly, with the cost-of-capital problem addressed the way it has most often been addressed in successful nuclear buildouts: by moving part of the construction risk toward a public or sovereign balance sheet. That is the France formula, transposed. Whether the second AP1000 fleet comes in dramatically cheaper than the first is the entire bet — and it is the only bet with a completed American reactor underneath it. Large reactors are not the part to give up on. They are the part the institutional logic actually points to — for utility-scale baseload, behind a utility or a state that can carry a thirty-year asset.

The genuinely promising small reactor follows the same rule, not the opposite one. GE Vernova Hitachi’s BWRX-300 — a simplification of a boiling-water design that has operated for decades — is the first SMR under construction in North America, building now at Ontario’s Darlington site behind a public utility paying out of its own balance sheet, with the Tennessee Valley Authority pursuing the same design at Clinch River in Tennessee. An incumbent vendor, a proven design lineage, a creditworthy public offtaker. Even here the honest caveat holds: the BWRX-300’s marketing price of roughly $2,250 a kilowatt is not what the first Darlington units are actually costing, and first-of-a-kind is exactly the phase where Flamanville and Vogtle went wrong. But the structure is sound. This is the small reactor’s real lane — not as a replacement for the large fleet, but for the data-center campuses and industrial loads that are co-located, that have a deep-pocketed offtaker, and that the grid cannot serve fast enough on its own.

Then there is the speculative tier, and it should be named as such. NuScale holds the only U.S.-certified small-reactor design, which sounds like a lead until you read the rest of the record: its flagship project in Idaho collapsed in 2023 when the per-megawatt cost climbed past what its municipal subscribers would pay and they walked. Its public-market structure rewards design milestones, customer announcements, and memoranda of understanding long before the hard validation arrives — a built, operating, repeatable plant. That is not a knock on the engineering. It is the argument of this entire essay restated a third way: the incentives are pointed at the stock, not the steel, and a company without a balance sheet to absorb the first-of-a-kind loss is the wrong institutional vehicle to solve a problem that was institutional all along. The reactor is not what fails. The capital structure is.

Who pays for the first one

To understand why the $80 billion structure looks the way it does, you have to start with why the state suddenly cared. For twenty years electricity demand in America was flat, and a flat market does not produce strategic panic. That ended. Artificial intelligence turned electricity into the input that determines who wins the most important technology race of the era. One industry description captures the logic: a data center takes the most expensive form of energy, electricity, and turns it into intelligence. And on the metric that matters, the United States is behind: China now generates more than twice as much electricity as America does, self-sufficient through coal and renewables, while the U.S. faces the scale-up and deployment constraints the prior essays in this series have documented. When power becomes the binding constraint on national competitiveness, power stops being a market and becomes a matter of state.

Bridgewater has a name for the broader shift, and it is the right one: modern mercantilism — the return of the state to the center of strategic industries, prioritizing national strength, supply-chain security, and self-sufficiency over the free-market consensus that governed the prior forty years. Their energy-security work makes the corollary explicit: cheap, abundant, domestic power is now treated as a precondition for winning the AI race and everything downstream of it. Once you see the nuclear revival through that lens, the financing structure stops looking strange and starts looking inevitable.

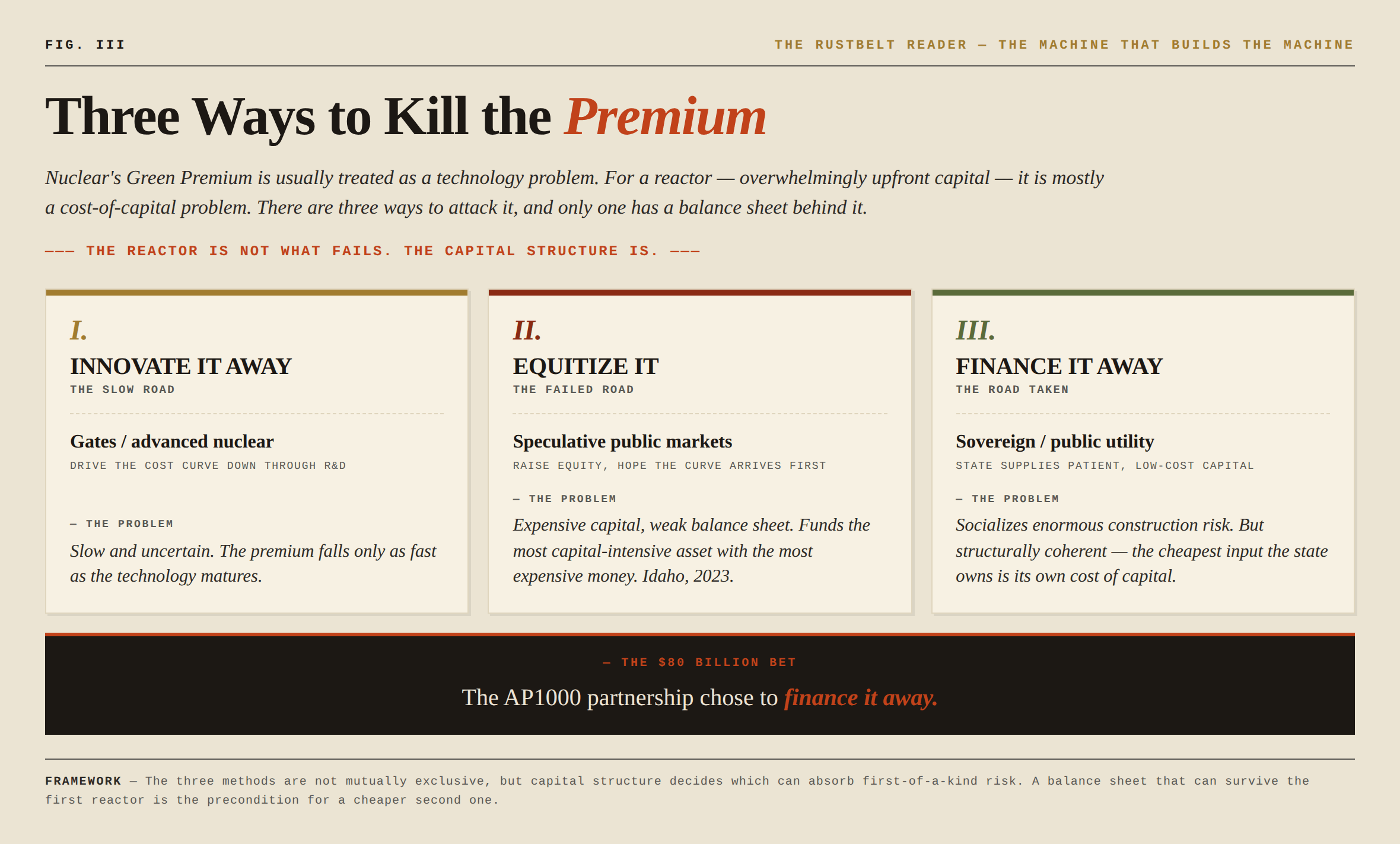

Recall the Green Premium — Bill Gates’s framing that the clean option costs more than the dirty one, and that the transition is fundamentally the work of driving that premium to zero through innovation. It is a useful idea with a blind spot. For nuclear, the premium is not mostly a technology problem. A reactor is overwhelmingly upfront capital; the fuel is cheap and the plant runs for sixty years. That means the cost of the electricity is set, more than by anything else, by the interest rate during construction and the years of delay before the asset earns a dollar. Flamanville’s auditors said it plainly: at €23.7 billion all-in, the power needs to sell near €138 a megawatt-hour to clear a four-percent return. Much of that premium is not the reactor. It is the financing of the reactor — plus the delay risk that financing magnifies.

Which means there are three ways to kill the premium, not one. You can innovate it away, which is Gates’s bet and a slow one. You can equitize it — raise speculative capital and hope the learning curve arrives before the subscribers leave, which is the bet that just failed in Idaho. Or you can finance it away: have the state supply the one input only the state owns below market — sovereign, patient, low cost-of-capital — and let the private builder supply the design and the operations.

The $80 billion AP1000 structure is the third option made concrete. The government helps organize the financing and permitting framework, takes a slice of the upside through a profit-participation interest — 20% of Westinghouse’s cash distributions above a $17.5 billion threshold, convertible to an equity stake of up to roughly 20% if the company goes public above $30 billion by 2029 — and, by facilitating the financing of long-lead-time items, moves part of the construction risk toward the sovereign balance sheet. The premium does not have to be innovated down to zero, because the most expensive part of it — the cost of capital — is being shifted to where it is cheapest.

The mercantilist lease — not legally, but economically. Look at where the capital actually comes from and the arrangement names itself. The stack is being shaped partly through allied money. Japan’s $550 billion U.S. investment commitment has been reported as a potential vehicle for nuclear projects involving Westinghouse, with Japanese firms positioned in the supply chain. Korea’s broader industrial package, and firms like Doosan, point in the same direction: allied capital and allied heavy industry being organized around American strategic capacity. Allied surplus capital is being steered toward a domestic strategic asset that the American state helps finance, partly underwrites, and stands to share in — while the hyperscalers line up to offtake the power. Each party supplies what it holds most cheaply: the allies their capital surplus, the state its balance sheet and permitting power, Westinghouse its one proven design, the AI buildout its demand. That is not a subsidy in the old sense of a check written to lower a price. It is the state leasing out its cost-of-capital to a sector it has decided is too strategic to leave to the market — the four tenets of modern mercantilism expressed as a term sheet.

What that sovereign capital actually buys, in the physical world, is not a reactor. It is a supply chain.

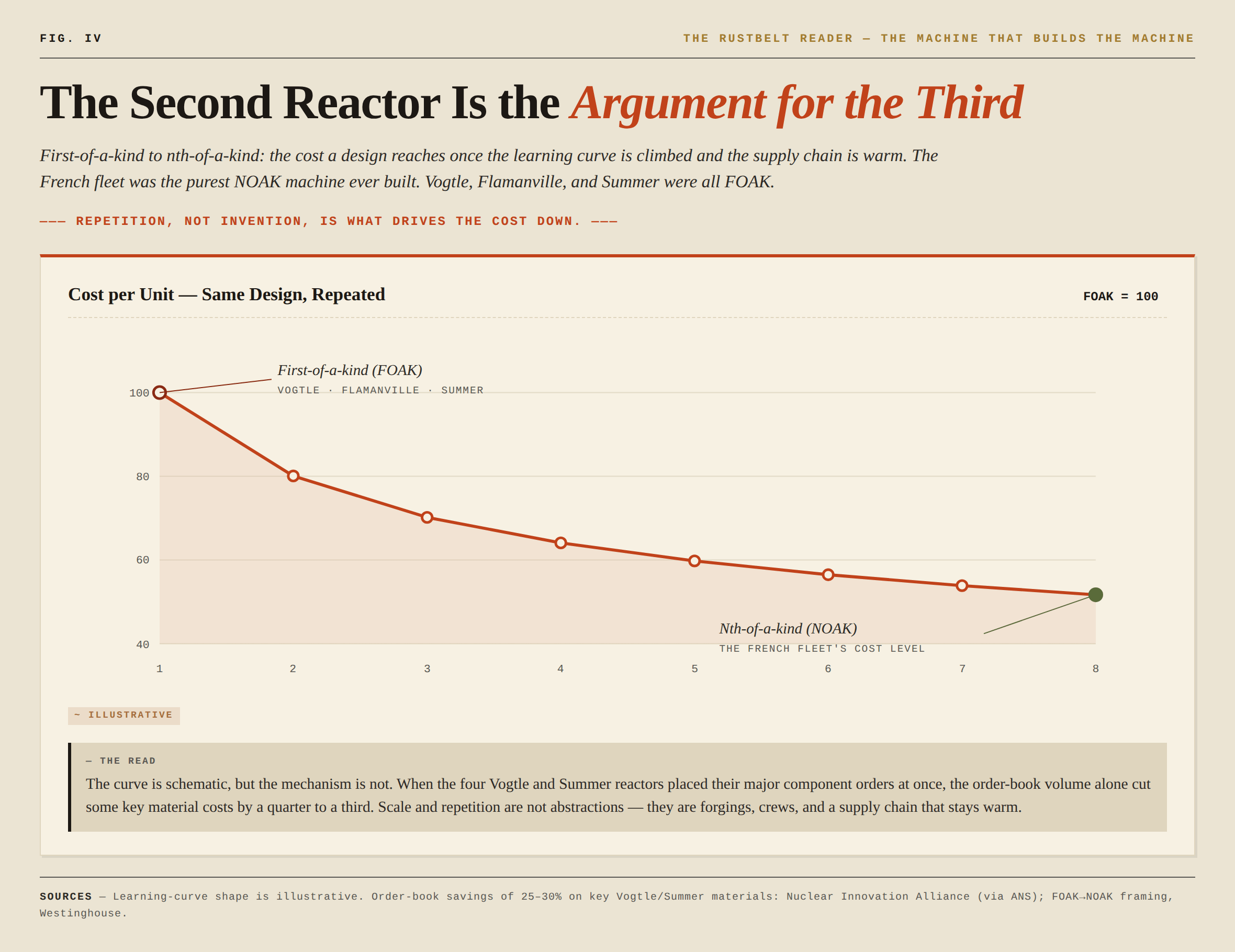

The deal’s own language is explicit that Westinghouse will lean on the industrial base “established during the construction of Vogtle units 3 and 4” — which is the tell. The thing that makes the second reactor cheaper than the first is not a cleverer design. It is a workforce that has poured the concrete before, a fabricator that has passed nuclear-grade inspection before, and a forging shop that has cast a reactor pressure vessel before. The industry has a name for the destination: nth-of-a-kind, or NOAK — the cost level a design reaches once the learning curve has been climbed and the supply chain is warm. France’s fleet was the purest NOAK machine ever built. Vogtle, Flamanville, and the cancelled Summer plant were all FOAK — first-of-a-kind — and FOAK is where the money dies. The entire $80 billion bet is an attempt to buy the country a passage from FOAK to NOAK, and that passage runs through physical plant. When the four Vogtle and Summer reactors placed their major component orders simultaneously, the order-book volume alone cut the price of some key materials by a quarter to a third. Scale and repetition are not financial abstractions here; they are forgings and crews.

This is where the financing structure becomes a regional question — and where this publication keeps its attention: not the reactor as a finished object, but the critical components inside it, and who can still make them. The heaviest of those components — reactor pressure vessels, steam generators, pressurizers — are forged at a handful of facilities on earth, most of them in East Asia, which is why Korea’s Doosan supplied Vogtle’s. Korea is the comparison that should focus the mind. Its recent nuclear build costs are commonly estimated at a fraction of U.S. costs, while Vogtle became one of the most expensive nuclear construction projects in the world. The numbers are not perfectly like-for-like, and the regulatory systems are different. But the direction is not mysterious: Korea kept a nuclear supply chain warm, and the United States did not. American nuclear components ordered cold after a thirty-year gap are expensive precisely because the capability atrophied. Korean components are cheaper because Korea never stopped making them.

So the choice arrives in its sharpest form. A serious American nuclear program is a decision about whether those forgings get made here again, in shops that can handle a 17,000-tonne press and the metallurgical tolerances a reactor demands — or whether the country keeps renting the critical components from the allies who held onto the capacity, which is cheaper today and is part of what the mercantilist lease actually buys. That is not a Silicon Valley capability. It is a heavy-industrial capability — the kind the Rust Belt once specialized in. The mercantilist lease is ultimately a bet that sovereign capital can rebuild not just a reactor fleet but the heavy-industrial base that fleets require — the machine shops, the forge lines, the welders certified to nuclear standard, the river and rail logistics to move components that cannot go by road. The financing structure is the visible part. The supply chain is what it is really trying to resurrect.

This is also why the earlier distinction holds so cleanly. The structures that work are the ones aligned with where the cheap capital actually lives: the sovereign behind the AP1000 fleet, the creditworthy public utility behind the BWRX-300. The structure that failed tried to fund the most capital-intensive asset in the economy with the most expensive money in the economy — retail equity chasing a milestone narrative. Gates’s framework cannot quite see this, because it treats the premium as a property of the technology. The mercantilist sees it for what it is: a property of the financing, and therefore something a state can simply decide to absorb. Whether that is wise industrial policy or a slow socialization of enormous construction risk is a real question, and the honest answer is that we will not know until the follow-on reactors are poured. But it is the bet the country has placed, and it is a coherent one.

What the record actually recommends

The case for American nuclear does not rest on optimism, and it should not pretend to. It rests on a process of elimination, and now on a decision the state has already made. The winter peak has to be met by something firm. The AI buildout is not waiting. The retiring coal fleet provided dispatchable power that intermittent sources do not replace one-for-one. Something dense and always-on has to fill that space — the list of carbon-free options that qualify is short, and the state has now begun putting its balance sheet behind the only one of them that is also firm.

France proved the machine works and the grid it produces is worth having. France also proved that the machine is only as buildable as the institutions around it — that the reactors were never the hard part, the standardization and the financing and the political durability were, and that a country can lose those faster than it loses the engineering.

That is the actual lesson for the United States, and it is not “build reactors,” nor is it “wait for the factory to save us.” It is that the country has to rebuild the conditions under which reactors are buildable: a standardized design poured more than once, financing that does not strangle a thirty-year asset at the construction phase, and a regulatory posture that answers the safety questions thoroughly and then stops reopening them. That is what the AP1000 partnership and the BWRX-300 are each, at different scales, trying to buy — a proven design behind a balance sheet that can survive the first one. And it is what the speculative pure-plays cannot, because they are trying to solve a financing problem with the wrong kind of financing.

The honest forward-looking caveat is that none of it is proven yet. The repeat AP1000 fleet has not poured its first follow-on unit. The BWRX-300 will not run until the end of the decade. TerraPower’s Gates-backed Natrium reactor breaking ground at a retiring coal plant in Wyoming is the cleanest single image of where this decade is heading, and it is also first-of-a-kind, which is the phase that has humbled everyone who entered it. The difference between this round and the last is not certainty. It is structure: proven designs, behind balance sheets, built more than once. That is the only configuration that has ever worked.

France built it once and forgot how. America built it twice — Vogtle and Summer — and nearly swore off it. The question now is whether either country can do the one thing neither has managed since the 1980s: build the same proven reactor a second time, and a third, cheaply enough that the third is the argument for the fourth.

A software economy scales by copying code. An industrial economy scales by preserving crews, suppliers, permits, financing channels, and muscle memory. Nuclear is the place where America finds out whether it still has the second kind of memory — and the Rust Belt, which holds most of what remains of it, is where the answer will be found or lost.

The reactors were always the easy part. They were the easy part in 1974, and they are the easy part now. What France had and lost, and what America never built, was the machine that builds the machine.

WORKS CITED & SOURCES

Grouped by claim. Primary and canonical sources favored; some outlets are named where the original is paywalled.

France — the Messmer Plan and the buildout

How France achieved the world’s fastest nuclear buildout, Works in Progress — https://worksinprogress.co/issue/liberte-egalite-radioactivite/

History of France’s civil nuclear program, Wikipedia — https://en.wikipedia.org/wiki/History_of_France%27s_civil_nuclear_program

The beginning of nuclear energy in France: Messmer’s plan, IAEA INIS — https://inis.iaea.org/records/czje0-6cv23

France — the 2022 outages

Nuclear Power in France, World Nuclear Association — https://world-nuclear.org/information-library/country-profiles/countries-a-f/france

RTE (French grid operator) — https://www.rte-france.com/en

Flamanville 3 — cost and schedule

Cour des comptes report, via Connaissance des Énergies (€20.4bn in 2015 euros / €23.7bn in 2023 euros; original €3.3bn) — https://www.connaissancedesenergies.org/afp/programme-depr-la-cour-des-comptes-publie-un-rapport-critique-et-recalcule-le-cout-de-flamanville-3-250114

Energy Intelligence, on the Cour des comptes €110–120/MWh estimate — https://www.energyintel.com/0000017b-a7db-de4c-a17b-e7db0a550000

Vogtle & V.C. Summer

Plant Vogtle Unit 4 begins commercial operation, EIA — https://www.eia.gov/todayinenergy/detail.php?id=61963

Two Years After Completion, Plant Vogtle Still Looms…, Inside Climate News ($36.8bn final, 7 years late) — https://insideclimatenews.org/news/10052026/plant-vogtle-nuclear-debate-two-years-after-completion/

What Was Learned from Building New Nuclear Reactors?, POWER (15-year schedule) — https://www.powermag.com/what-was-learned-from-building-new-nuclear-reactors/

Vogtle project update, AP via ANS Nuclear Newswire (Summer abandonment; cost milestones) — https://www.ans.org/news/article-3949/vogtle-project-update-cost-likely-to-top-30-billion/

Regulation, culture, and political economy

It’s the Regulation, Stupid, The Breakthrough Institute (Calvert Cliffs, regulatory ratchet) — https://thebreakthrough.org/journal/no-20-spring-2024/its-the-regulation-stupid

Why Does Nuclear Power Plant Construction Cost So Much?, Institute for Progress (Eash-Gates study) — https://ifp.org/nuclear-power-plant-construction-costs/

Bernard Cohen, The Nuclear Energy Option, ch. 9 (regulatory ratcheting) — http://www.phyast.pitt.edu/~blc/book/chapter9.html

Jack Devanney, Nuclear is too Expensive (ALARA; Korea vs. U.S. cost) — https://jackdevanney.substack.com/p/nuclear-is-too-expensive

Three Mile Island accident was eerily foreshadowed by a Hollywood blockbuster, WHYY (The China Syndrome, 16 March 1979; TMI, 28 March 1979) — https://whyy.org/articles/three-mile-island-accident-was-eerily-foreshadowed-by-a-hollywood-blockbuster-days-before/

Korea vs. U.S. build cost

Heavy Manufacturing of Power Plants, World Nuclear Association (forging capacity; Doosan) — https://world-nuclear.org/information-library/nuclear-fuel-cycle/nuclear-power-reactors/heavy-manufacturing-of-power-plants

Jack Devanney, Nuclear is too Expensive (Korea ~$2,000/kW; Vogtle >$10,000/kW) — https://jackdevanney.substack.com/p/nuclear-is-too-expensive

The Westinghouse / AP1000 partnership ($80B)

United States Government, Brookfield and Cameco announce transformational partnership, Cameco (28 Oct 2025) — https://www.cameco.com/media/news/united-states-government-brookfield-and-cameco-announce-transformational-partnership

Cameco Form 6-K, SEC (partnership structure: 20% of distributions above $17.5bn) — https://www.sec.gov/Archives/edgar/data/0001009001/000119312525253372/d935274dex991.htm

US Government Announces Historic $80 Billion Nuclear Partnership…, K&L Gates — https://www.klgates.com/US-Government-Announces-Historic-80-Billion-Nuclear-Partnership-with-Westinghouse-Electric-Company-Cameco-Corporation-and-Brookfield-Asset-Management-to-Construct-AP1000-Reactor-Fleet-10-30-2025

US partners with Westinghouse, Cameco and Brookfield on $80B nuclear deployment, Utility Dive — https://www.utilitydive.com/news/westinghouse-cameco-brookfield-nuclear/803999/

SMRs — BWRX-300, NuScale, TerraPower

GEH BWRX-300 SMR Approved for Construction at OPG’s Darlington Site, Neutron Bytes (construction May 2025; first unit ~2030) — https://neutronbytes.com/2025/05/17/geh-bwrx-300-smr-approved-for-construction-at-opgs-darlingtion-site/

BWRX-300, Wikipedia (OPG timeline; final investment decision May 2025) — https://en.wikipedia.org/wiki/BWRX-300

NuScale / UAMPS Carbon Free Power Project cancellation, 2023 — reported by Reuters and the U.S. Department of Energy (search “NuScale UAMPS Carbon Free Power Project terminated 2023”)

Supply chain & FOAK to NOAK

Feds in $80 billion Partnership with Westinghouse to Build AP1000s, Neutron Bytes (leverage of the Vogtle-era supply chain) — https://neutronbytes.com/2025/10/28/feds-in-80-billion-partnership-with-westinghouse-to-build-ap1000s/

NSI report addresses supply chain bottlenecks, ANS Nuclear Newswire (25–30% order-book savings) — https://www.ans.org/news/article-7870/nsi-report-addresses-supply-chain-bottlenecks/

Nuclear supply chain under pressure in a fragmented world, Damona (East-Asian forging concentration) — https://www.damona.co/nuclear-supply-chain-under-pressure-in-a-fragmented-world/

Financing frame — modern mercantilism, the AI-power thesis, Green Premium

Bridgewater Associates / Greg Jensen, We’re All Mercantilists Now — bridgewater.com (Research & Insights)

Bridgewater Associates, Power Politics: Energy Self-Sufficiency in a Modern Mercantilist World (Oct 2025) — bridgewater.com (Research & Insights)

U.S. Energy Information Administration, international electricity data (China vs. U.S. generation) — https://www.eia.gov/international/data/world

Bill Gates, How to Avoid a Climate Disaster (the “Green Premium”) — gatesnotes.com

A note on the figures referenced in the charts: dollar and euro totals are rounded; the AP1000 and BWRX-300 economics are forward commitments, not realized costs. The “mercantilist lease” is an analytic characterization of the deal’s structure, not a legal description of ownership.

SUBSCRIBE

If you’ve read this far, you’re exactly who The Rustbelt Reader is written for — people who want to understand the physical economy as it actually works: the capital, the supply chains, the institutions, and the industrial memory that decide what gets built and what doesn’t.

Subscribe to get every essay in your inbox. Free subscribers get the full pieces. It’s the best way to make sure the next one finds you.

And if this clarified something, forward it to one person who’d argue with it.

The very first fair and comprehensive analysis of where we are and how we arrived here, that I have ever seen. Congratulations!

I would like to have seen mention of Copenhagen Atomics progressive design pathway and business plan for modular thorium reactors. Using nuclear engineering principles validated by the US in the early 1960s at Argonne and elsewhere, at a time when nuclear powered aircraft were being actively considered. Reportedly the lack of bomb suitable byproducts was an ironic disqualifier for further development.

By planning a modular, serially upgradeable design, Copenhagen seem to solve the problems of latent design flaws (pull the defective module and replace with newer) and flexible scaling to adapt to load changes. That their design is inherently walk away safe from the types of catastrophic high-pressure explosive events which require the massive concrete and steel containment structures that are required for most of the old designs, should make multiple real world prototype testing feasible. We learn to make bricks individually, not as completed houses. https://www.copenhagenatomics.com/

The end goal of a breeder capable of consuming the problematic, inefficiently burned nuclear fuel waste of the last 60 years would also seem a major incentive to develop at speed. One wonders why the leader of the Swiss Greens decided to launch a Soviet made rocket attack on the Superphénix fast-breeder nuclear plant in Creys-Malville under construction in 1982? That the progressive Left was a strong part of the 1950s Anti Nuclear movement which later linked fear of weapons to opposition to peaceful utility power, all while the Soviets were vigorously expanding both, raises suspicion about motivation.

The current "Climate Emergency" campaign, prominently linking the iconic, parabolic cooling towers, now a symbol of "nuclear hazard" in the public mind, with the clouds of white water vapor relabeled as "carbon(sic) pollution" makes one wonder what powerful interests are being served.

What is wrong with my line of thought?