Follow-up to “Trump’s Orinoco Deal” and “The Permission Layer”

January 7, 2026 — By Dante Alighieri

Pittsburgh, PA

Washington can open the legal gate. But Caracas still has to clear the breakeven.

In my first two notes, I framed Venezuela as a two-part system:

The Physical Layer: the rusted pipes, upgraders, and dilution needs.

The Permission Layer: sanctions, licenses, shipping/insurance, and payment rails.

This dispatch adds the third and final constraint: the Allocation Layer—the boardroom reality that capital has options.

Even if Washington flips the permission switch back on, Big Oil boards will still ask a blunt question: Why deploy billions into high-cost Venezuelan barrels when the market is full of lower-cost ones?

BloombergNEF’s blunt baseline: this is “discount oil”

Start with the molecule itself. Orinoco crude is extra-heavy and sour—more like industrial paste than West Texas “pump-and-go.” That chemistry creates two structural penalties:

The Diluent Tax: you need lighter hydrocarbons (condensate/naphtha) just to make it flow.

The Refinery Tax: you need expensive, specialized hardware—like cokers—to turn it into high-value products.

Because of that, Orinoco barrels don’t sell for the headline benchmark price. BloombergNEF notes Venezuelan heavy crude typically trades at a structural discount (on the order of ~$7–$10/bbl below WTI in their framing, before you add sanction/market frictions).

Thus, before drilling or rehab, your revenue “ceiling” is lower than lighter competitors.

The competition: a brutal hierarchy

Venezuela’s problem isn’t just its own rust—it’s that the rest of the world got better at drilling while Venezuela stood still.

Money is fungible. A dollar invested in the Orinoco is a dollar not invested in Texas or Guyana. And when boards compare projects, they start with one question:

What oil price do we need to make this investable?

BloombergNEF sketches the competition clearly:

Guyana: breakevens near ~$35/bbl (BNEF estimate)

Permian Midland Basin: around ~$48/bbl average (BNEF estimate)

Canada (oil sands): about ~$55/bbl (as commonly cited in the Reuters/WoodMac comparison)

Then comes the Venezuelan headache. Reuters, citing Wood Mackenzie, reports breakevens for key Orinoco grades averaging more than $80/bbl for new production.

That’s why Reuters calls the opportunity a potential “poisoned chalice”: the resource is massive, but the cost—and risk—stack is not naturally competitive.

A quick nuance: not apples-to-apples barrels

This isn’t “Orinoco vs Permian” as identical barrels. Orinoco is a system barrel—diluent, logistics, often upgrading burden, and downstream fit. The Permian is a light system optimized for low-cost upstream and export netbacks.

But boards still compare them because the decision is the same everywhere: where does the next $1B go?

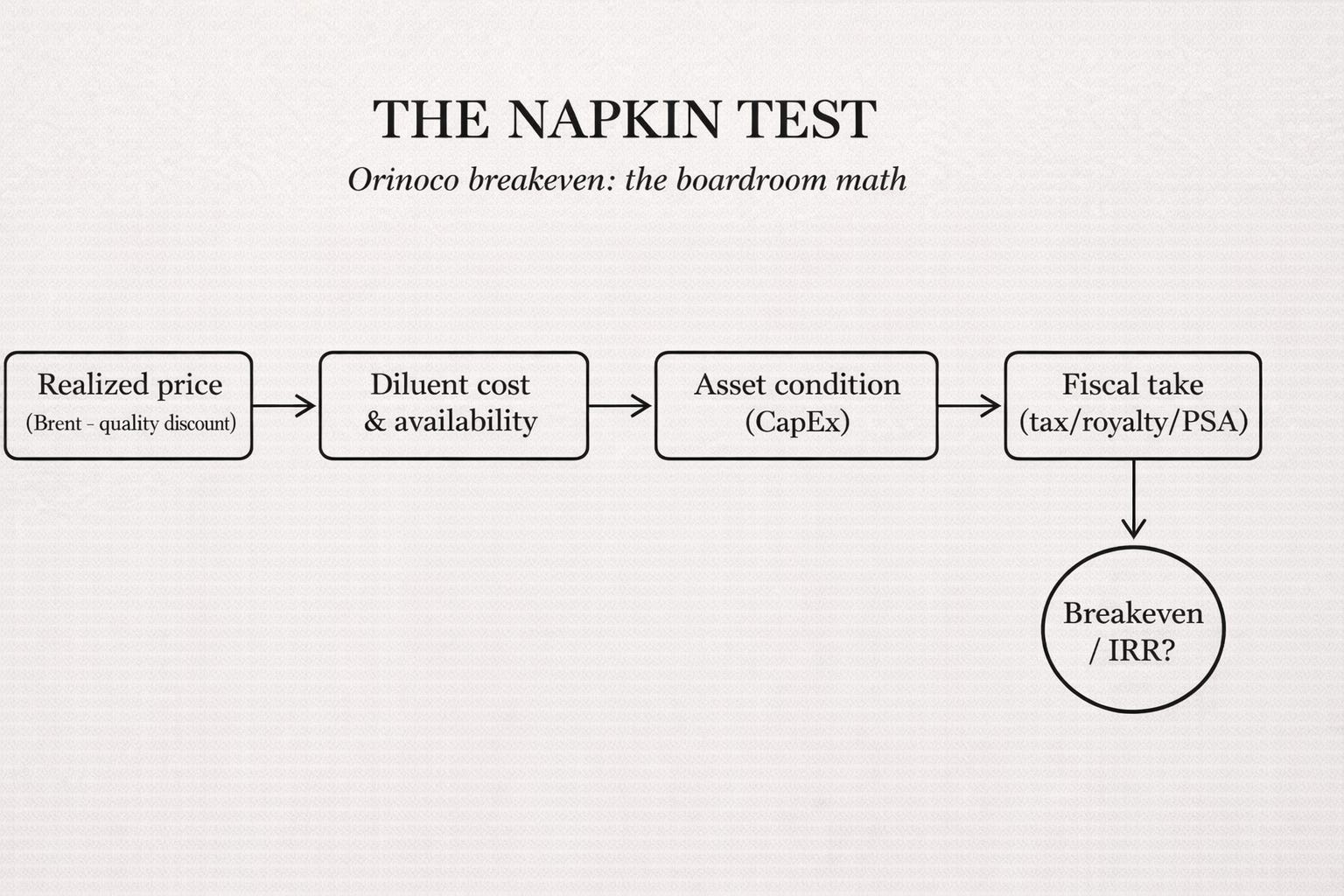

The Napkin Test: why the math sucks

You don’t need a complex spreadsheet to see the trap. You need one napkin and four line items.

To make money, an Orinoco barrel has to survive four hits:

1) The Discount Hit

You’re selling WTI minus a heavy-sour discount—and that’s before permission-layer friction widens the spread.

2) The Diluent Hit

You have to buy and move diluent just to keep crude moving. In heavy systems, diluent isn’t a nice-to-have—it’s the flow enabler.

3) The Rust Hit (Rehab capex)

This is not “turn the valve.” It’s brownfield rehab—upgraders, pumps, lines, power, reliability. Wood Mackenzie notes Orinoco upgraders largely went offline in 2019–2021 and that those still running require consistent spend to keep operating.

4) The Government Hit (the killer variable)

If fiscal terms are heavy—royalties, taxes, JV structures—the breakeven explodes. High cost plus high state take is how “oil-rich” becomes “uninvestable.”

The result:

When you add Discount + Diluent + Rust Repairs + Government Take, the price of oil required for a company to keep real profit gets very high—fast.

“Get the oil flowing” isn’t a political slogan. It’s an arithmetic test.

What changes the answer: when government makes the barrel investable

The Orinoco doesn’t win capital just because the permission layer reopens. It wins when government action changes the cash math—either by shrinking the discount stack, lowering upfront risk, or rewriting fiscal terms.

Here are the levers that actually move the boardroom model—and the evidence Washington is at least considering some of them:

Discount compression (make the barrel “clean” to trade)

The fastest way to raise realized prices is to remove the frictions that widen differentials—shipping/insurance risk, payment risk, and murky legality. That’s why the administration’s stated goal isn’t merely “production,” but controlling how barrels are sold and where proceeds go. Energy Secretary Chris Wright said the U.S. wants Venezuelan oil sold with revenues routed through U.S.-controlled accounts, explicitly framing it as leverage and a way to make the system function again.Reliable diluent access (solve the binding operating constraint)

Heavy oil doesn’t move without diluent. Government can’t change viscosity, but it can change access—by opening procurement channels, clarifying licensing for imports/exports, and enabling the logistics that keep diluent flowing. BloombergNEF flags operational constraints and the heavy-barrel discount dynamics as core hurdles to any “renaissance.”Lower rehab cost per barrel (shift risk off private balance sheets)

Brownfield Venezuela is a rehab project, not a drilling story. If Washington wants private capital to do the work quickly, it has to change who eats the early capex risk. Reuters reported Trump said the U.S. may subsidize oil companies to rebuild Venezuela’s energy infrastructure. And Axios reported Wright said the administration is considering compensating U.S. oil firms that invest.A fiscal reset (the decisive variable)

Even with subsidies, the project doesn’t clear if the host government take is too high or contracts aren’t enforceable. This is where “government intervention” matters most: new fiscal terms, credible arbitration/enforcement, and stable export rules. Reuters also reported Washington is pressing majors to finance large investments if they want to recover Venezuelan debts/arbitration-related claims—another form of state-directed structuring of incentives.

Bottom line: breakeven falls when the deal works—lower state take, enforceable rules, and a legal/financial on-switch that makes the barrel bankable. And the latest Washington signals suggest they’re exploring exactly that toolkit: revenue control mechanisms, subsidies/compensation, and structured terms to pull Big Oil into the rehab.

Closing

Wood Mackenzie’s public view is the bridge between our “permission layer” thesis and the boardroom math: Venezuela can rebound with operational improvements and investment under favorable conditions—but sustaining and expanding beyond that requires real capital and consistent execution.

Washington can open the gate.

But licenses don’t drill wells—capital does. And capital is trained to go where costs are low, terms are durable, and the discount stack is stable.

But capital flows are evolving. More coming on that soon.

Stop reading the headlines. Start doing the math.

Politics creates speeches, but economics creates barrels. If you want to understand the physical and financial realities behind the energy transition—and why “energy independence” is harder than it looks—subscribe to The Rustbelt Reader. We track the intersection of industry, policy, and price.

Sources

BloombergNEF — Venezuela’s Oil Renaissance Faces Several High Hurdles (Jan. 6, 2026).

Reuters — Wood Mackenzie breakeven comparison and “poisoned chalice” framing (Jan. 2026).

Wood Mackenzie — What could change in Venezuela mean for oil production? (Dec. 5, 2025).

Quick follow-up for the “breakeven”. Here’s the napkin test I’m using:

Brent breakeven ≈ (All-in $/bbl ÷ (1 − govt take)) + Total discount

• All-in $/bbl = ops + diluent + logistics + “rust rehab” capex (spread over barrels)

• Govt take = royalties/taxes (the swing factor)

• Total discount = heavy/sour quality + any market/permission friction

Example (pure napkin): if all-in costs are ~$50/bbl, govt take ~15%, and total discount ~$20/bbl, then breakeven is ~($50/0.85)+$20 ≈ $79 Brent. If either discount widens or govt take rises, the breakeven jumps fast—which is why “get the oil flowing” ultimately has to clear boardroom math, not just headlines.

You clearly know a great deal more about this than I do, albeit a low bar. Thanks for the very enlightening exposition on the economics of VZ oil.

I conclude that total ignorance of this and basic economics on the part of Chaviatas is what led to the decline and fall of their country.

Question: Given the challenges you cite, why are China and Russia so interested in VZ crude?