The Magnequench Parable

How America Sold a Choke Point—and Learned What a “Gloved” Market Looks Like

By Luca Pacioli | The Rustbelt Reader

January 16, 2026 | Pittsburgh, PA

“The capitalists will sell us the rope with which we will hang them.”

- Vladimir Lenin (attributed)

America’s civic religion treats “the market” like a force of nature—impersonal, neutral, almost moral. China treats markets more like strategic terrain: something the state can grade, irrigate, fence, and weaponize. Adam Smith’s invisible hand was never invisible in China. It simply wore a glove.

If you want a millennial U.S. case study of what a gloved market can do to an ungloved one, you don’t need to start with TikTok.

Start with a small, forgettable divestiture from the 1990s:

Magnequench.

Why GM sold, and who bought, matters because it’s the mechanism — not the moral.

GM treated Magnequench like a non-core industrial asset in a 1990s era of restructuring and portfolio triage, the kind of divestiture Wall Street rewards precisely because it turns long-cycle manufacturing into near-term financial cleanliness.

The buyer, however, was not simply “the market.” Multiple academic and policy treatments describe GM selling Magnequench to the Sextant Group, an investment vehicle led by Archibald Cox Jr., with backing from two Chinese state-linked firms often identified as San Huan New Material and China National Nonferrous Metals Import & Export Corp.

And the state linkage wasn’t abstract. The buyers were politically wired. One account notes that the new Chinese chairman of Magnequench, Hong Zhang, was married to Deng Xiaoping’s daughter Deng Nan. Another account describes the other Chinese investor in the deal as being run at the time by another Deng son-in-law—a reminder that this wasn’t merely “Chinese capital” in the generic sense, but Chinese capital moving through the ruling family’s orbit.

Washington reviewed the deal; the Clinton administration allowed it to proceed, reportedly with conditions tied to keeping operations in the U.S. for a period — the kind of paperwork safeguard that looks comforting on signing day and weightless later.

And then there’s the motive that hangs over the whole episode: China’s market access. Contemporary reporting and later commentary note that union leaders and critics suspected GM’s willingness to accommodate Chinese interests was entangled with its broader push to compete in China’s auto market — not “bribery” in a suitcase sense, but the subtler, era-typical trade: cooperation for permission.

The Rope Has a Precedent

This is not the first time America has learned—too late—that “private optimization” can collide with national survival.

In April 1942, TIME described the uproar over Standard Oil of New Jersey’s prewar patent and cartel arrangements with Germany’s I.G. Farben—an arrangement alleged to have constrained or delayed parts of America’s synthetic rubber push right as the world turned hostile. Whatever the final legal texture, the historical rhyme is the point: peacetime deals can become wartime liabilities.

That is the same rhyme Magnequench repeats—only the commodity is not rubber.

It’s torque.

The Thing Detroit Didn’t Know It Was Building

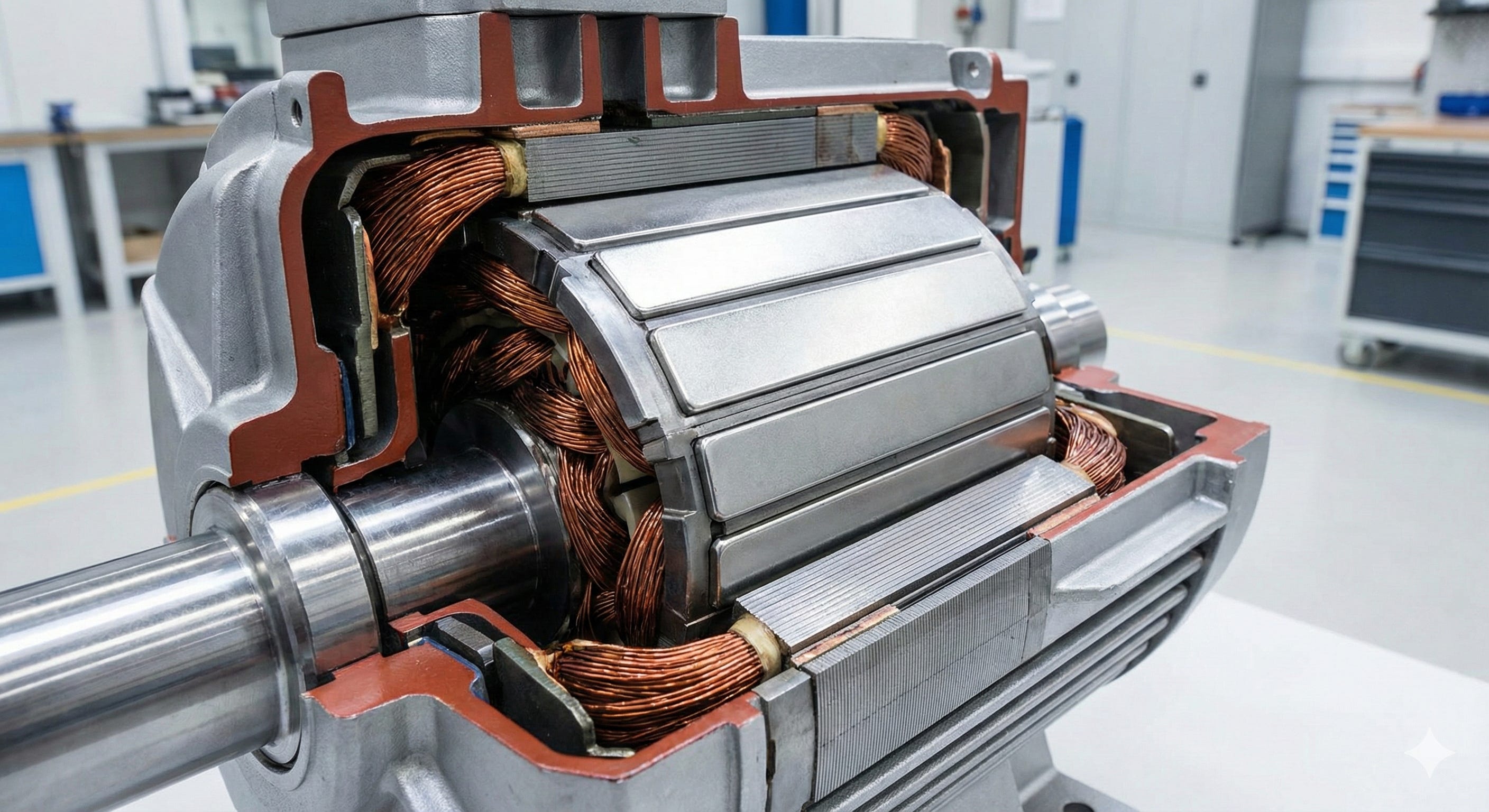

Rare-earth magnets are easy to trivialize because the word magnet sounds domestic—refrigerators, toys, gadgets.

But neodymium-iron-boron (NdFeB) permanent magnets are miniaturized torque: powerful motion and guidance in small spaces. They sit inside the “boring” components modern life quietly depends on—motors, servos, actuators—and they sit inside the components modern militaries depend on too.

They also hide in your pocket. As one U.S. magnet-maker put it on national television, there are “probably 12 magnets” in an iPhone, and “up to 40 magnets” in a car. That is not a boutique input. That is a foundational one.

Which is why Magnequench was never just a factory story.

It was a capability story.

The Choke Point Isn’t the Mine

Here is the misconception that makes the screw-up look smaller than it was:

When most people hear “rare earths,” they picture geology—who owns the dirt.

But leverage doesn’t primarily live in the hole in the ground.

It lives in what comes after:

Ore → Separation → Metals/Alloys → Powder → Magnet-making → Finished Systems

That middle stretch—the conversion layer—is where raw material becomes usable power. And that is where the choke point concentrates.

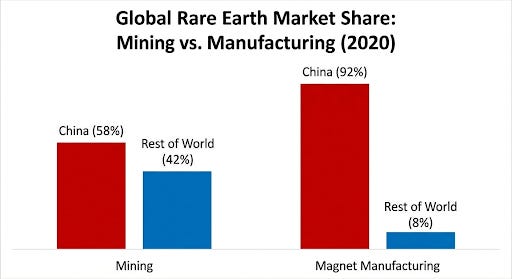

Reuters puts the asymmetry bluntly: China mines about 60% of the world’s rare earths, but makes about 90% of rare-earth magnets. CBS, citing Wood Mackenzie, frames the downstream dominance as even more extreme—as much as 95% of global rare-earth magnets.

So no—GM did not need to “own rare earths” for Magnequench to matter.

Owning the molecule is not owning the capability.

The “Gloved Hand” Logic

Here’s where Americans tend to flinch, because it insults our operating myth.

In a pure quarterly optimizer, the rational decision is: buy the cheaper input.

In a security optimizer, the rational decision is: buy the leverage—even if it loses money this year.

China didn’t “beat” markets. It instrumentalized them—using policy, licensing, infrastructure, and strategic ownership to shape what “rational” means over a longer horizon than a Western earnings call. And when it wants leverage, it does not need to invade. It can license.

Reuters’ export-control summary spells out the mechanism: licenses that industry sources said could take “two to three months or longer,” with shipments halted at ports as applications are processed.

Rare-earth magnets are not a normal input.

They’re a leverage input.

“Okay—but what exactly did GM lose?”

Not just a logo on a building. Not just a line item in a divestiture deck.

The true asset GM—and the country—lost wasn’t “ownership of dirt.”

It was the stuff you can’t spreadsheet cleanly:

Process know-how: powder processing, sintering, yield discipline, quality control, tooling—the tacit craft that lives in engineers and operators, not in PowerPoints.

Scale capability: the gap between “we can do it in a lab” and “we can do it reliably at volume.”

Ecosystem gravity: once the conversion layer relocates, everything that depends on it clusters nearby.

Option value: the ability to surge production without asking a rival for permission.

And here’s the high-stakes receipt that turns this from “sad globalization story” into “strategic malpractice”:

In a 2006 congressional hearing record, Senator Evan Bayh cited Magnequench as making “80 percent of the rare earth magnets that allow our smart bombs to function,” and warned plainly: “It is not very smart to rely on China for a critical component of an important weapons system for our country.”

That is the difference between a commodity and a choke point.

The Bill Comes Due

In April 2025, China tightened controls on rare-earth-related items and pushed exporters into a licensing regime. Reuters described the effect in the plainest possible terms: manufacturers raised the alarm; licenses could take months; shipments halted at ports.

But the best description of the problem is not a white paper. It’s a sentence from an Oklahoma warehouse.

USA Rare Earth CEO Joshua Ballard told CBS News: “Right now, we have to ask permission from China…” calling it an “incredible choke point.”

That’s what the conversion layer means in the real world: not scarcity in the ground, but discretion at the gate.

And the glove has been tightening, not loosening. Reuters later reported expanded controls and rules designed to reach beyond China’s borders—requiring compliance even for some foreign producers whose products contain Chinese material or use Chinese equipment.

Then came the paradox that should make every “the market will handle it” argument sweat: Reuters reported China’s total rare-earth exports in 2025 rose to 62,585 metric tons (highest since at least 2014), even as restrictions tightened on several medium-to-heavy elements. The lever is not “China has none.” The lever is China can choose.

That’s what a gloved market looks like in practice: not the absence of supply—the discretion over supply.

The Rebuild—and the Scale of the Hole

Now the West is paying the stupid tax: rebuilding the conversion layer it treated as disposable.

Neo Performance Materials—one of the industrial successors in this lineage—frames the scale problem in a way that should sober anyone who thinks this is “easy to reshore.” Its Q3 2025 MD&A describes an EU Just Transition Fund–supported permanent magnet facility projected to produce 2,000 metric tonnes per year in Phase 1A, with plans to scale to over 5,000 mt/year in Phase 1B.

And in the investor presentation, the company juxtaposes that buildout with a brutal benchmark: estimated permanent magnet demand outside China of 251,000 MT (2035 estimate).

That’s the definition of a choke point.

And even the would-be rebuilders admit the calendar is unforgiving. Ballard told CBS the U.S. is “a good 10, 15 years behind” where rare-earth magnet production should be. In the same report, he said his company is assembling machines intended to produce up to 5,000 tons of magnets per year—and even that would be only about 10% of U.S. demand.

That is the rebuild era in one statistic: a heroic effort… to claw back a tenth.

Rules and Reflections

Here’s the simple test for a gloved market:

Can a rival’s paperwork stop your factory faster than a rival’s missiles?

If the answer is yes, three rules apply:

Rule #1: The conversion layer is the empire.

Owning resources is not the same as owning capability. The industrial middle—where raw becomes usable power—is where leverage concentrates.

Rule #2: If profit is the only optimizer, resilience will be liquidated.

Quarterly governance will always sell strategic insurance—until the premium comes due.

Rule #3: In a world of gloved markets, supply chains are foreign policy.

If a rival can throttle your inputs with licensing, you are not a superpower.

You’re a customer.

And customers don’t get to dictate terms.

Join the Revival

If you believe industrial history isn’t just the past—but the blueprint for the next era—subscribe to The Rustbelt Reader. We cover how industrial capacity becomes political power—and what it takes to rebuild both in America’s next cycle.

Read More

Sources & Footnotes

China’s export controls, market share framing (≈60% mining; ≈90% magnets), and licensing delays: Reuters explainer (June 4, 2025).

Expanded restrictions and extraterritorial-style compliance rules: Reuters (Oct 10, 2025).

China’s 2025 rare-earth export totals (62,585 metric tons) and April restriction context: Reuters (Jan 14, 2026).

Neo Performance Materials Q3 2025 MD&A: EU Just Transition Fund support; Phase 1A 2,000 mt/year; Phase 1B >5,000 mt/year; capex and grant reimbursement notes.

Neo Performance Materials Q3 2025 investor presentation: “Estimated Demand Outside of China: 251,000 MT (2035 estimate)” (Adamas Intelligence).

Magnequench “smart bombs” choke point quote and “not very smart to rely on China…”: U.S. congressional hearing record (2006).

Standard Oil–I.G. Farben controversy as U.S. historical analog: TIME (April 6, 1942).

Oklahoma rebuild scene, dominance framing (“as much as 95%”), “permission” quote, magnets-in-iPhone/car, 5,000 tons = ~10% of U.S. demand, and “10–15 years behind”: CBS News (June 5, 2025).

Really insightful. Reminds me of another huge issue I was reading about in the crazy shortage we have in plumbers, electricians and construction workers in general. For two generations everyone has been told they had to go to college, take on lots of debt, and work in a cubicle doing random soulless stuff.