The Last Privilege

50-year American subsidy is quietly ending. The bond market is the first place to feel it.

In 1965, Valéry Giscard d’Estaing gave the United States a name for something his country had complained about for years. He called it the exorbitant privilege.

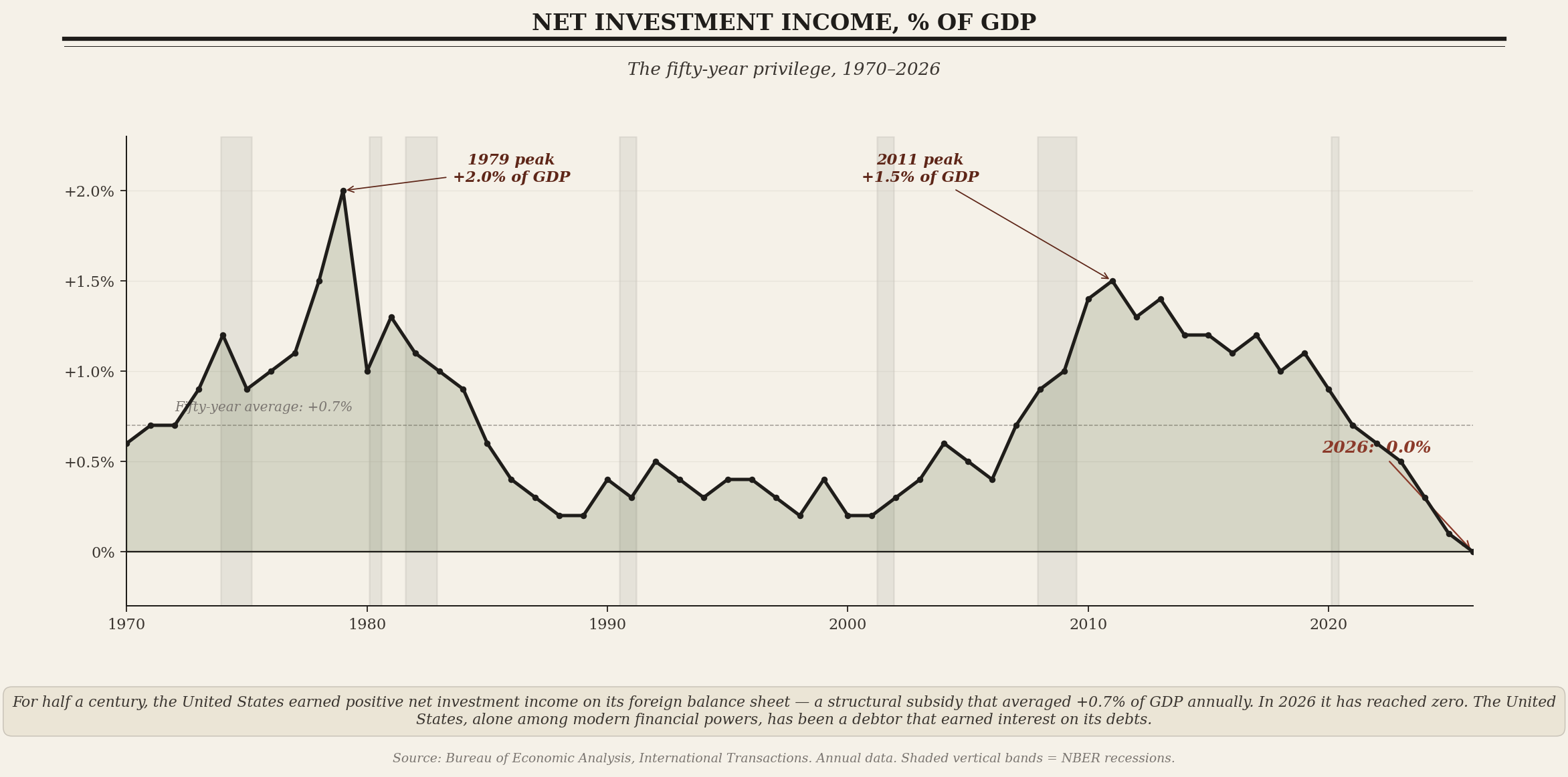

The privilege had a specific mechanism. The United States borrowed from the world in safe, low-yielding instruments — Treasuries, agency MBS, dollar deposits — and invested in the world through risky, high-yielding ones — foreign direct investment, controlling equity stakes, portfolio equity. The asymmetry generated a steady stream of positive net income flowing back to American shores, despite the United States being the world’s largest net debtor. At its 2011 peak, that stream reached roughly 1.5% of GDP — approximately $250 billion per year in today’s terms.

Compounded over five decades, this represents trillions of dollars in foregone interest payments and trillions in foreign earnings that flowed home rather than being reinvested locally. No other country in modern economic history has managed it on a comparable scale. Spain after its silver empire could not. The Netherlands after its commercial empire could not. Britain after its industrial empire could not. Each transitioned from creditor to debtor and paid the corresponding costs.

The United States, alone, has been a debtor that earned interest on its debts.

That period is ending. As of 2026, US net investment income has reached zero — the lowest reading since the United States became a structural net debtor in the 1980s. The decline has been steady, multi-year, and visible in plain Bureau of Economic Analysis data.

The mechanism is breaking down on both sides simultaneously.

US borrowing costs have risen as Treasury rates normalized to 4-5%. Foreign equity returns have stagnated as European demographic decline, Chinese balance sheet contraction, and EM debt accumulation compress the yields earned on US assets abroad. The spread that generated the privilege — between what the United States paid on its debts and what it earned on its foreign holdings — has compressed from 3.2 percentage points at its 2011 peak to roughly 0.2 percentage points today.

The privilege did not require any policy decision. Its erosion has not required one either.

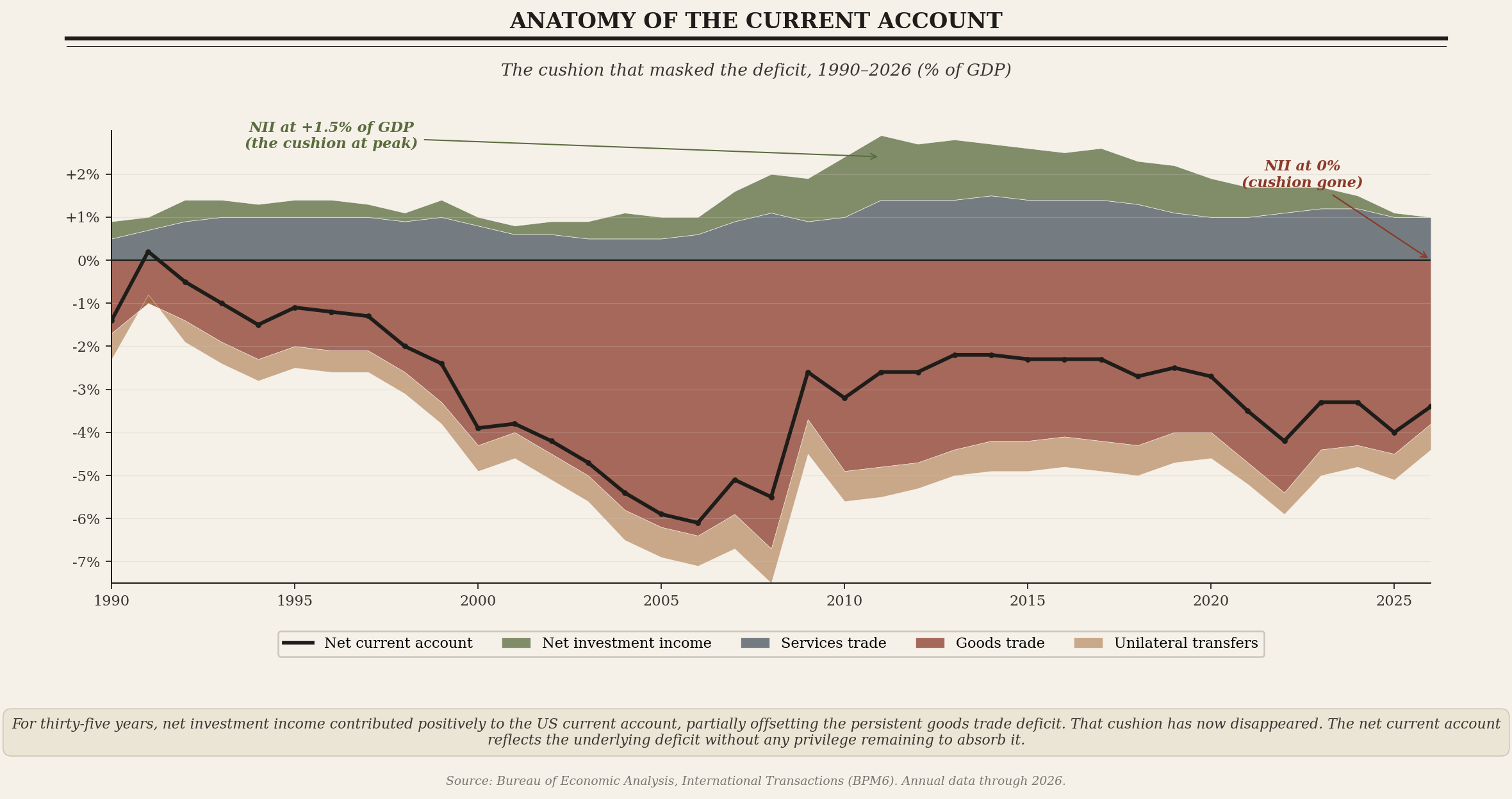

The consequences are now becoming visible in the broader external accounts.

A 1.5-percentage-point swing in net investment income — from +1.0% of GDP in 2019 to zero today, with further decline likely — represents a structural widening of the US current account deficit independent of any change in trade flows. The deficit was 2.3% of GDP in 2017. It is 3.4% today. It will likely reach 4.5-5% by 2030 even if trade balances remain unchanged. The widening is being driven not by Americans consuming more imports relative to exports, but by the underlying mathematical reality that disappearing investment income must be replaced by other forms of external financing.

This is the structural pressure beneath the trade policy disputes of this decade. Tariffs, industrial policy, and re-shoring debates are predictable responses of a political system whose external position has become structurally harder to fund. Late Habsburg Spain reached for bullion controls when its silver surpluses dwindled. Britain embraced imperial preference in the 1930s after the gold standard collapsed. When structural advantages erode, political systems reach for second-best tools.

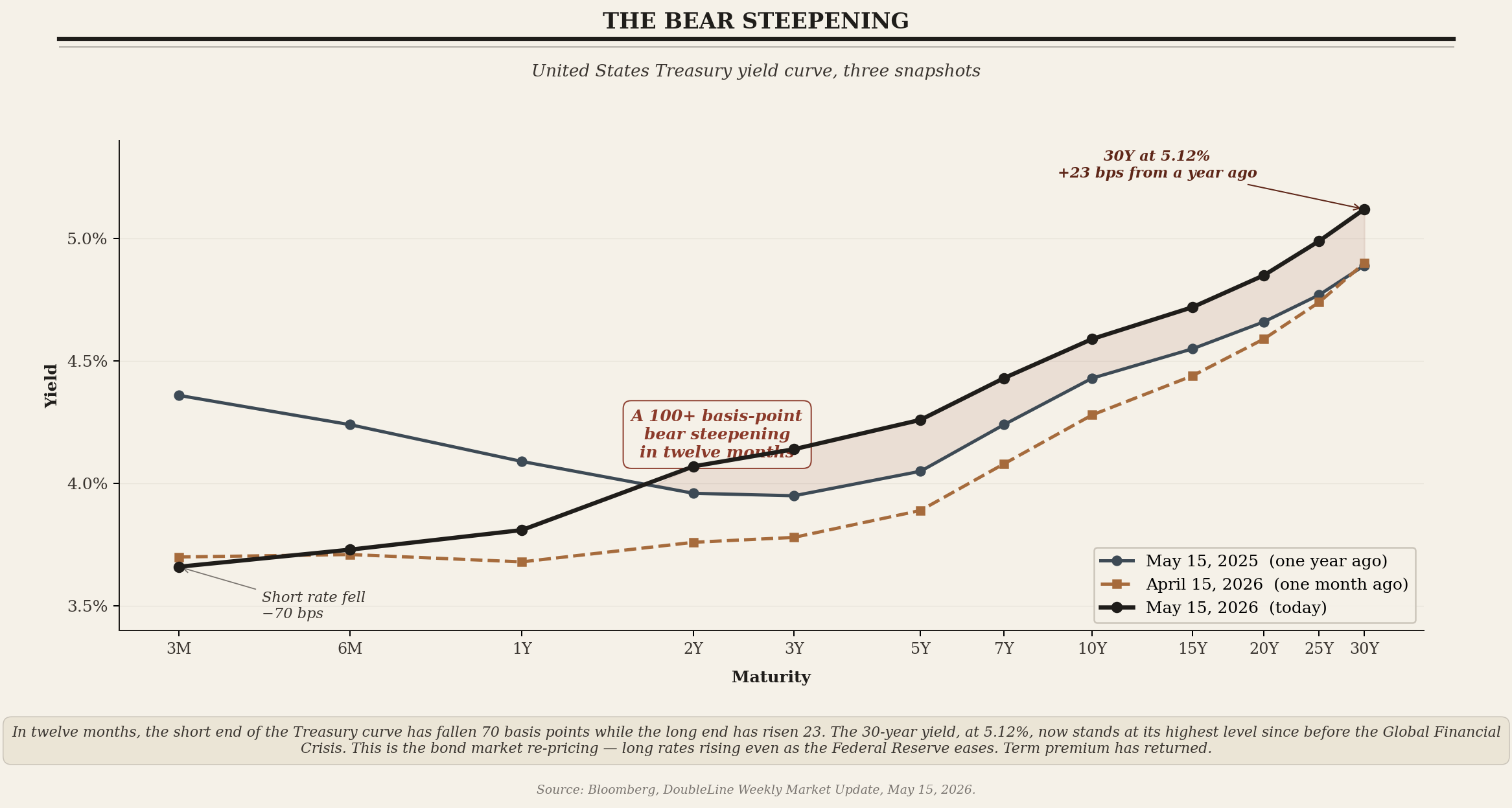

The most immediate consequence is playing out in the United States Treasury market.

The connection runs through a mechanism rarely named explicitly. For decades, the US trade deficit has been financed by what economists call dollar recycling. Americans buy foreign goods. Foreigners receive dollars. Foreigners overwhelmingly choose to hold those dollars in US financial assets rather than converting them into other currencies. Chinese exporters’ dollar earnings recycled through the PBOC into Treasuries. German trade surpluses found their way into US corporate bonds. Saudi oil revenues recycled into American real estate and equities. The mechanism did not change for fifty years.

When foreign preference for US assets weakens, the recycling weakens with it. The dollars still get earned. They are increasingly recycled into gold, into domestic investment, into other countries’ bond markets. They flow into US Treasuries with less consistency and at progressively higher yields.

The recycling never stopped. The willingness behind it did.

Three trends now operate simultaneously. Federal deficits at 6% of GDP combined with Federal Reserve balance sheet runoff have produced net new private-market Treasury supply of roughly $2.5 trillion annually since 2023 — four times the 2010s average. Foreign official holdings of Treasuries have fallen from 22% of outstanding in 2010 to about 12% today. The Federal Reserve itself has transitioned from being the marginal Treasury buyer to being a marginal seller — the largest reversal of central bank Treasury demand in modern monetary history.

The shape of the resulting re-pricing is visible in the curve itself. Over the past twelve months, the short end of the Treasury market has fallen by 70 basis points as the Federal Reserve began easing. The long end has risen by 23 basis points over the same period. A 100-basis-point bear steepening in a single year — long rates rising while short rates fall — is unusual. It happens when bond markets price structural concerns that monetary policy alone cannot resolve.

The Treasury market still functions. But every auction now clears slightly harder than the last, at slightly higher yields than expected. Regime change in fixed income markets is not a thunderclap. It is the accumulation of small frictions, sustained over years.

The dollar’s reserve status is not in imminent danger. It retains overwhelming network effects — roughly 60% of global reserves, 88% of FX transactions, 50% of trade invoicing. The euro at 20% has been declining since 2009. The renminbi at 2-3% lacks the open capital account required of a credible reserve asset.

But reserve currency status is not a switch. It is a spectrum.

The United States is moving from one end toward the other, slowly, in data that has been visible throughout the move. This is the regime change disappearing NII foreshadows — not a crisis, not a collapse, but a narrowing of degrees of freedom across every domain of policy. Fiscal policy becomes more constrained as borrowing costs rise. Monetary policy becomes more constrained as foreign capital flows turn price-sensitive. Trade policy becomes more constrained as external financing pressures grow. Strategic policy becomes more constrained as allies grow less willing to subsidize positions that no longer come with the financial benefits they once did.

The current Treasury and Federal Reserve leadership have acknowledged pieces of this. Secretary Bessent has made strengthening the Treasury market his central policy concern. Chair Warsh has acknowledged the disconnect between front-end policy rates and long-end yields. What neither has articulated publicly is the structural mechanism — the disappearing NII subsidy, the weakening dollar recycling — that connects current market signals to the longer arc of American financial position.

Treasury Secretaries cannot say that foreign demand is structurally weakening even when it is. Fed Chairs cannot say that fiscal dominance constrains them even when it does. That gap, between what officials can say and what the data shows, is the analytical space this argument tries to occupy.

The privilege did not arrive in a single year. It compounded across decades, quietly, in the gap between what America paid on its debts and what it earned on its assets.

The unwinding will look the same. Not a crisis. Not a collapse. A compounding, year by year, of constraints that did not previously bind.

The first decade of that compounding has already passed.

The reserve currency remains. The subsidy attached to it is thinning.

That's a really interesting piece. Fortunately for the U.S., we have just passed through the nadir in the long term macroeconomic cycle. However, this will begin to really bite as 2040 and the next nadir approaches.

A lot will depend upon how the Indian and Central Asian economies develop during the same period. Russia and Europe are collapsing economically. China is a five millennia old introverted snake eating its own tail. The Arabian Peninsula is hobbled by Islam and ancient conflicts and, we are now past Peak Oil. Africa will only ever be a Juju-obsessed resource pot for others. South America is the only remaining question mark.

The Trump Corollary to the Monroe Doctrine certainly appears a wise choice for several decades to come. Rebuild domestically to ensure resilience.