The Clearing Price

Balance-sheet utilization is the danger gauge of a financialized republic.

By Luca Pacioli | Pittsburgh, PA

“I used to think if there was reincarnation, I wanted to come back as the president or the pope. But now I want to come back as the bond market. You can intimidate everybody.”

— James Carville, 1993

Editor’s Note: This is a synthesis essay, drawing together two threads from this newsletter — the external-account series that traced how American financing became fragile, and the Mellon series that traced how the financial system lost its capacity to absorb pain. It also makes good on a promise: the previous external-account essay closed by saying a future piece would examine the operational mechanisms — Treasury market plumbing, the shadow liquidity system, the basis trade — that translate structural shifts into daily market behavior. This is that piece.

In the autumn of 2022, the British government discovered the price of its own debt in the space of three days.

On September 23, a new Chancellor announced a budget of unfunded tax cuts. The gilt market did not debate it. It repriced. Thirty-year yields, which had spent the prior decade below two percent, lurched toward five. And then the move stopped being about fiscal policy and became about plumbing. British pension funds had spent years running a strategy called liability-driven investment — leveraged positions in gilts, designed to match long-dated obligations, that worked beautifully until yields moved too far too fast. As gilt prices collapsed, the funds faced collateral calls. To meet them, they sold gilts. The selling drove yields higher. The higher yields triggered more collateral calls. The collateral calls forced more selling.

This is the part to hold onto. The spiral had nothing to do with whether Britain was solvent. Britain was solvent. It had everything to do with whether the market could absorb the selling — and the answer, for about forty-eight hours, was no. The Bank of England, which had been preparing to sell gilts as part of its inflation fight, was forced into an emergency reversal, pledging to buy up to £65 billion to halt the cascade. The Prime Minister who ordered the budget was gone in forty-four days.

The United States is not Britain, and the distinction matters. The Treasury market is not merely a national debt market; it is the collateral base of the global dollar system. That gives America advantages Britain did not possess in 2022: deeper demand, broader plumbing, standing swap lines, and a central bank whose liabilities are themselves the world’s funding instrument. The comparison is not a claim of equivalence. It is a claim of mechanism. In both cases, the danger begins when leveraged holders of sovereign debt become forced sellers into a market whose balance-sheet capacity is already constrained. Britain is not America’s forecast. Britain is America’s mechanism, demonstrated on a smaller sovereign three years ago.

The question that should occupy anyone who underwrites risk is therefore not whether the United States can fund itself. It is at what price, and how orderly the discovery of that price turns out to be.

The question is price, not solvency

Let me state the position plainly, because it is more useful than the catastrophist version that circulates in its place.

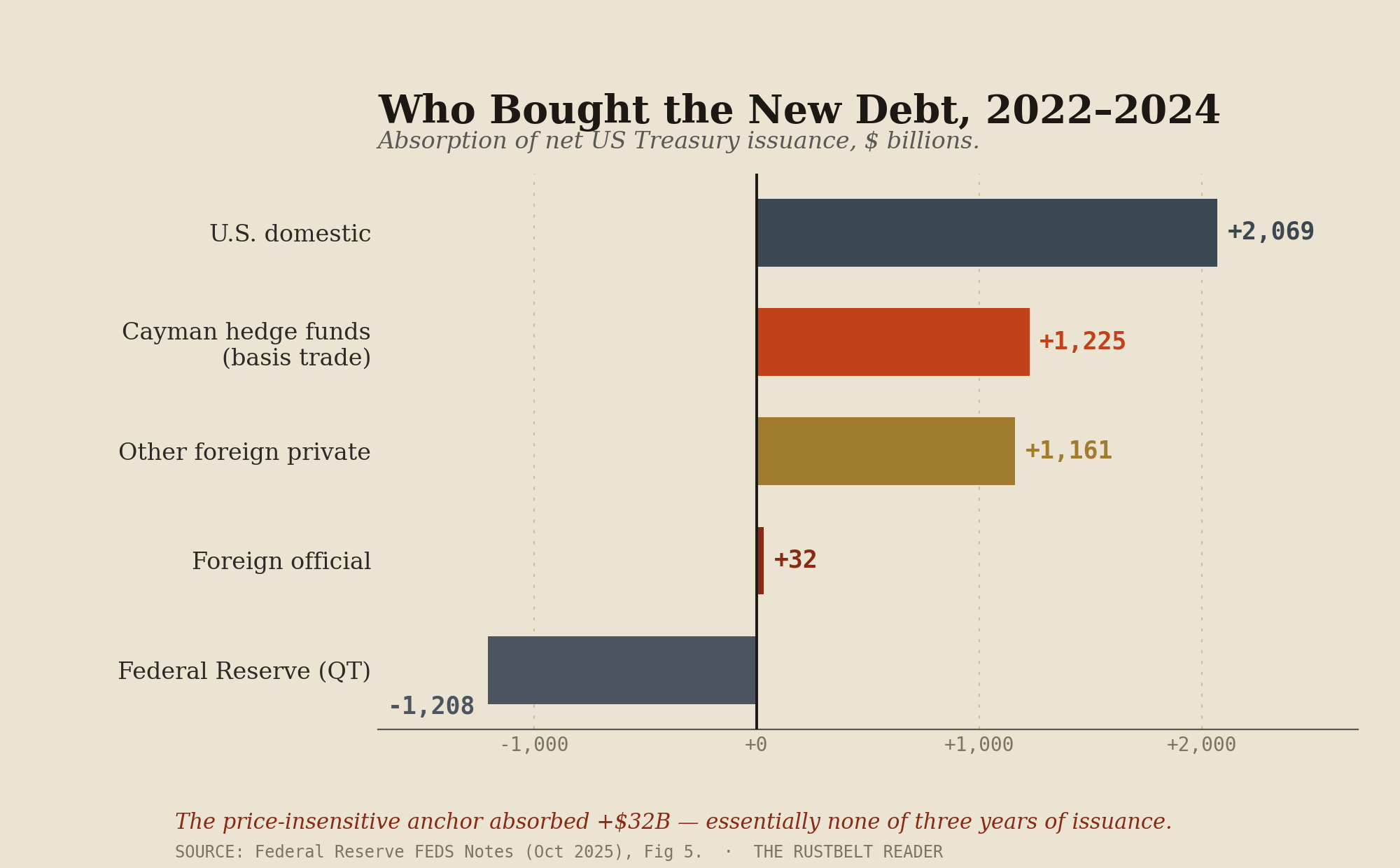

We do not know the private sector’s capacity to absorb United States debt at the current pace of issuance. It has never been tested at this scale, with this composition of buyers. For most of the modern era the question never arose, because the dominant buyers were price-insensitive — foreign central banks accumulating dollars because their mandates required it, the Federal Reserve absorbing duration because its policy demanded it. Price-insensitive buyers do not ask what yield compensates them. They show up regardless, and a market financed at the margin by such buyers can carry almost any quantity of debt without strain.

It helps to separate what is actually in question. The stock of debt — some $37 trillion — is not the immediate problem; large stocks can be carried for decades. The pressure is in the flow: a deficit near six percent of GDP at full employment means relentless new issuance that must be placed every week. The change that matters is in the marginal buyer of that flow. And the price that buyer demands shows up in two places the earlier essays decomposed — the real yield, near two percent and the highest since 2008, and the term premium, the compensation for holding duration, grinding back toward its historical norm after a decade suppressed below zero.

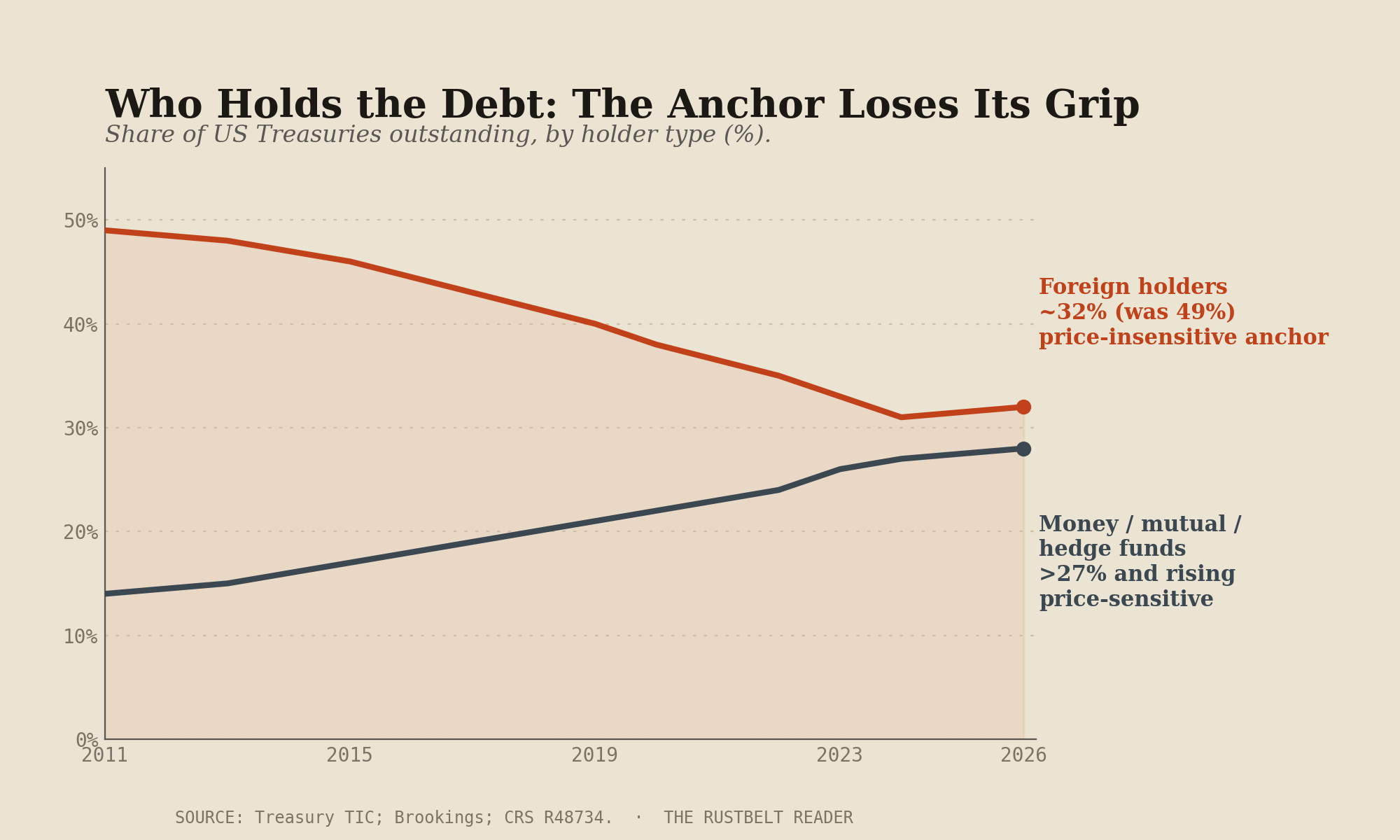

Here is the shift, stated carefully. The old anchor buyers have not disappeared. Foreign official holders still own roughly $9 trillion of Treasuries; the Federal Reserve still holds a vast portfolio. But they no longer dominate the marginal flow the way they once did. The foreign share of outstanding Treasuries has fallen from roughly half in 2011 to about a third today; foreign official accumulation stalled after 2014; and the Fed, after a decade as a buyer, spent two years as a net seller and now sits neutral. What increasingly sets the price at the margin is the price-sensitive buyer — the pension fund, the foreign private investor, the leveraged desk — who asks the question the central banks never did. What am I being paid to hold this?

So the binding variable is no longer whether the debt gets funded. It does; every auction clears. The binding variable is the price at which it clears, and whether that price resets gently or violently. This is not collapse, and the distance between “the financing has become fragile” and “the system is about to collapse” is where most writing on this subject loses its discipline. A clearing price is not an apocalypse. It is a number — possibly high enough to inflict a long, grinding adjustment on everything built when capital was free. That is a serious outcome. It is not the end of the dollar, and conflating the two forfeits the right to be taken seriously.

Balance-sheet utilization: the danger gauge of a financialized economy

This is the essay’s central idea, so let me give it bones rather than atmosphere.

In an industrial economy, the danger gauge was capacity utilization. In a financialized economy, the danger gauge is balance-sheet utilization — how much room the financial system’s balance sheets have to absorb selling before the selling becomes mechanical.

In the 1970s, when factory utilization pressed toward ninety percent, the productive system had no slack and a shock had nowhere to go but into prices. The modern equivalent is not in the factories. It is in the Treasury market’s capacity to absorb a wave of selling before dealers and leveraged holders are overwhelmed. When that capacity is ample, a financing shock is digested. When it is thin, the same shock turns into a spiral that ends only when a buyer of last resort appears.

Unlike capacity utilization, no official series reports this as a single number. But it can be built from observable components, and naming them is what turns an elegant idea into an instrument. Forced-selling capacity is a composite of:

1. Dealer balance-sheet capacity — how much inventory primary dealers can warehouse before they stop intermediating. 2. Hedge-fund Treasury leverage and basis-trade size — the pool of potential forced sellers. 3. Foreign official participation — the price-insensitive anchor, present or absent. 4. Treasury volatility (the MOVE index) — the market price of the fragility. 5. Repo funding stress — whether the leverage can still be financed. 6. Auction quality — tails, bid-to-cover, and indirect-bidder share, which reveal who is actually showing up.

Read together — and reading independent series together is the discipline this newsletter was built on — these describe a market whose surface is presently calm and whose plumbing is more leveraged, and less anchored, than the last time it broke. Volatility sits quiet today, though it spiked hard during the spring’s geopolitical shock. The basis trade sits near a record. Foreign official participation sits near a multi-decade low. The gauge does not say a break is imminent. It says the system is loaded. Those are different statements, and the difference is the honest content of this essay.

The plumbing, as promised

The previous essay left an IOU: a piece on the machinery that turns structural shifts into daily behavior. The gilt crisis is the key to reading it, because a debt crisis does not arrive as an auction with no bidders. It arrives through the plumbing.

The central pipe is the basis trade — an arbitrage in which hedge funds buy Treasuries and sell Treasury futures against them, capturing the small gap between the two, financed with heavy leverage in the repo market. Individually rational; collectively, a large and concentrated exposure. The trade is now estimated near $1.4 trillion gross, roughly double its 2020 size, concentrated in a handful of funds at high leverage. These funds have become among the larger marginal absorbers of new issuance — which means the buyer standing in for the departed central bank is, increasingly, a leveraged arbitrageur who holds the bond only while the trade works.

That is the mechanism in one sentence: the leveraged holder is a buyer in calm and a forced seller in stress. When yields move sharply, margin is called, positions unwind, the funds sell into a falling market — which lifts yields, which calls more margin. We have already seen the draft. In March 2020 the basis trade unwound violently; hedge funds sold an estimated $173 to $200 billion in cash Treasuries; dealers, capital-constrained, could not absorb the flow; the world’s deepest market seized; and the Federal Reserve was forced to buy at extraordinary pace to restore function. That is the shadow liquidity system the earlier essay promised to examine — not a system of buyers but of conditional holders, levered against one another, whose collective capacity to absorb a shock is balance-sheet utilization made concrete.

Why the two threads are one thread

The external-account series explained why the financing became fragile: the price-insensitive buyer lost its dominance, and the marginal buyer now asks the price. The Mellon series explained why the system cannot easily absorb the higher price that implies: for forty years the policy regime suppressed downturns, and the leverage and asset valuations that accumulated under that regime are now the system’s standing condition. One series described the spark; the other the fuel.

Put them together and the structure of the risk is clear. The cost of capital is the core input price of the largest sector of the modern economy — finance, insurance, and real estate, now roughly a fifth of output, where manufacturing once stood. When the cost of capital rises, it strikes the load-bearing wall, not a peripheral corner. It resets commercial real estate into a maturity wall — roughly $875 billion of loans due this year, much of it underwritten when money was free. It thins the equity cushion under every asset priced off the old rate. And it compounds, because the largest borrower whose cost of capital is rising is the federal government, whose debt is short enough that a higher rate reaches the interest bill within quarters, widening the deficit, demanding more issuance into a market already asking a higher price.

That is the loop. Not an oil shock, which raises a price and stops, but a financing shock, which raises a price and feeds on itself. The 1970s taught a generation to watch the oil terminal. The chokepoint moved. It is now the Treasury auction and the mortgage rate, because that is where the economic base now sits.

This is Ferguson’s point, and it is worth making explicit: the historical danger to a great power is rarely insolvency. Great powers do not vanish because creditors refuse them one morning. They weaken when debt service begins to compete with defense, with investment, with institutional renewal — when a rising share of the budget is spent servicing the past rather than building the future. The risk a rising clearing price describes is not a default. It is the slow crowding-out of state capacity by the cost of carrying what was already borrowed.

Two paths down

If the clearing price continues to rise — or merely remains structurally higher than the post-2008 system was built to bear — the question becomes how the adjustment occurs. There are two paths, and honesty requires holding both.

The benign path is the grind. The real ten-year yield settles at a structurally higher level and stays there — say two and a half to three percent for a decade. Painful but absorbable: it reprices assets gradually, stresses the leveraged corners, widens the deficit, and forces, eventually, some fiscal adjustment. An economy grinds through an orderly repricing the way it grinds through a long winter. A stressed assumption of five and a half percent on the nominal ten-year — where a normalized term premium would put it, within the range the market touched as recently as 2023 — is not a forecast of catastrophe. It is an estimate of the clearing price of an orderly adjustment.

The malign path is the gap: the same repricing, but disorderly, where the forced-selling dynamics in the plumbing turn a grind into a cascade, as they did in Britain. Here the yield does not settle; it jumps, because leveraged holders become forced sellers at once and balance-sheet capacity has run out. And this is where the two series collide, because the only actor large enough to arrest a gap is the central bank — and its capacity to do so is now itself a variable.

That is the fact distinguishing this moment from prior interventions. In 1987, in 1998, and in 2008, the Federal Reserve could halt a cascade because its own balance sheet was small and the sovereign’s debt manageable; the rescuer had clean books to lend against. Today it would arrive carrying $6.5 trillion already — the floor that never returned after the last intervention — atop a sovereign near $37 trillion with interest costs past a trillion dollars a year. The intervention required to halt each successive cascade has grown, while the credibility of each new intervention has become harder to take for granted. Where those lines cross, central bank balance-sheet expansion to stabilize a market private buyers are no longer willing to support at the prevailing price stops reassuring the market and starts unsettling it, because at that point the currency, not the bond, absorbs the adjustment. We do not know where that crossing lies. Anyone who claims to is selling something.

What would have to be true for this to be wrong

A thesis that cannot be falsified is prophecy, not analysis. So, honestly, what would have to be true for this argument to fail.

The market may clear at a higher price without incident — the grind, not the gap. Private buyers may have far more capacity than the fragility framework assumes, absorbing issuance at yields that are higher but stable, and the scenario resolves into nothing more dramatic than a decade of dearer money. This is not only possible; it may be the single most likely path. Fragility is a probability, not a certainty, and deep reserve-currency markets have absorbed shocks that would have destroyed smaller sovereigns.

Productivity may rescue the arithmetic. If the current investment wave durably lifts the growth rate, the deficit shrinks against a larger economy and the debt is outgrown rather than repriced. This is the strongest offset, because it works on the denominator — the only variable that makes the problem smaller rather than merely rearranged.

And the dollar’s network effects may prove more durable than any historical analog suggests. No prior reserve currency was embedded in the global plumbing as the dollar is; the demand that embedding creates has no precedent and may slow the erosion below what the historical cases would predict.

The case here is not that the malign path is fated. It is that the system has traded acute risk for chronic fragility, that the trade has a terminal point even if no one can date it, and that balance-sheet utilization is the instrument that tells you which path you are on. You do not have to predict the ending. You have to know what to watch.

And none of this means policy is helpless. Maturity extension, fiscal consolidation, the regulatory treatment of dealer balance sheets, a standing repo facility, changes in the composition of Treasury issuance — each affects the path, and several are already being debated. What policy cannot do is repeal the underlying question. It can shape how the question is answered. It cannot make the question go away: what price will the marginal buyer require?

The market is not a moral auditor

There is a temptation, having come this far, to reach for Mellon’s instinct — to say the pain is necessary, that the overdue audit should be welcomed. I resist it, because that is where this kind of analysis curdles.

Mellon was wrong about 1929. Irving Fisher showed why: in a leveraged economy, letting prices clear does not heal the system but accelerates the debt-deflation spiral that turned a crash into a catastrophe. The lesson of the 1930s is not that pain is good; it is that uncontrolled pain in a leveraged system is ruinous. Anyone who romanticizes the burn has not reckoned with the nine thousand banks that failed while the bottom refused to come.

But the part Mellon had right frames this moment. A system that never clears is one that has stopped pricing risk honestly; pain deferred is not pain avoided but pain compounded, paid by whoever comes next. We deferred for forty years. We let the Rust Belt take its audit in full — let the mills close, let the people who made things absorb the market’s discipline without mercy — and then, when the financial system faced the same test, we chose rescue. The country still lives with the difference.

And here a caution matters most. The market is not a moral auditor. It is a price-setting institution. It does not judge whether a society deserves pain or has earned a reckoning. It tests, mechanically and without sentiment, whether existing balance sheets can survive a higher clearing rate. To say the market will exact justice is to mistake a pricing mechanism for a moral one. The honest statement is narrower and harder: the United States has moved from a regime in which official institutions suppressed the price of its debt to one in which more of that price is discovered by private, leveraged, and price-sensitive balance sheets. That does not make a crisis inevitable. It makes the path of adjustment the central question.

Whether that adjustment is gentle or abrupt is the open question. The Bank of England got forty-eight hours of warning. We may get a decade, or we may get less. The arithmetic does not announce its timing. It only sets a price, and waits to see what the price can bear.

In the end, the clearing price decides.

Rustbelt Rules & Reflections

The question is always price. A solvent borrower can still be disciplined by the market. What gets repriced is not whether you are funded but what you are charged — and what the charge breaks.

Fragility is a probability, not a prophecy. The system is loaded, not doomed. The honest analyst names the gauge, not the date.

Balance-sheet utilization is the modern capacity utilization. In an industrial economy the danger gauge was the factory; in a financialized one it is the balance sheet’s room to absorb a shock.

The rescuer needs clean books. A lender of last resort reassures only while its own balance sheet and the sovereign’s can bear the rescue. When they cannot, the rescue becomes the risk.

Watch the plumbing, not the auction. The crisis arrives through the basis trade, the collateral call, the forced seller — not the failed sale.

The market sets the price; it does not render the verdict. It tests balance sheets. The meaning we assign to the test is our own.

The Rustbelt Reader studies history, measures the present, and imagines the future through the lens of industry, finance, infrastructure, and power. This essay synthesizes two series — the external-account thread (The Last Privilege, The Slow Unwinding) and the doctrine thread (The Last Central Banker). Figures on the external account, the Federal Reserve balance sheet, the basis trade, and current yields are drawn from the BEA, the Federal Reserve (H.4.1), Treasury TIC, the IMF, the CFTC, and Bank of England post-mortems, as of early June 2026. Historical relationships are shown for their shape; current readings are point-checked against primary sources. The conclusions belong to the reader.

This is excellent stuff. Thank you.