Return to Baseline

The resting rate of inflation has reset higher, and you can see it component by component in the basket. The near-term disinflation is real anyway — and the level and the rate are two different bets.

MACRO & MARKETS · JUNE 2026

There is a version of the inflation debate that is conducted entirely in the next three data prints. Oil plunged on the Iran ceasefire; the compute-price anomaly is unwinding; wage growth has softened. Add it up and the disinflationists are right that the coming months get cooler. I have said so myself, and I will say it again here: the near-term path is down.

But there is a second debate, conducted in decades rather than months, and it is the one that actually decides where rates rest. My argument across the last several months has been a single claim: the resting heart rate of inflation has reset higher than the 2010s, with 2% now closer to a floor than a ceiling. I built it from the bottom up — component by component, from shelter to goods to energy — and the purpose of this piece is to lay the whole structure out in one place, and then draw the distinction that matters most for anyone following it: the inflation level and the interest rate are two different bets, and the second does not follow automatically from the first.

We did not develop a new inflation problem. We lost the thing that was hiding the old one.

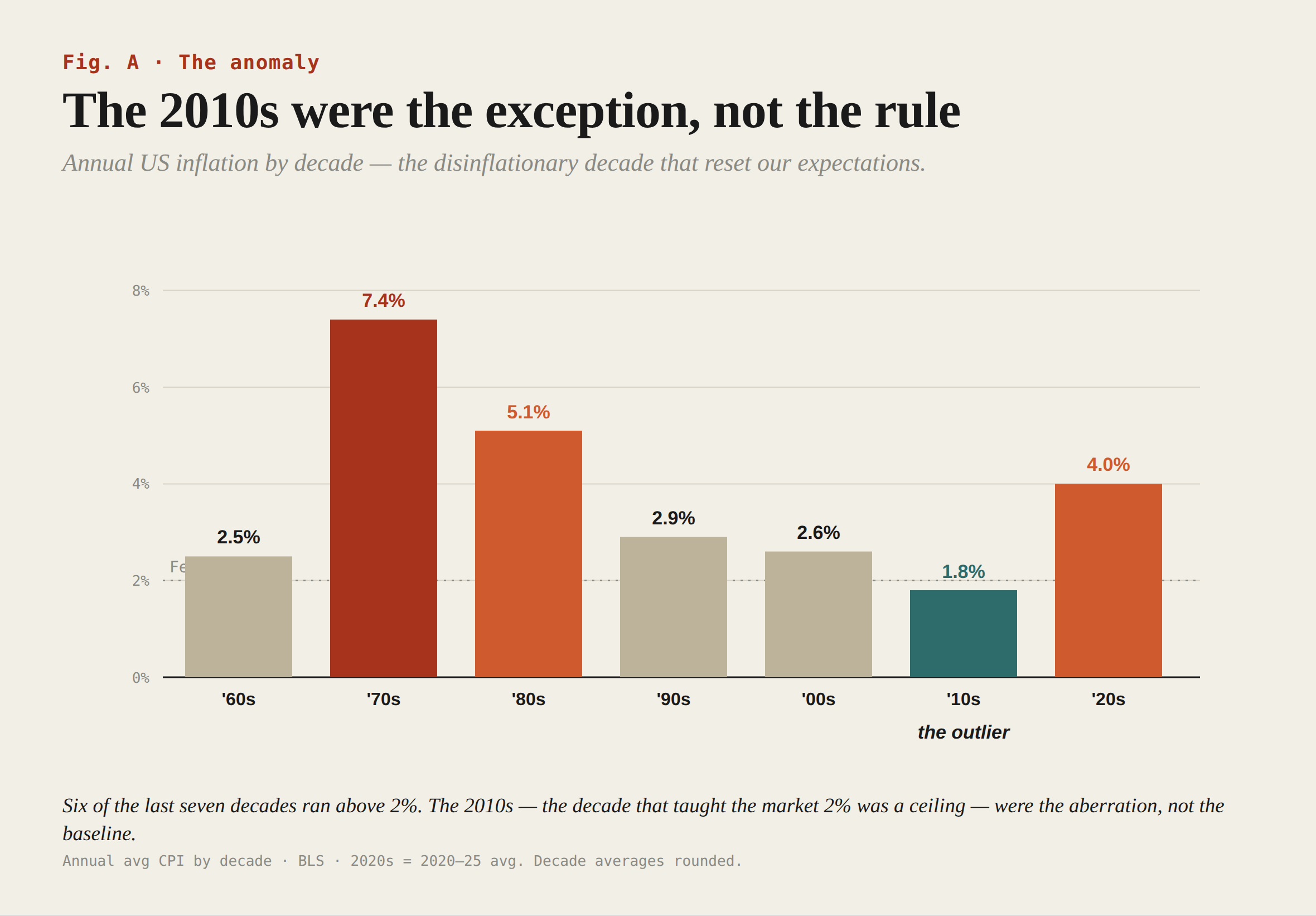

THE 2010s WERE THE ANOMALY

Start with the reframe that does the most work, because it inverts the entire debate.

We have spent years treating ~2% as the natural state of inflation and anything above it as a problem to be cured. The long history says that has the picture backwards. The 2010s, when inflation averaged something like 1.8%, were not the baseline. They were a uniquely favorable accident: China flooding the world with low-cost goods, shale coming online, post-crisis deleveraging suppressing demand, the 2000s commodity supercycle rolling off. An unusual convergence of downward forces, all pulling at once, strong enough to mask the upward pressure that was already there in services and housing.

That convergence is over. China’s export-share expansion has reversed into trade conflict. Shale’s one-time supply shock is spent. The deleveraging is done. And the upward pressure in services and housing that was always underneath — the pressure the 2010s masked — is now unopposed. We did not develop a new inflation problem. We lost the thing that was hiding the old one. The current environment is not “new” at all; it is a return to the pre-crisis baseline, where overheating pushes inflation above target and the burden falls on disinflationary forces to prove they can hold it down.

That is the macro claim. Here is where it shows up in the plumbing.

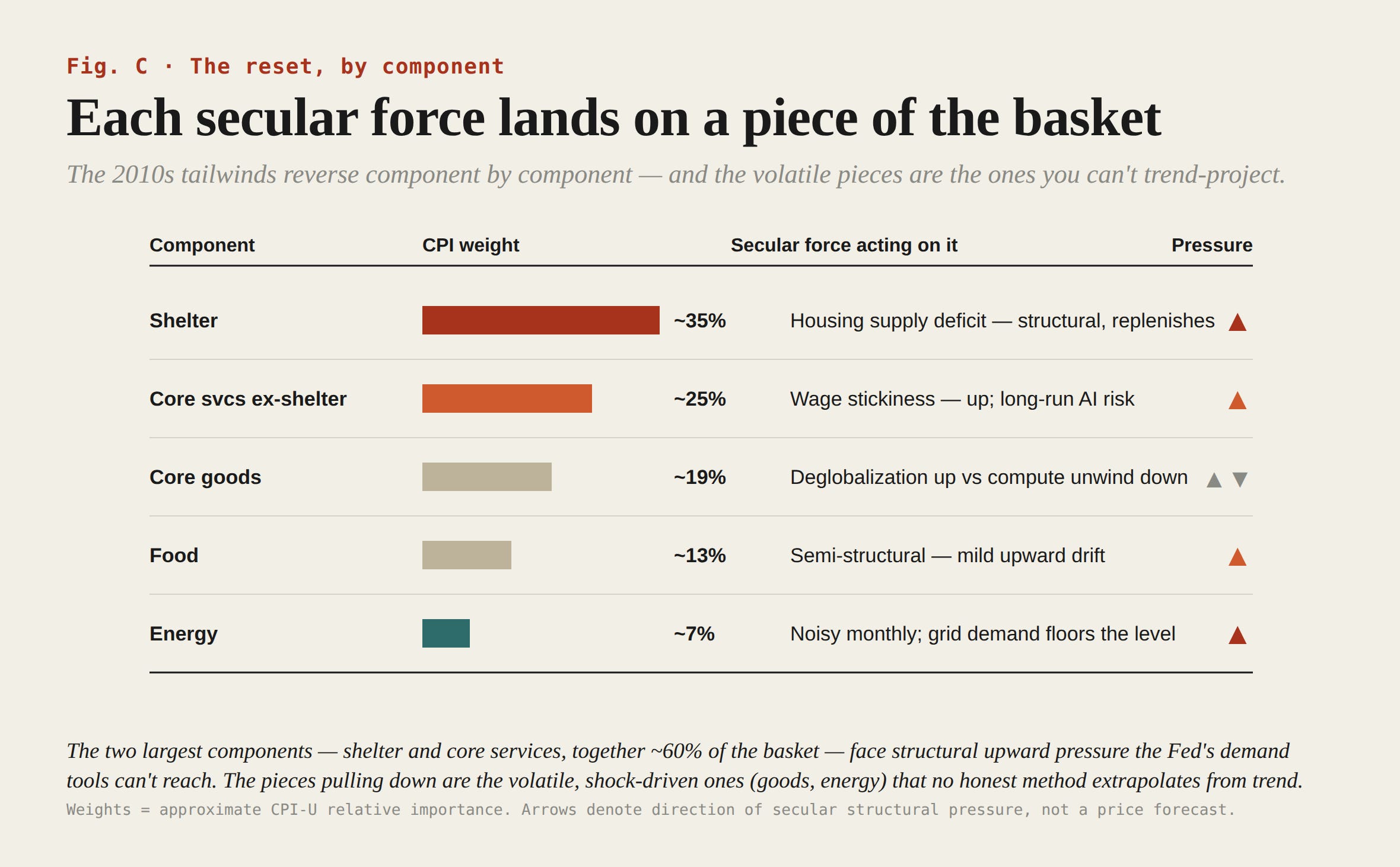

WHERE THE RESET LIVES IN THE BASKET

The secular forces are abstractions until you map them onto the components they move. Three of them land directly on pieces of the CPI I have written about before.

Deglobalization → core goods. The single largest source of the 2010s disinflation was the goods basket — China exporting deflation into it year after year. That tailwind is not just fading; it is reversing into a structural headwind as the world rotates away from lowest-cost production toward domestic industrial bases. The discipline here matters: the tariff impulse of the moment is best read as a one-off price-level increase, not a durable engine, and I will not pretend otherwise. The durable story is slower and bigger — the secular end of goods disinflation. For a decade, goods running near zero netted headline down to 2%. As goods stops subtracting, the same services-and-shelter pressure that was always there nets out higher. That is the “two regimes” point I have been making since the start: the disinflationary tailwind didn’t just fade, it became a headwind.

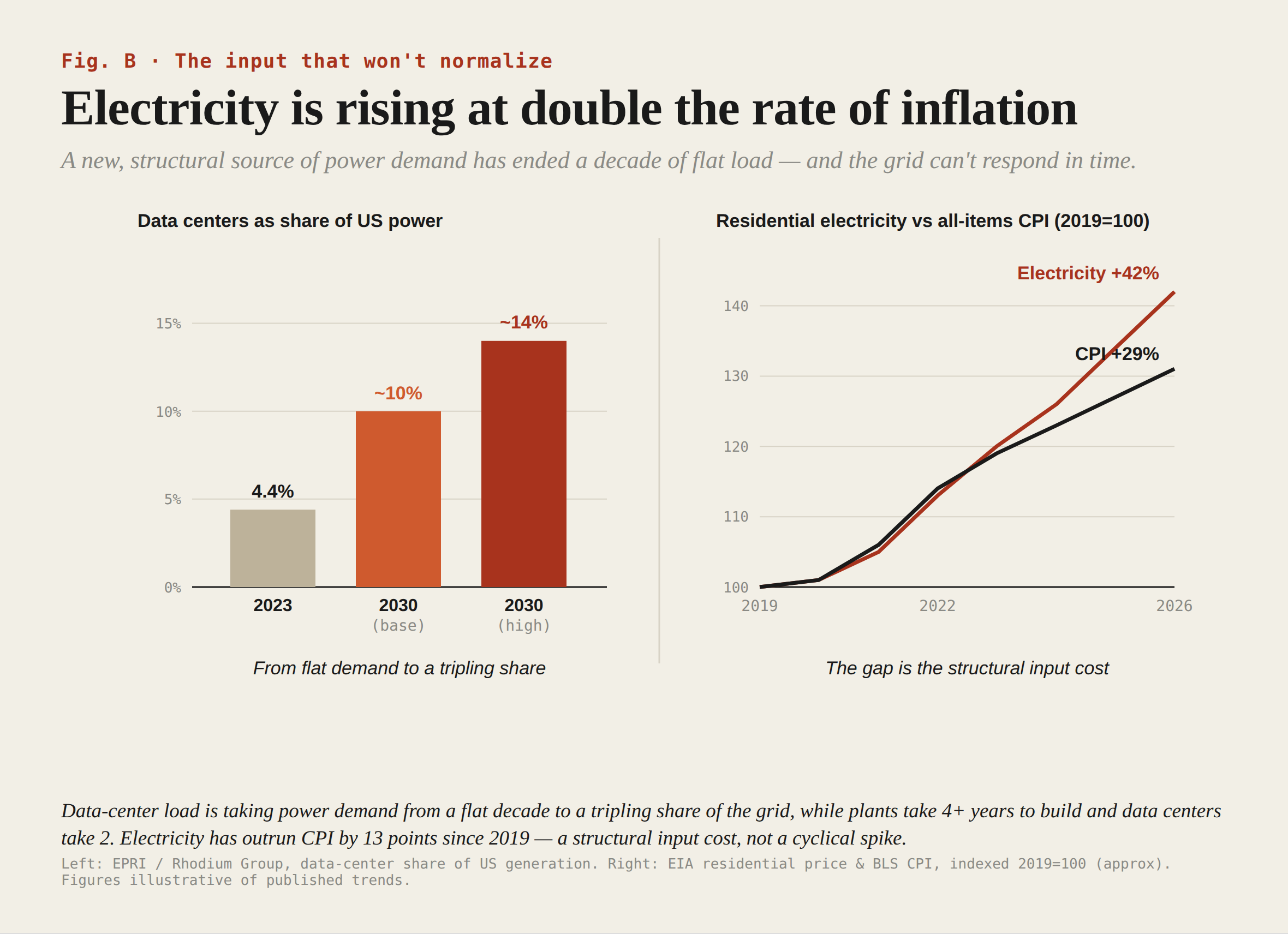

Fiscal activism and the energy transition → the floor under energy. I argued previously that energy will not simply normalize back down, because AI data-center buildout is adding a large and durable source of electricity demand for the first time in decades. That looked, at the time, like the most aggressive assumption in my estimate. The data has since caught up to it: electricity inflation is already outstripping broader prices, and the data-center capex flooding into the grid is pushing against constrained supply for the copper, the transformers, and the generation capacity it needs. The monthly energy print will stay violently noisy — it just round-tripped on a war premium and a ceasefire. But the level it reverts toward is structurally higher than the last cycle’s, and that is a floor-raiser hiding inside the most volatile component in the basket.

Fed independence → the floor under everything. The final force is institutional rather than arithmetic — it is the one my component math cannot see, and it may be the most important. A central bank under sustained political pressure to ease — a Fed where a governor has been fired and a sitting CEA chair installed as a voting member — is structurally more likely to run policy a touch too loose for conditions. The historical record is not subtle: economies with less independent central banks have tended to run higher realized inflation over time. Even where there is a valid near-term case for easing — and there is one today — the long-run expression of political influence is downward pressure on rates relative to what conditions warrant. That is an institutional floor no shelter model or goods basket will show you, and it ties to the Fed’s recent withdrawal of forward guidance: less anchoring, more discovered pricing, in exactly the direction that lifts the resting rate.

A note on company. I reached this from the bottom up — from underwriting CRE and watching the basket. Bridgewater’s recent secular study reached the same place from the top down: a resting rate reset higher, 2% now a floor rather than a ceiling, the 2010s as the anomaly. When the plumbing and the macro model point independently at the same floor, weight it more than either alone. (Their study ends in a pitch for inflation hedges, which is their business; I’m taking the analysis, not the sales close.)

THE WILD CARD, POSITIONED

The honest objection to all of this is AI. If it delivers a productivity miracle, it could drive disinflation large enough to override every force above — cheaper labor on a productivity-adjusted basis, automation cooling the job market, cost-saving innovation across the economy.

I do not know where AI nets out, and I distrust anyone who claims to. But Bridgewater’s study reframes the uncertainty in a way that resolves the paralysis: betting that AI disinflation will be more than enough to offset the entire stack of secular inflation pressures is the speculative position. Near-term, AI is plainly inflationary — it is bidding up electricity and industrial commodities right now. The disinflationary payoff is real but it lives in the long tail and at uncertain magnitude. So the base case is not “AI rescues 2%.” The base case is that AI is one more force in a wide cone, pushing down over a horizon nobody can date, against a present that is pushing up. The burden of proof sits with the disinflationists, and it is a heavy one.

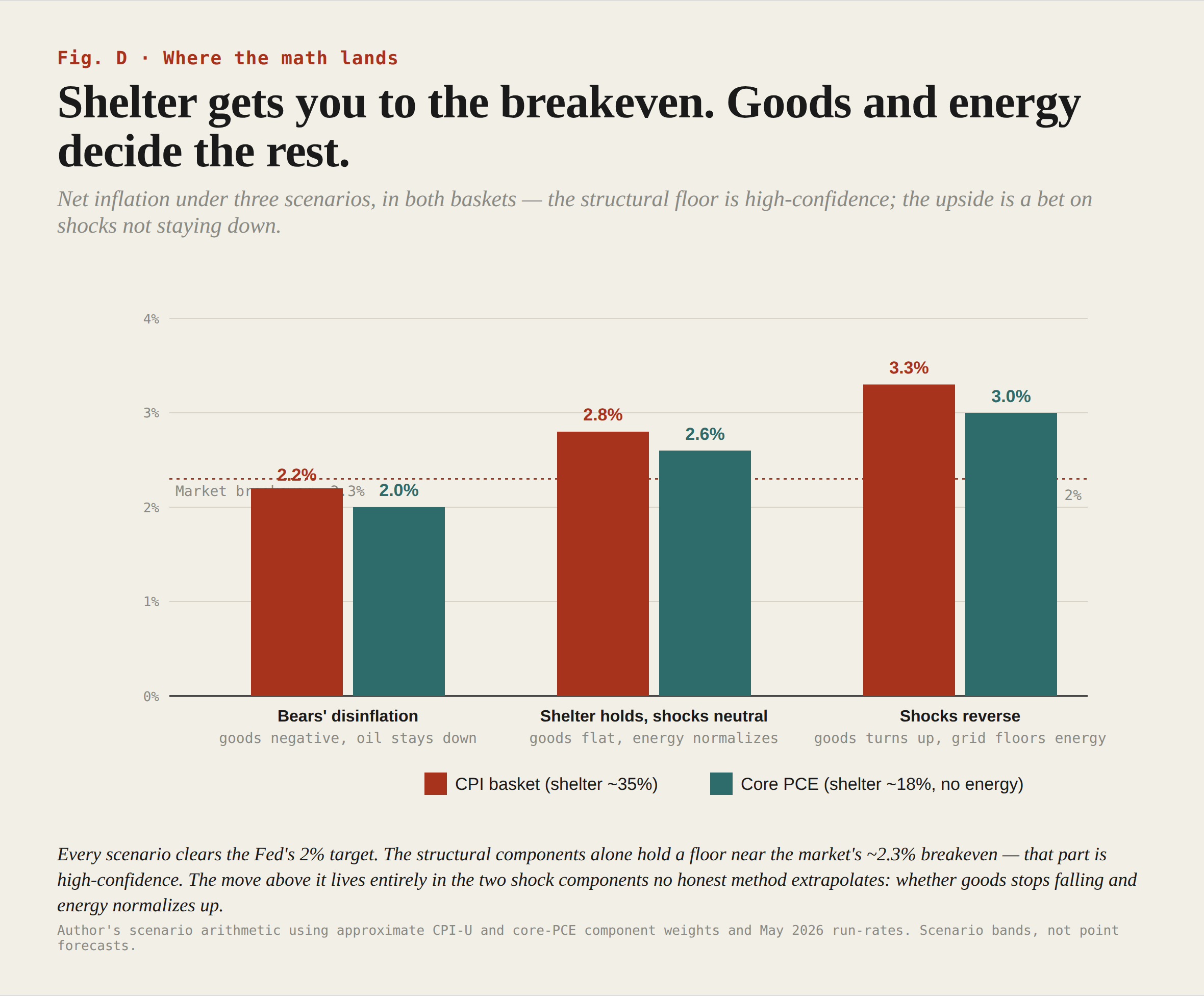

SO WHERE DOES THAT LEAVE THE FLOOR

The next several prints soften — commodities and the compute anomaly roll off, the lagged components ease mechanically. That disinflation is real, and it is cyclical noise on top of a resting rate that has structurally reset higher: goods no longer subtracting, energy floored by the grid, services sticky, shelter held by a supply deficit, an institutional thumb on the scale. The disinflationists are measuring the noise. The level it decelerates toward sits meaningfully above the 2% the market still treats as gravity. The 2010s told us 2% was the floor; the basket in front of us says it is closer to the ceiling.

THE LEVEL IS NOT THE RATE

Here is the distinction I underweighted until a sharp exchange forced it, and it is the most important caveat in this piece: a higher resting rate of inflation does not automatically mean higher interest rates. Those are two claims, and the second does not follow from the first. What connects them is the Fed’s reaction function — and the reaction function is doing something right now that cuts against the trade you would naively put on from everything above.

The near-term read belongs to the disinflationists, and I will give it to them plainly. The commodity impulse is reversing, oil has fallen, the compute anomaly is unwinding, and the prints over the coming months get softer — softer still for anyone watching three- or six-month averages. More to the point, this is a Fed that projected cuts with core inflation at 2.5%, under real political pressure to ease. A central bank with that revealed reaction function does not hike into a mid-2s floor. It looks through it and cuts. So the front-end trade — long the short end, betting the Fed eases more than the market prices — is the correct expression of the near-term, and I would not fight it. For the next several months, the level barely matters; the response is everything, and the response is dovish.

The structural read is where I plant the flag, and it is a claim about the durability of that reaction function, not the level. “Cut into 2.5%” is a reaction function calibrated to a belief — that disinflation is still ongoing, that the above-target print is a way station on a glide path to 2%. My entire case is that the glide path ends in the mid-2s-to-low-3s and stays there: goods no longer subtracting, energy floored by the grid, services sticky, the institutional thumb on the scale. If that floor proves real, the premise underneath “look through it” fails. You can treat an above-target rate as transitory for only so long before a stable floor forces the question — and when the Fed stops calling a structural floor temporary, the reaction function re-rates. The market is not pricing that eventual capitulation, and the timing of it is the actual edge.

So the two reads do not collide; they sit at different points on the curve and different points in time. The front end rallies on the cuts. The long end is where the structural floor bites — and a Fed cutting aggressively into a floor that will not fall is precisely the setup for a steeper curve and, eventually, an un-anchoring of long-end inflation expectations. The near-term dovish trade and the long-term structural floor are not opposites. The first may well be the bridge to the second.

THE FALSIFICATION

The thesis now has two pieces, and each can fail in its own way.

The level fails if the 2010s forces re-emerge: if China re-floods global goods markets, if a new supply shock does for energy what shale did, or if AI productivity arrives faster and larger than the inflationary capex it requires. Then the resting rate falls back toward the 2010s and the disinflationists are right about the regime, not just the next three prints. I do not expect it, but that is the bet.

The rate claim fails if the Fed simply accommodates the higher floor indefinitely — if a less independent, politically pressured central bank decides a mid-2s/low-3s world is fine and never re-rates its reaction function to fight it. In that world I could be entirely right about the floor and still wrong that it ever forces higher rates. That is the genuine risk to the structural trade, and notably it is the same Fed-independence dynamic I cited as a floor-raiser cutting the other way — the institution that lets inflation run higher is also the one that might never lean against it. I have to hold both.

So: watch the level, but watch the response harder. Everyone agrees the next prints fall, and the front end should rally as the Fed cuts. The structural argument is that a floor which refuses to keep falling eventually breaks the reaction function that is currently trading it — and the market is pricing neither the floor nor the capitulation it will force.

The fever is breaking. The baseline it breaks back to is not the one we got used to — and the harder question is not where inflation settles, but how long the Fed pretends it hasn’t.

Supports my thesis that the next decade or so supports good economic growth here in Canada. Especially the West.