Reflections: Mellon Accepted Burn. We Accepted Bubbles. Now the Financial Forest Is Ready to Blow.

Why central bankers must stop being firefighters and start becoming forest managers.

Authors Note:

I often write about economic history, and pieces like this aren’t for everyone.

That’s why I label my work clearly, so you can effectively follow the threads you enjoy and skip what doesn’t speak to you.

Some readers come for the Battles series, others for the Builders, others for Reflections like this one.

My hope is simply that each labeled piece helps you choose your own way through The Rustbelt Reader.

Every economic crisis forces nations to confront the same ancient question: How much pain is necessary?

There are only three ways to meet a fire: invite it, fight it, or manage it.

Andrew Mellon invited it.

Paul Volcker managed it.

Ben Bernanke fought it.

The truth lies not in the extremes, but in understanding how to manage the forest.

I. Mellon Revisited: A Flawed Response, but an Honest Instinct

This must be stated clearly:

The liquidationist advice attributed to Andrew Mellon during the Great Depression was a mistake. [1]

The economy was too large, too interconnected, and too fragile for such severity. Unemployment soared. Deflation spiraled. The financial system buckled.

But Mellon’s underlying instinct—that economies require periodic clearing—was not entirely wrong. His worldview, forged by Thomas Mellon’s frontier ethic of thrift and hardening through adversity, recognized something modern policymakers often deny:

Systems weaken when corrections are delayed indefinitely.

Mellon misjudged the scale.

The fire became uncontrolled.

But the instinct behind his error still matters.

II. Volcker: The Measured Fire

Paul Volcker succeeded because he understood what Mellon did not:

The burn must be large enough to restore discipline, but controlled enough to preserve the system.

Facing runaway inflation, Volcker delivered pain—controlled pain:

Interest rates above 20%

Two recessions

A deliberate breaking of inflation psychology[^2]

It was not elegant; it was blunt.

It crushed farmers, strained manufacturers, and triggered debt crises abroad.

But domestically, Volcker held the containment line.

He cleared the underbrush without letting the blaze jump the forest.

His “controlled burn”:

restored trust in the dollar,

rebuilt the long-term foundation of credit markets,

and positioned the country for decades of expansion.

In this sense, Volcker redeemed Mellon’s instinct while avoiding Mellon’s error.

But here is the irony:

Volcker’s victory created the stability that later policymakers used to justify ever-lower interest rates, ever-higher leverage, and ever-greater intervention.

The measured burn became the justification for forty years of increasingly suppressed fires.

Note: Volcker and Ben Bernanke held the exact same office —an independent Chairman separated from the Treasury. This independence is what allowed him to raise rates against the political wishes of the White House. This was different for Mellon — he held both roles. Fed independence is a point widely discussed in markets today.

III. Bernanke: The Overcorrection Era

Ben Bernanke, shaped by scholarship on the Great Depression, acted decisively in 2008 to prevent Mellon’s mistake from repeating.

He stabilized credit.

He halted deflation.

He prevented collapse.

But this ushered in the Age of Suppression:

Zero interest rates

QE as a recurring tool

Perpetual rescue expectations

Systemic aversion to natural downturns[^3]

Bernanke saved the economy—but the doctrine that emerged from his era created a forest too dense, too leveraged, and too dependent on intervention.

This is not Bernanke’s fault.

It is the institutional path our system adopted.

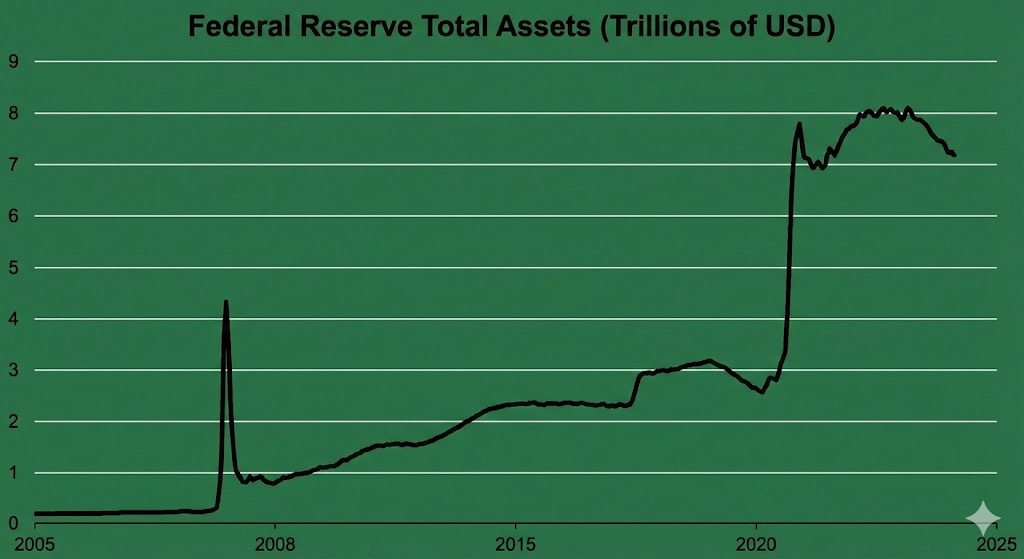

The Risk of the Vertical Line:

This exponential expansion represents the "Age of Suppression" in visual form. When the central bank becomes the buyer of last resort, it suppresses the natural cost of risk. The danger is twofold: First, it distorts price signals, encouraging capital to flow into speculative assets rather than productive growth. Second, it creates a "liquidity trap"—scaling this mountain is easy, but climbing down (Quantitative Tightening) without crashing the market is historically unprecedented. At least to my knowledge.

IV. Pittsburgh: The Case Study of Measured Collapse

Pittsburgh proves the point more vividly than any textbook.

The steel collapse of the 1980s was painful—brutally so—but not total.

There was no federal QE for the blast furnaces.

No bailout for the mills.

The fire burned.

We must not romanticize the flames.

The transition cost Pittsburgh nearly half its population—a diaspora of families searching for work in distant states and distant lives.

The burn cleared the land, but it scarred the earth.

And yet, the roots held:

Universities

Hospitals

Engineering culture

Civic resilience

Identity forged in steel and struggle

Because the burn was real—painful but measured—Pittsburgh was forced to find new soil.

It rebuilt into a hub for robotics, AI, healthcare, and advanced manufacturing.[4]

Pittsburgh is the national metaphor:

Controlled fire leads to resilient rebirth.

Uncontrolled fire destroys.

Suppressed fire weakens.

V. The New Doctrine: Central Bankers as Forest Managers

Neither Mellon’s severity nor Bernanke’s suppression is sustainable.

The correct doctrine is Volcker’s: measured fire.

Central bankers must become forest managers:

1. Allow natural correction cycles.

Small burns prevent big ones.

2. Prevent system-wide destruction.

Never repeat 1930–32.

3. Preserve long-cycle health.

Currency credibility, middle-class stability, and geopolitical strength all depend on a system that renews itself.

The dollar’s reserve status is not eternal.

It rests on trust—trust built through stewardship, not convenience.[5]

Empires fall when forest management collapses—

when discipline yields to expedience,

and when fires are either ignored or extinguished entirely.

VI. Conclusion

The path forward is neither Mellon’s liquidation nor Bernanke’s endless rescue.

It is a disciplined, ecological approach to economics:

“Healthy systems don’t avoid fire.

They use it.

They manage it.

They grow stronger from it.”

When nations avoid every burn, they build up the underbrush of excess until a spark becomes a catastrophe.

When nations manage their cycles with discipline, they renew themselves.

Nature’s cycle is never complete.

It waits for leaders wise enough to guide it.

Rustbelt Reflection

Pain is not the enemy.

Unmanaged pain is.

Strength comes not from perpetual rescue,

but from allowing systems to renew themselves before they break.

Select Quotes:

Andrew Mellon

“Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate…” (Attributed by Hoover)[1]

“The harm done by speculating with borrowed money is far greater than any temporary benefits.”

Paul Volcker

“The basic responsibility of the Federal Reserve is to maintain the value of the currency.”

“Once you lose credibility, you lose everything.”[2]

Ben Bernanke

“In 2008, the choice was between intervention and catastrophe.”

“The lesson of the Great Depression is clear: allow no deflationary collapse.”[3]

Footnotes / Work Cited

[1]: Herbert Hoover, The Memoirs of Herbert Hoover: The Great Depression, 1929–1941. Scholars debate whether Mellon used these exact words, but they accurately reflect his liquidationist stance.

[2]: Paul Volcker & Toyoo Gyohten, Changing Fortunes (Times Books, 1992).

[3]: Ben S. Bernanke, The Courage to Act (W.W. Norton, 2015).

[4]: Christopher Briem, University of Pittsburgh – Regional Economic Studies.

[5]: Barry Eichengreen, Exorbitant Privilege: The Rise and Fall of the Dollar (Oxford University Press, 2011).

Editor’s Note:

In the coming weeks, I’ll be publishing a follow-up piece exploring a timely question: What would Andrew Mellon think of America’s current fiscal deficit and national debt?

Mellon’s worldview—shaped by frontier discipline, industrial prudence, and a suspicion of excess—offers a framework for understanding today’s fiscal trajectory. That essay will examine his likely views on deficits, debt monetization, and the long-term sustainability of America’s balance sheet.

If you enjoyed this reflection:

The Rustbelt Reader grows through readers like you. I label my work so you can follow the threads you care about—Battles, Builders, Statesmen, Reflections, or Pittsburgh history.

If you’d like to support more independent writing on economic history, civic resilience, and Rust Belt renewal, consider subscribing or sharing the newsletter with someone who might appreciate it.

Thank you, sincerely, for reading.