Capital Allocation After the Easy Decade

Why the last ten years trained the wrong instincts—and why that matters now

Writers often opine on asset classes, allocations, or investment strategies—and that can be useful. But too often we skip the more important question: the foundation those decisions rest on.

In capital allocation, the ultimate objective isn’t nominal returns, benchmark-relative performance, or even volatility control. It’s the preservation and growth of purchasing power over time. That’s what investors actually live on—what funds future consumption, flexibility, and security.

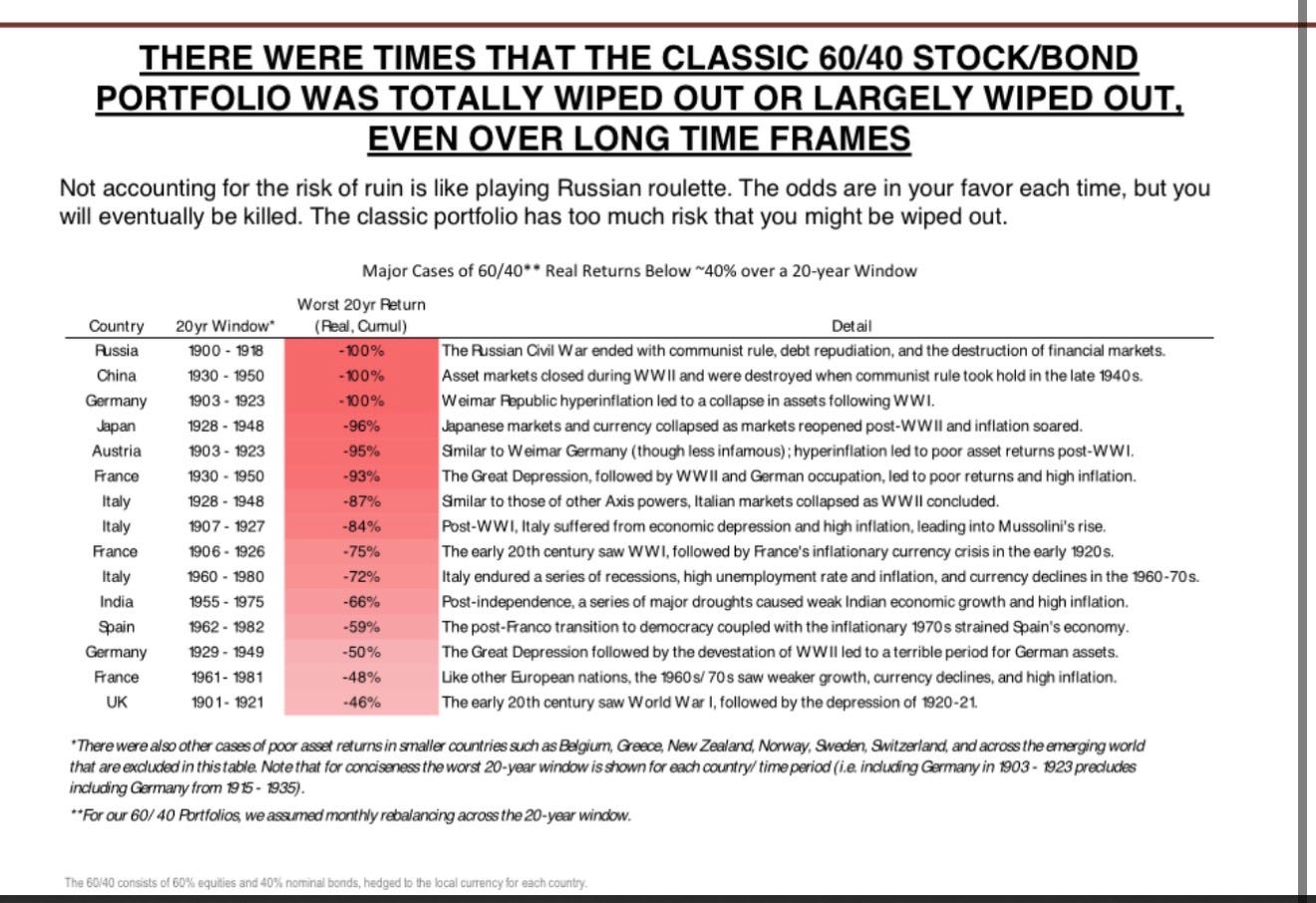

History is clear that wealth can be permanently impaired not only by sudden crashes, but by long stretches in which purchasing power quietly erodes.

The last decade made it easy to forget that.

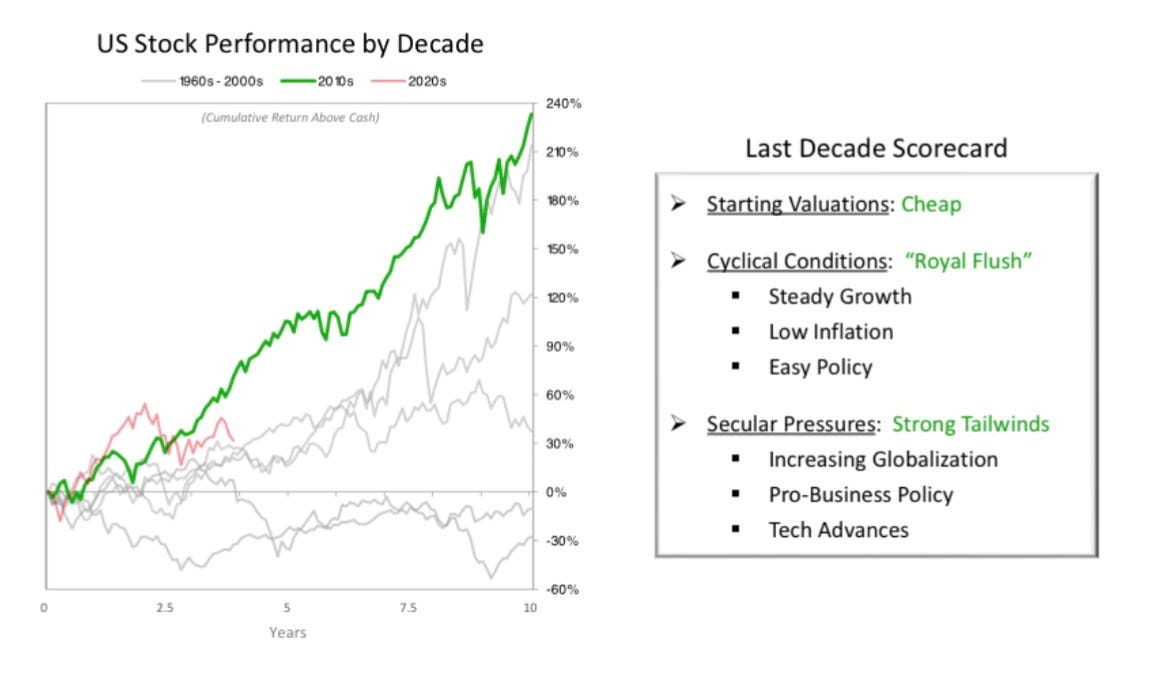

First, a reminder of just how unusual the recent period really was

The past decade sits at the extreme upper end of historical experience for U.S. equity performance. Measured relative to cash, returns were not merely strong—they were exceptional.

This matters because investors do not form expectations in textbooks. They form them through lived experience. For many market participants, this period came to feel normal: steady compounding, shallow setbacks, and fast recoveries. History suggests it was anything but.

Strong returns weren’t accidental—they were structural

The last decade benefited from a rare alignment of favorable conditions: cheap starting valuations, steady growth, low inflation, easy monetary policy, globalization, and rapid technological progress.

This combination didn’t just lift returns—it pulled them forward. When valuations expand while discount rates fall, future returns are effectively borrowed into the present. The danger isn’t that these forces reverse all at once, but that expectations forged under a “royal flush” fail to adjust when the cards change.

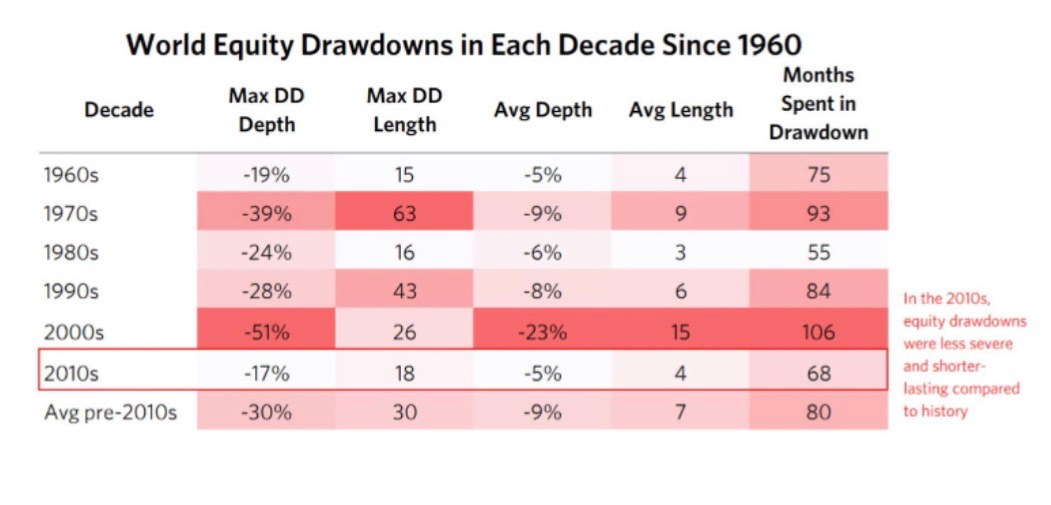

Policy didn’t eliminate risk—it shortened pain

A defining feature of the 2010s was not the absence of drawdowns, but their brevity. Compared with earlier decades, equity declines were generally shallower and resolved more quickly.

This experience reshaped behavior. Drawdowns came to feel temporary. Risk felt manageable. Leverage felt survivable. That conditioning was rational—but it rested on the assumption that policy would always have room to respond. History shows that assumption is regime-dependent, not permanent.

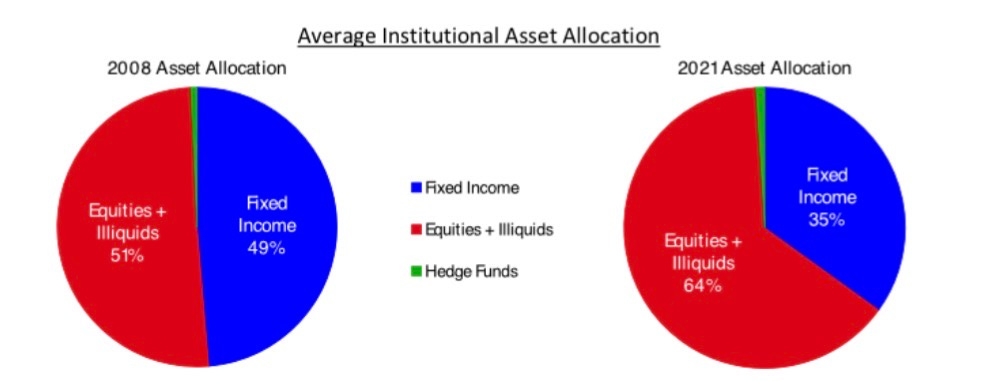

Portfolios adapted rationally to that environment

Faced with falling yields and fast equity recoveries, portfolios evolved in predictable ways. Fixed income allocations declined. Equity exposure rose. Illiquid assets gained favor. Risk budgets expanded.

These shifts were not reckless—they were adaptive. But they also concentrated exposure to a narrow set of assumptions: continued growth, policy flexibility, and stable correlations. Risk did not disappear. It converged.

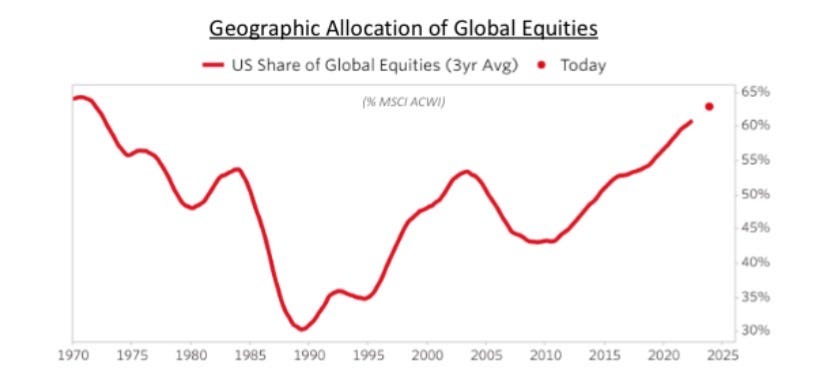

Geographic concentration increased alongside asset concentration

At the same time, capital increasingly flowed toward U.S. assets, reinforcing geographic concentration. Superior returns, policy credibility, and technology leadership pulled global portfolios toward a single dominant market.

Diversification within a winning regime replaced diversification across regimes. That works—until it doesn’t.

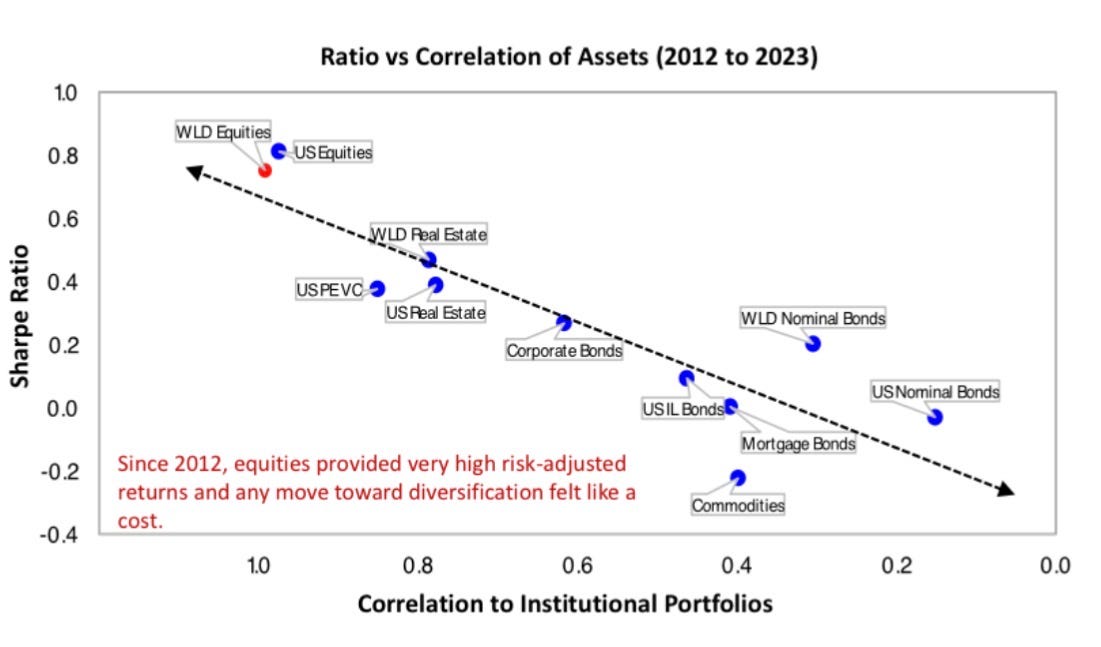

Over the last decade, diversification felt like a cost

Since 2012, equities delivered unusually high risk-adjusted returns, while traditional diversifiers lagged. In that environment, reducing correlation often meant reducing performance.

The cost of diversification was visible every quarter. The benefit remained theoretical. For a long time, that tradeoff appeared irrational to accept.

But diversification isn’t designed to maximize Sharpe ratios in calm seas. It exists to protect purchasing power when correlations rise and regimes break.

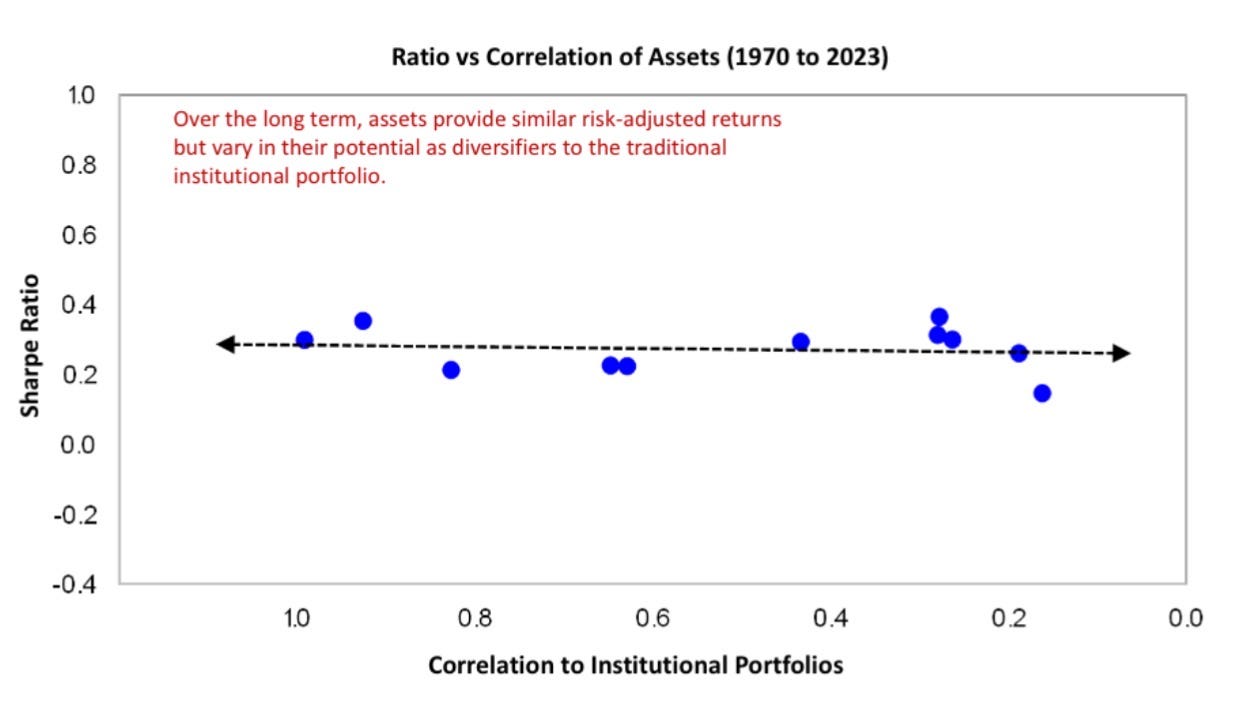

That experience is unusual—and dangerous to extrapolate

Over longer horizons, risk-adjusted returns across asset classes tend to converge. What differentiates them is not return potential, but how they behave relative to one another under stress.

The recent period rewarded concentration and penalized balance. History suggests that outcome is the exception, not the rule. Extrapolating it forward is one of the most common—and costly—errors investors make after an easy decade.

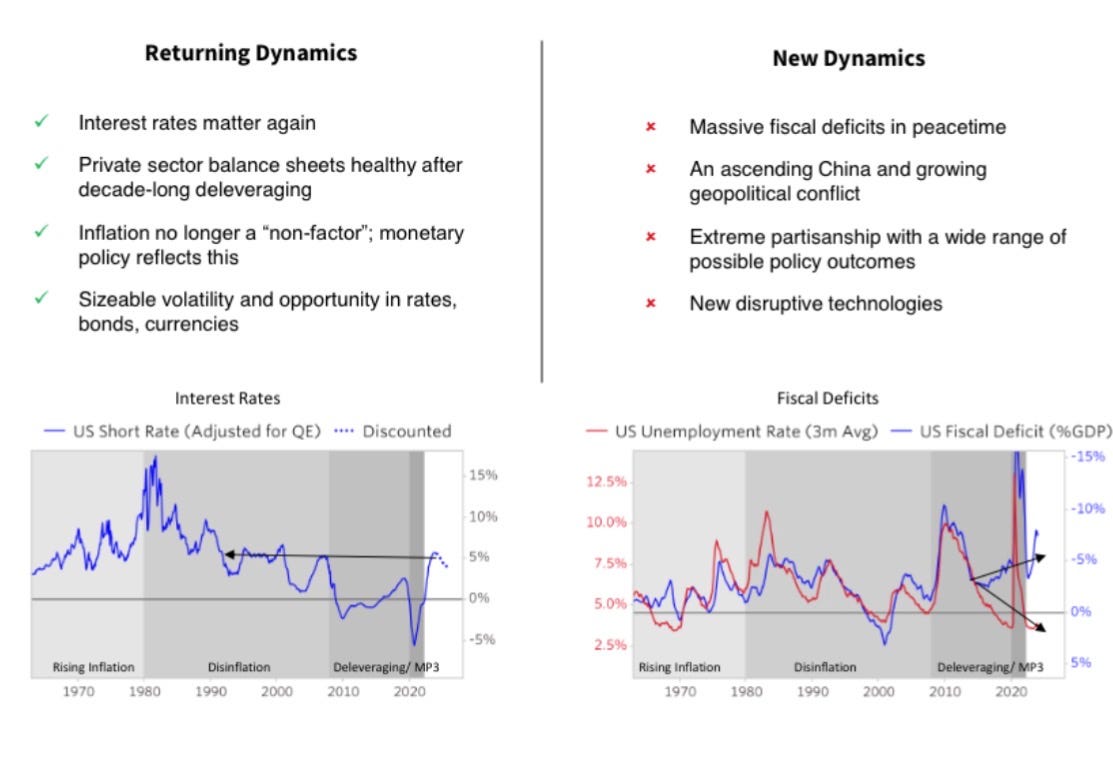

A more complex regime is emerging

Old constraints are returning. Interest rates matter again. Inflation is no longer a non-factor. Volatility has reappeared across rates, bonds, and currencies.

At the same time, new pressures complicate the backdrop: large fiscal deficits in peacetime, geopolitical fragmentation, political polarization, and rapid technological disruption. These forces interact rather than cancel, creating feedback loops rather than clean cycles.

In such an environment, portfolios optimized for stability and extrapolation are fragile.

What wealth management is really about

Wealth management is not about predicting the next regime. It is about avoiding permanent impairment of purchasing power across regimes.

That requires a shift in priorities:

from optimization to resilience

from Sharpe ratios to correlation behavior

from efficiency to optionality

from recent winners to structural roles

Diversification can feel expensive—until it becomes essential. The most dangerous moments often follow the most comfortable data.

But before we debate which assets belong in a portfolio, it is worth clarifying what those assets are meant to do.

That is the task of Part II.

If you want Part II—asset class fundamentals—subscribe. The goal isn’t more opinions. It’s a better model.

Brilliant easy to understand timely, history lesson. Wow

Thank you so much.